At BBH, we are always searching for differentiated investment strategies that can help enhance long-term portfolio returns while reducing risk. Over the past few years, we have been particularly focused on adding independent return strategies that can provide equity-like returns but with lower volatility. While we believe this provides unique diversification and return benefits in all environments, independent return strategies can play a particularly valuable role during periods of higher equity market valuations. Here, we explain how incorporating independent return strategies can play a key role in enhancing a portfolio’s return potential, diversifying return sources, and positioning it for the future.

Market context and portfolio positioning

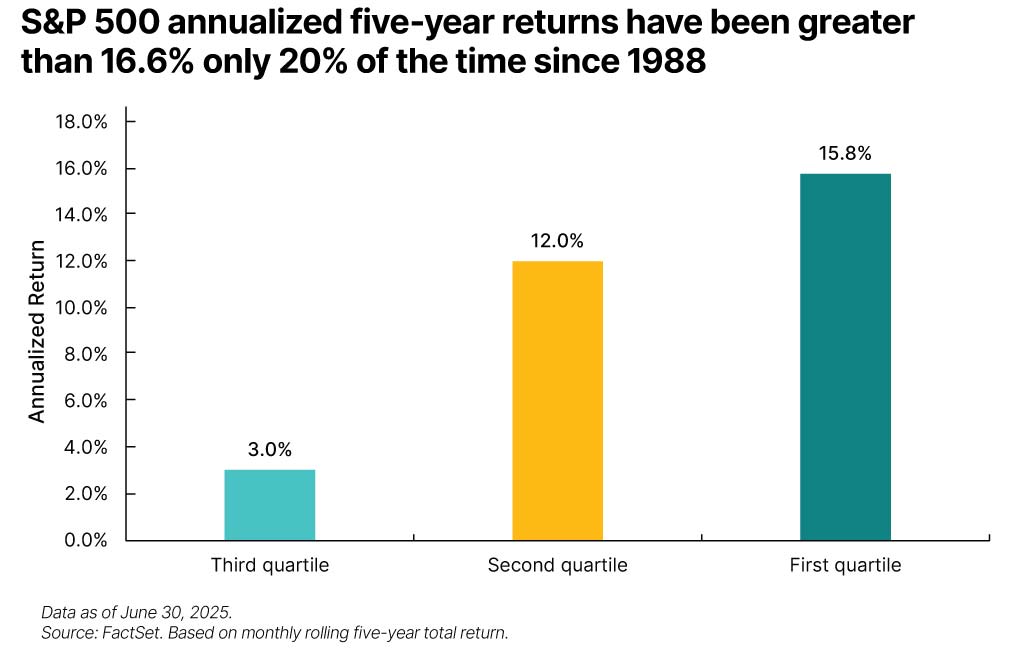

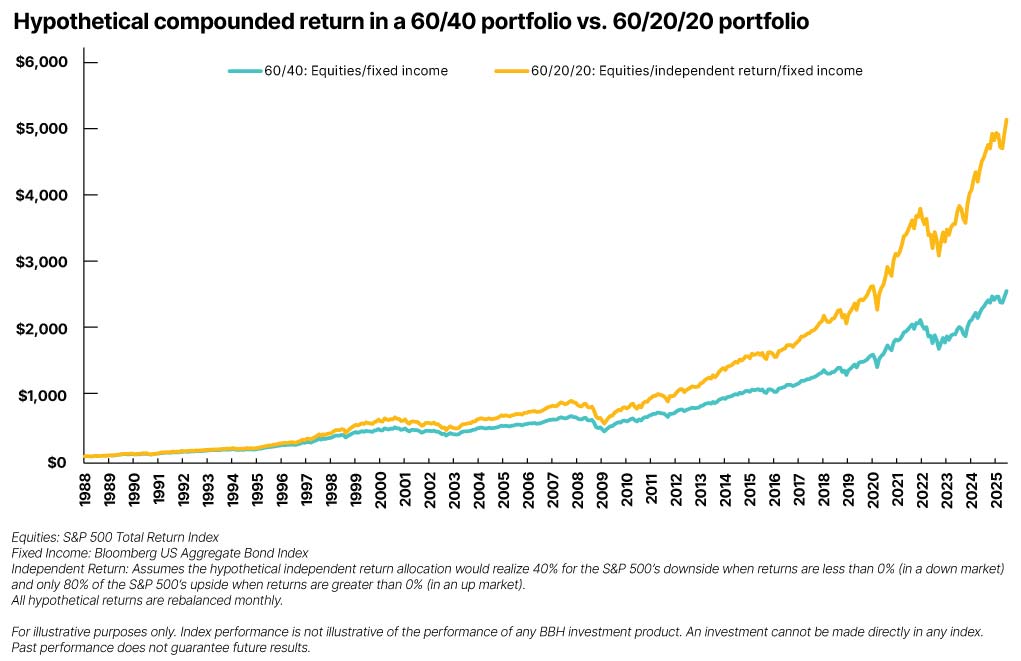

Despite continuous headlines about volatility and uncertainty, market performance has been strong over the past five years – note the S&P 500’s 16.6% annualized return, which represents a top-quartile return for the index. As shown in the nearby chart, the S&P 500’s first-quartile five-year annualized return between 1988 and second quarter 2025 was 15.8%. Of the 390 rolling observations, the index generated a return greater than 16.6% only 20% of the time.