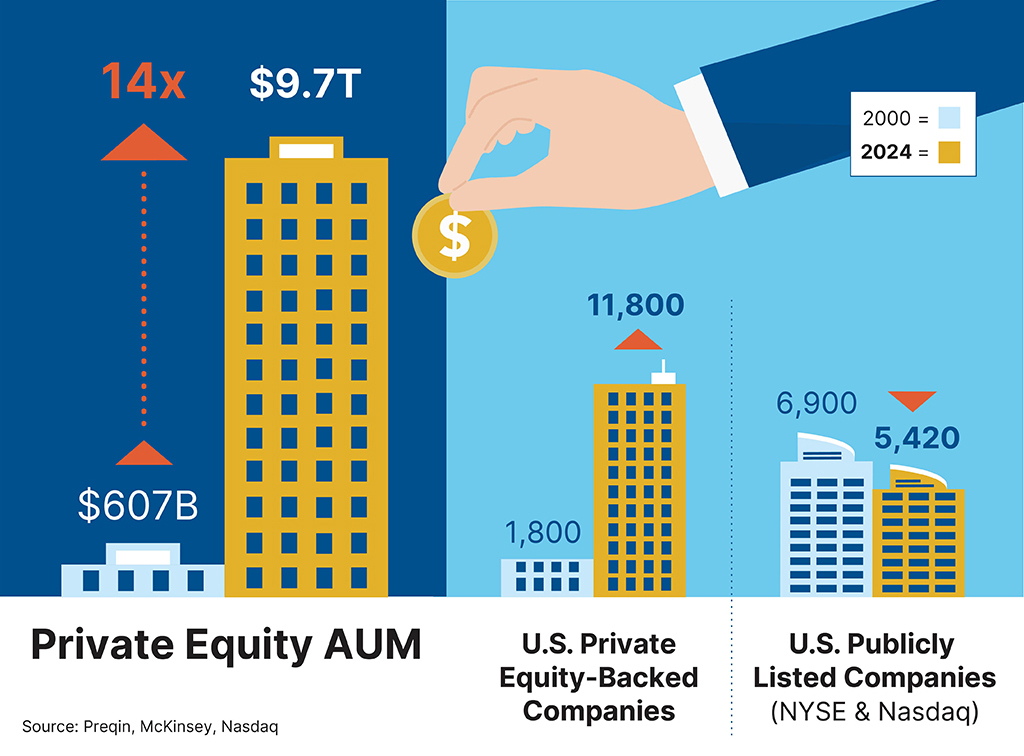

While publicly traded equity and debt markets receive far more media attention, private markets have rapidly grown in both size and importance in recent years. A recent study by Preqin found that private equity (PE) assets under management increased from $607 billion in December 2000 to $9.7 trillion by September 2024, or a roughly 16x increase. Similarly, PitchBook found that the number of U.S. PE-backed companies grew from roughly 1,800 in 2000 to nearly 11,800 in 2024, while the number of U.S. firms publicly listed on the NYSE and Nasdaq fell from roughly 6,900 to about 5,420.

A recent study by Preqin found that private equity (PE) assets under management increased from $607 billion in December 2000 to $9.7 trillion by September 2024, or a roughly 16x increase. Similarly, PitchBook found that the number of U.S. PE-backed companies grew from roughly 1,800 in 2000 to nearly 11,800 in 2024, while the number of U.S. firms publicly listed on the NYSE and Nasdaq fell from roughly 6,900 to about 5,420.

Our Investment Research Group, which oversees asset allocation, manager selection and monitoring, and risk management across the Capital Partners investment platform, believes that systematically allocating capital to top-tier private market investments can be additive to many of our clients’ portfolios.

Why invest in private markets?

At a fundamental level, investing in private markets allows investors the chance to earn an illiquidity premium over marketable securities with comparable risk. We think critically about the opportunity cost of deploying our clients’ capital in any investment. If we are investing in private markets, where clients would have less liquidity relative to public markets, we always consider whether there is adequate compensation for capital lockup.

Fortunately, private markets provide several opportunities to earn incremental returns that are not available to public market investors. Some of the areas we find attractive include PE, venture capital, direct lending (i.e., private credit), real estate, and distressed debt (i.e., private debt). While we invest in each of these strategies, in the following sections we’ll focus on PE, as it is our largest private markets allocation.

Access to a larger universe of high-quality opportunities

Private markets are home to a rich and diverse set of investment opportunities that do not trade in the public markets. For example, while private businesses are typically smaller compared to their public peers, they can exhibit the same high-quality characteristics that market participants traditionally associate with large publicly traded companies.

Private companies can offer mission-critical products or services, are often market share leaders in their industries, and can exhibit attractive unit economics paired with the potential of high returns on invested capital and long runways for growth. The combination of these attributes can allow investors the opportunity to find unique private company investments and generate alpha.

Overall, we believe the PE market’s investable universe offers businesses of comparable quality to our public market investments. It also benefits from differentiated opportunities for value creation including sourcing, structuring, and operational expertise.

Adding value from sourcing and structuring

PE managers must independently source and structure their investments, which creates challenges as well as opportunities. For example, sourcing expertise can add value if a manager is able to engage a company’s management team on a potential acquisition before other buyers are even aware that the business is for sale. In other words, the information asymmetry in private markets makes these undiscovered opportunities and corresponding off-the-run transactions possible. There is no comprehensive list of all private businesses, much less a list of all private businesses up for sale. Therefore, in these instances, buyers will face less competition for the assets, an advantage that often leads to a better price.

Another aspect of private market value creation and risk management is the ability to negotiate the terms of the investment, which includes the potential to better align the management team’s incentives with the fund’s interests. In the public markets, investors must accept the terms of the security as written, and changing management incentives often requires a successful activist campaign or proxy fight.

Ability to earn returns from operational expertise

PE managers with unique industry relationships and expertise can add value for investors both on the initial identification of deals and by creating value in the company post-close. An experienced PE investment team with deep skills in a specific industry can often prove to be a more capable partner relative to a purely financial buyer trying to earn returns from financial engineerin.1 In such instances, management teams may be willing to select the PE partner that can provide the best resources or dilute their equity ownership more than they otherwise would, while simultaneously leveraging its operating expertise to drive outsized growth and operating efficiency over the longer term.

One such common resource is operational expertise. PE teams of all sizes build out internal teams comprising former management consultants who have the time and expertise to improve a business’s pricing strategy, increase factory productivity, or source talented executives. In fact, in 2017, Yale University CIO David Swensen referred to PE as a “superior form of capitalism,” in large part due to the ability of talented teams to make a company better during their hold period.

Flexibility in capital deployment

By virtue of the closed-end structures that are used in private equity funds, general partners (GPs) have the flexibility to call capital from limited partners (LPs) when compelling opportunities present themselves. Conversely, they can shrink their capital base by being net sellers of assets when market valuations are rich.2

In order to fully benefit from this dynamic, LPs must have a plan to efficiently fund future capital calls and must also be prepared to reinvest distributions in a timely manner into other suitable investments. Savvy public markets investors can accomplish something similar. However, the contractual capital commitments that LPs make to private funds often enable these investors to quickly take advantage of attractive opportunities.

The option value of committed (but uncalled) capital can be another important driver of returns, though it is often realized in an irregular fashion as market cycles present attractive dislocations between the price and value of assets.

How does one invest in a private market fund?

In contrast to public market funds that typically have liquid and open-ended structures, investing in private market funds is a long-term endeavor that requires disciplined and active management. Private fund lives are typically 10 years at a minimum and are broken into three different periods: investment, harvest, and divestment.

- Investment Period

- Harvest Period

- Divestment Period

The investment period is typically the first three to five years of the fund’s life, during which the GP sources, diligences, and acquires its portfolio companies. The fund calls the LPs’ capital as each company is added to the portfolio. Depending on the strategy, additional capital may be required to acquire a complementary business or to complete other strategic operational initiatives.

The time from investment to exit (or divestment) is the harvest period. During this period, the GP is focused on optimizing and growing the businesses. Typically, the portfolio companies’ management teams and the GP work hand in hand to execute their value creation plans.

During this time, portfolio companies may require incremental capital or distribute profits and income. Eventually, investor cash flows transition from negative to positive as the portfolio companies require less investment and begin distributing cash back to investors.

The conclusion of the harvest period is marked by the sale of portfolio companies, known as the divestment period. The sale proceeds, inclusive of invested capital and market appreciation, are returned to the fund.

How does one understand the cash flow dynamics of private funds?

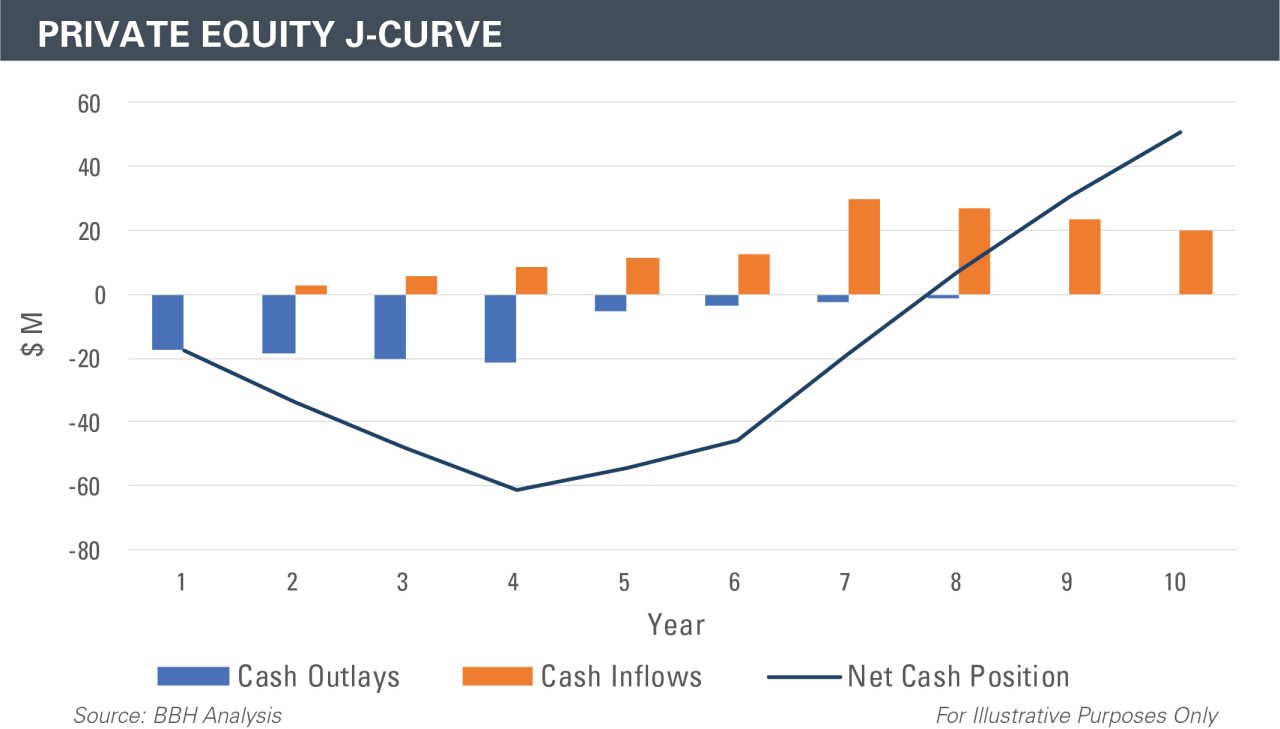

Private market funds’ cash flow often follows a unique pattern referred to as the J-curve. As seen in the nearby chart, a fund investor’s net cash position (blue line) is the sum of the fund’s cash outlays (blue columns) plus cash inflows or distributions (orange columns). The investor’s net cash position with respect to the fund is subject to a “J-curve effect,” where capital is called early in the fund’s life, after which it takes several years for investors to receive enough distributions to reach a breakeven cash position and eventually realize a positive return. The final net cash flow to investors will be unknown until the fund’s final position is exited and the proceeds are distributed to investors.3

| Year | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

| Cash Outlays | -17.5 | -18.75 | -20 | -21.25 | -5 | -3.75 | -2.5 | -1.25 | 0 | 0 |

| Cash Inflows | 0 | 2.625 | 5.4375 | 8.4375 | 11.625 | 12.375 | 29.6875 | 26.6875 | 23.5 | 20.125 |

| Net Cash Position | -17.5 | -33.625 | -48.1875 | -61 | -54.375 | -45.75 | -18.5625 | 6.875 | 30.375 | 50.5 |

Interestingly, as seen above, an investor’s capital at risk rarely reaches the level of his total fund commitment due to the early distributions in a fund’s life. In other words, the fund will return capital from dividends, asset sales, or recapitalizations from existing portfolio companies while continuing to make new investments.

Notably, these distributions do not require an outright sale of the investment – in a dividend recapitalization, for example, an investor can reduce the amount of his equity at risk but still compound capital through continued ownership of the business or property. In some successful transactions, the fund can even return its entire cost basis in the investment to LPs while maintaining ownership, which is akin to “playing with house money.”

Due to the regular return of capital, clients in most instances will not have more than 75% of their fund’s commitments invested, despite having 90% or more of their commitments called. The practical takeaway is that the investor must commit more capital to private markets than she intends to have invested at any time.

How does one construct a private markets portfolio?

A single private fund investment does not make a mature private markets portfolio. Unlike public market funds that reinvest capital following the sale of a stock, private funds return capital to investors when they sell an investment, which means these investors must commit to new funds to maintain the same level of exposure.

An example: the impact of investment periods and market environments | |

Investment period | Market environment |

Like all investing, private market returns will differ depending on the periods in which they are made. For example, many PE funds that deployed large amounts of capital in 2006 through 2008 struggled to meet their return targets, as they were investing into highly priced assets ahead of the financial crisis. In contrast, 2009 vintage PE funds posted extremely attractive returns, on average. | Similarly, the performance of different strategies can vary depending on the market environment. Distressed debt, for example, is more countercyclical and allows investors to deploy capital into different assets and market environments than PE, which is more procyclical. |

While it is difficult to predict the period that will result in the most optimal environment for deploying capital, we believe that to be a successful private market investor, it is critically important to remain a consistent, methodical allocator to private markets across both vintage years (year of the fund’s initial investment) and asset classes. It is also important to invest with funds managed by GPs who respect valuation and a strong alignment of interest with the LP.

How much should one invest in private markets?

In short, an allocation to private markets should be large enough to make a difference to the overall portfolio’s return (at least 5% to 10%), but not so large that the illiquid portion of the portfolio and unfunded capital commitment create unintended liquidity concerns.

As a private markets portfolio matures, it is often possible to fund capital calls for newer funds with distributions from maturing funds. While these cash inflows and outflows will never match exactly, a mature portfolio should exhibit these self-funding characteristics in most normal investment environments. However, in extreme circumstances, such as a deep economic recession, divestments slow and capital calls may increase, creating steep funding requirements as portfolio values decline.

As such, we advise clients to be mindful of the liquidity dynamics at play as private markets allocations rise. As illiquidity is a risk that rises in importance during a bear market, it is helpful to look at the impact of a large private market allocation during a bear market scenario, as illustrated in the following table.

| Private Markets – Bear Market Allocation Scenario | |||

|---|---|---|---|

| Starting Weight | Bear Market Return | Ending Weight | |

| Public Equity | 65% | -50% | 51% |

Private Markets | 20% | -20% | 25% |

Fixed Income | 15% | +5% | 25% |

| Unfunded Commitments | 7% to 9% | 15% | |

| Private Markets Exposure | 20% | 25% | |

| Total | 27% to 29% | 40% | |

| For illustrative purposes only | |||

Since marketable equities typically experience steeper mark-to-market declines during bear markets, a portfolio initially allocated 65%/20%/15% to public equity, private markets, and fixed income, respectively, would emerge from a steep downturn at roughly 51%/25%/25%.

In the same portfolio, unfunded commitments, a fixed dollar amount that initially represented 7% to 9% of the portfolio, would increase to 15% of the client’s assets. Total private markets exposure and unfunded commitments could increase from a normal portfolio weight of 27% to 29% to as high as a 40% weight in a drastic scenario like this one.

Consider what happened to several endowments during the 2008 global financial crisis. As many of these institutions overallocated to private investments, their private markets exposure and unfunded commitments increased to uncomfortably high levels. As a result, many institutions put pressure on private fund managers to reduce or release commitments due to concern about the lack of liquidity in their portfolios. Moreover, institutions were forced to borrow to fund potential commitments. Today, top institutions track unfunded commitments closely and have robust plans for funding these calls when they come due.

Going into a downturn with an overallocation to private markets virtually eliminates the investor’s ability to allocate capital to once-in-a-cycle opportunities in the public market or new private market opportunities that emerge at the end of a downturn. Many sophisticated investors stood on the sidelines in 2009 as others with more liquid portfolios took advantage of extraordinary investment opportunities. We prefer that clients’ portfolios have adequate liquidity to increase equity risk in either public or private investments when the right opportunity is presented.

While aggressive private markets allocations may be more palatable to some growth-oriented investors, the risk of being overallocated to the private markets underscores our conservative approach to portfolio construction.

With that said, we work hand in hand with each client to better understand their liquidity preferences, spending needs, and time horizons to determine an appropriate long-term private markets allocation.

Conclusion

At BBH, we believe that systematically allocating to private markets can benefit client portfolios. When done correctly, investing in private markets exposes client portfolios to a rich universe of high-quality investments that are not available in the public markets. PE allocations must be managed carefully, however, and clients must ensure they are diversified across both vintage years and strategies while paying particular attention to the amounts they commit.

We focus on all of these dynamics before recommending a new private fund for suitable clients, and BBH relationship managers are always available to help clients through the process of building exposure to these illiquid assets over time.

If you would like to learn more about our approach to private markets investing, please reach out to a BBH relationship manager or a member of our Investment Research Group.

Contact Us

1 Generally, financial engineering in private equity means levering the company with excessive amounts of debt

2 The general partner is a part owner and manager of the investment partnership and has discretion to make investment decisions on behalf of the limited partners. Limited partners are investors or “silent” partners in an investment partnership.

3 When an investor breaks even, the realization multiple of distributions/invested capital equals 1.00x.

Private market funds are only available to qualified investors. Generally, they would include persons who are “Qualified Purchasers” for the purpose of the Investment Company Act of 1940 and “Accredited Investors” for the purpose of the Securities Act of 1933 and non-U.S. Professional Investors. Additionally, an investor in a private market funds should be aware that they will be required to bear the financial risk of this investment for a significant period of time.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved. PB-08562-2025-05-12