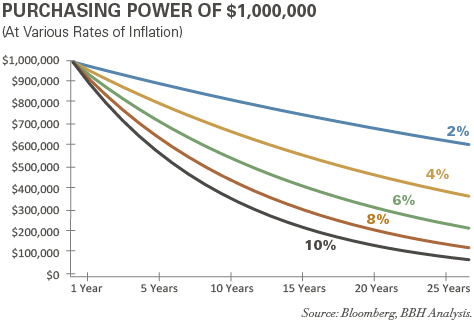

We are deluged with information. Richard Saul Wurman, the godfather of information architecture, calculates that there is more information in a single issue of The New York Times than the average citizen in the 17th century would have been exposed to in his lifetime. And that calculation doesn’t even take into account the proliferation of new technology and the explosion of information available through new media. The issue is particularly acute for investors, who can access up-to-the-minute stock quotes on their iPhones, check the value of their portfolios on an iPad and choose from a multitude of television shows, magazines and newspapers to bathe in the information stream of financial markets, economies and politics. Shortage of information isn’t the problem – shortage of insight is.

Recent years have offered no respite from these maladies, and the future looks no more likely to. Volatility has returned to financial markets, geopolitical uncertainty abounds, inflation is picking up, and interest rates are rising as well. Recently, tax reform, the threat of a trade war and the implications of budget agreements have all competed for investors’ attention, making it increasingly difficult to glean meaning from a cacophony of headlines. This distinctly modern challenge is known as information overload, a condition where the presence of too much information obscures what is genuinely important, leading either to the inclination to react to each and every new data release, or, at the opposite extreme, do nothing and succumb to paralysis. Clay Shirky, a thinker and writer on the broad subject of the role of technology in society, claims that there is actually no such thing as information overload, only filter failure. So what filters should investors have in place to enable them to hear the signal through the noise and not be distracted to their own detriment?

We offer in the following pages a series of related bedrock beliefs that help guide our own thinking about investing, whether at the level of asset allocation, security selection or the identification of third-party managers we engage to help manage our clients’ assets. We believe that these investment tenets are important in any environment but critical in one characterized by heightened uncertainty.

Risk is not volatility.

One of the cornerstones of modern portfolio theory is that risk is defined as volatility and that the primary objective of portfolio management is to minimize that risk for a particular level of desired return. On initial consideration this makes sense, as exaggerated volatility of market returns is certainly unappealing to most people. Yet on second thought, most investors like upside volatility – it’s the downside volatility they can do without. So we find that the fundamental assumption of modern portfolio theory is imperfect at best, and one that we do not share. Make no mistake – volatility is not a desirable state of affairs, but in our opinion, the real definition of investment risk is the possibility of permanent loss of capital: losing money and not getting it back.

Indeed, for the disciplined investor, volatility is an essential contributor to investment success. Price volatility creates the opportunity for a patient investor to acquire a security at an appropriate discount to intrinsic value.1 That discount creates a margin of safety,2 or a valuation cushion, should unanticipated changes occur, either at the level of the company or issuer, or in the broader investment environment. At the same time, upside price volatility requires the discipline to sell securities – even ones with good fundamentals – if a rally pushes the price beyond the intrinsic value of the asset.

If anything, a lack of volatility can also present a serious risk, as it indicates a degree of complacency that can magnify the reaction of a market or specific security to adverse developments. As an example, consider the long stretch of price stability that characterized the equity market just before the onset of the Great Recession. On average, the S&P 500 experiences about 22 days a year in which the index moves by more than 2% in either direction.3 From 2004 through 2006 – a three-year period – the market only had two such days. Complacency reigned as imbalances built, bubbles inflated, and investor sentiment implied that nothing could go wrong. Of course, with the benefit of hindsight, we know that a lot did go wrong, and the market’s complacency in advance of that exacerbated the severity of the bear market that followed. On a smaller scale, the market correction in early 2018 followed a similar period of subdued volatility, during which investors underappreciated the rising risk of inflation. We are reminded of Warren Buffett’s admonition that investors should be greedy when others are fearful but fearful when others are greedy.

Price volatility may be uncomfortable and undesirable, but it’s not the best definition of investment risk, and it can even act as a complement to a value-based approach to investing.

Price and value are different things.

The concept of price has wonderful characteristics: It has the advantages of availability, transparency and frequency. Functioning markets and rapid reporting mean that we can usually all agree on the price of a security. Prices change constantly, and those changes are updated instantly on a variety of pricing sources, widely available to professional and personal investors alike. The problem with prices, as outlined in the previous section, is that they can be quite volatile.

Value, on the other hand, has the mirror attributes of price. Value is not transparent, available or frequent, but because of that enjoys less volatility. Whereas an investor can watch the price of a stock change throughout the course of a trading session, the value of the underlying company is only derived through patient and careful analysis and is therefore a far more robust notion than price. Benjamin Graham elegantly framed the distinction between price and value by noting that in the short run the market is a voting machine, whereas in the long run it is a weighing machine. The “votes” of countless traders determine price day to day, and second to second. Weighing the underlying economic viability and free cash flows generated by a business determines value, a far more durable concept. Investors primarily interested in the preservation and growth of their wealth over the long run are better off focused on value than price for precisely these reasons.

Price and value are obviously interconnected concepts, but investors should keep the relationship in perspective. Investing based on value acknowledges the volatility of prices but further recognizes that price volatility merely creates the opportunity to acquire fractional shares in a business at an appropriate discount to the underlying value of the company. An investor who makes price her sole or primary investment variable is like a man searching for his missing car keys underneath a street lamp because the light is better, not necessarily because the keys are there. Price is transparent, but true value is rarely discovered underneath the street lamp.

Investors must know what they own.

In order to assess the risk of permanent impairment to capital or the intrinsic value of an investment, an investor first must understand it. This requires significant research into the security, enterprise and industry under consideration for a direct investment or a deep understanding of the investment philosophy and approach when engaging a third-party manager. Without knowing what you own, it is nearly impossible to handle the information overload – to distinguish between developments that meaningfully affect the intrinsic value of the underlying investment and those that merely move the price for a shorter period of time. Even if the distinction can be made, without a deep knowledge of the investment, it is challenging to determine whether a price movement adequately reflects a possible change in underlying value. In the absence of this insight, volatility ceases to be an opportunity and becomes an enemy once again.

There are at least two strong implications that follow from the idea of knowing what you own. First, it does not make sense to invest in securities or portfolios where you don’t have visibility into the investment rationale, process or holdings. When performance is weak and very little is known about the underlying causes, what is an investor to do? Buy more because it’s cheap? Sell before it falls further? Ignorance of the underlying fundamentals leaves only emotion as a driver of action, and hope and fear make for poor investment strategies. We prefer to rely on analysis and conviction when others are buying and selling based on emotion.

Second, holding too many investments prevents an investor from knowing them well enough. Portfolios should be appropriately diversified but can easily become overdiversified, thereby introducing the risk of not developing adequate knowledge of and conviction in what is owned. Maintaining a degree of concentration in the number of investments allows an investor to dig deeper into each one, which will serve her well when price volatility inevitably tests her convictions.

There is no such thing as passive investing.

In an attempt to avoid underperforming the market over any time period – short or long – many investors shun active investing in favor of the apparent safety of passive, or index, investing.