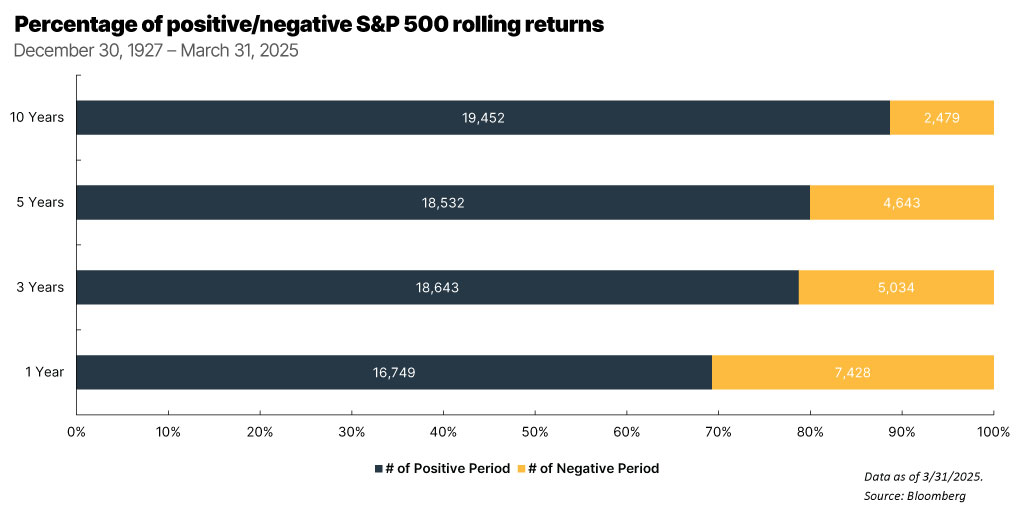

The temptation to time the market – jumping in and out based on short-term moves – can be strong, especially in periods of uncertainty. However, history continues to show that successfully predicting market returns is exceptionally difficult, and missing just a handful of the market’s best days can significantly impact long-term returns.

We believe that market timing is not a reliable investment strategy. Instead, staying invested through market cycles and maintaining a disciplined long-term approach, staying diversified, and ensuring portfolios are resilient across different market conditions remains the best way to build wealth over time.

What is market timing?

We define market timing as the speculative strategy of making buy or sell decisions based on predictions of short-term market price movements. Importantly, market timing decisions are based on estimating the returns of the market (or corresponding index), such as U.S. large cap stocks, rather than a particular security.

Market timing strategies can involve several different approaches. One approach employs using nonfinancial indicators to predict market movements. For example, one may attempt to predict what may happen to U.S. equity markets if a given presidential candidate were to win an upcoming election. Such an investor may determine that the risk of an unfavorable candidate winning the election warrants staying out of the market until the election is resolved.

Another approach involves the use of technical indicators, such as historical stock prices. In this case, an investor might notice that the MSCI ACWI has generated positive returns for the past five years and may decide to wait for the “bubble” to burst.

Yet another common approach is timing based on historical market valuations. An investor utilizing this approach might make valuation comparisons across time or different markets. While keeping track of these data points can be helpful, attempting to base entry or exit decisions on them may be detrimental to long-term returns. There are too many other variables that influence market returns over the short to medium term, and it’s difficult for anyone to make accurate predictions on macro issues over a long period of time.

Time in the market vs. timing the market

Of course, investors would love to be able to time the market perfectly, investing at market bottoms and moving to cash at peaks. Unfortunately, such market timing is challenging for all investors, no matter how sophisticated. We adhere to the adage that “it is about the time in the market, not timing the market” that allows investors to best position themselves for strong long-term results. A long time horizon that benefits from the power of compounding is much more impactful, and generally more successful, than the mirage of market timing.

Instead of trying to time the market by monitoring broad market, economic, or political indicators, investors should utilize a bottom-up, fundamental approach with a long-term horizon to select high-quality individual securities trading at a discount to estimates of intrinsic value.3 Such an approach is the most reliable way to generate attractive long-term returns. In addition, investors are also well served by implementing a rebalancing strategy that optimizes the benefits of such actions without the potential tax consequences.

What is the allure of market timing?

Despite the abundance of evidence suggesting that market timing is a futile exercise, its allure persists. Why? One hypothesis is that this strategy is a response to the legitimate realities of investing as well as behavioral biases. Specifically, all investors can see how beneficial it would be if they could predict market movements and adjust a portfolio in advance of those movements. Doing so would allow one to dramatically outperform the gold standard of a buy-and-hold strategy over the long term.

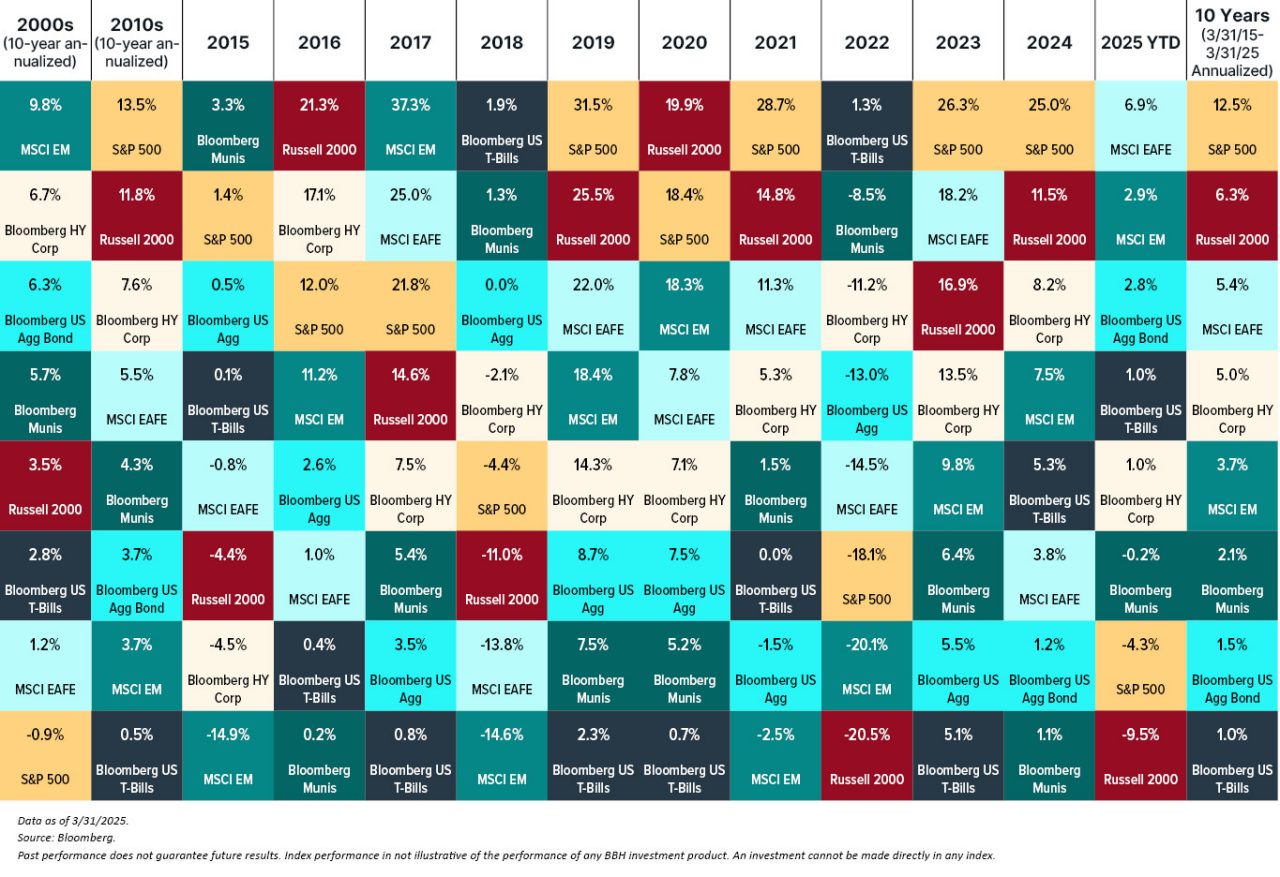

Looking at the following chart, the “all-knowing” investor would have moved out of developed international and into small-cap equities at the end of 2015, only to rotate into emerging market equities at the end of 2016. In theory, that investor would be able to generate returns at a level rarely attained.