ROIC multiplied by reinvested capital equals value created flowchart

In previous articles, we’ve described why Brown Brothers Harriman (BBH) tends to reject the traditional investment taxonomy of “value” vs. “growth.” In our opinion, all good investing is (or should be) value investing, and all businesses – whether fast or slow growing, cyclical or stable – should be purchased with reference to the gap between market price and a conservative intrinsic value estimate.

That is why we prefer to use portfolio company quality as the primary touchstone when evaluating businesses and other investors. However, this mental model invites another contentious debate: What is the necessity of business quality, and what does “quality” mean in the first place?

A Brief History of Quality Investing

Warren Buffett and the late Charlie Munger have long been considered the primary evangelists of “quality investing.” However, this was not always the case: During the late 1950s and early 1960s, while managing his original, eponymous partnership, Buffett adhered mostly to Benjamin Graham’s deep value philosophy. Graham’s approach, also known as “cigar-butt” investing, used balance sheet metrics to identify statistically cheap companies with re-rating potential. Little emphasis was placed on the long-term prospects of the businesses in question.

As time went on, however, Buffett evolved. In his 1989 Berkshire Hathaway shareholder letter, he reflects:

Unless you are a liquidator, that kind of approach to buying businesses is foolish. … [N]ever is there just one cockroach in the kitchen, [and] any initial advantage you secure will be quickly eroded by the low return that the business earns. … Time is the friend of the wonderful business, the enemy of the mediocre.

What caused this revelation? In part, increased market efficiency. As screening technology improved and professional investors proliferated, statistically cheap “net-net” stocks dwindled in number and size, becoming an unrealistic vehicle for Buffett’s increasingly large pool of capital.

Buffett was also influenced by Phil Fisher, who published “Common Stocks and Uncommon Profits” in 1957, and Munger. In his 2014 letter, Buffett writes: “It took Charlie Munger to break my cigar-butt habits … The blueprint he gave me was simple: Forget what you know about buying fair businesses at wonderful prices; instead, buy wonderful businesses at fair prices.”

By the time Buffett met Munger in 1959, Fisher had already pioneered the idea of owning excellent businesses for the long term; at Berkshire Hathaway, the two combined Fisher’s proto-growth philosophy with Graham’s valuation discipline to become the investing juggernaut they are today.

Defining Quality

What makes something a “quality” business? As a starting point, we return to Buffett, this time writing to Berkshire Hathaway shareholders in 1996: “Your goal as an investor should simply be to purchase, at a rational price, a part interest in an easily-understandable business whose earnings are virtually certain to be materially higher five, 10, and 20 years from now.”

The core measuring stick depicted here should be clear: A quality business is one that can meaningfully grow its earnings over time. However, there are several additional characteristics: A quality business is one that can grow earnings over time, for a long time, with a high degree of predictability.

Before exploring each qualifier, we must establish what gives companies value in the first place: cash flow. Consider the following example: If you, a private business owner, purchased a company that you could not sell for 20 years, you would derive value solely from the owner earnings that accrued to your bank account over time. Your returns, meanwhile, would be measured based on the size of those cash flows relative to the original acquisition price. You could choose whether to let your cash profits accumulate or to reinvest and grow the business, but your operating results would reflect the impact of these decisions. Over the truly long term, given a rational purchase price, the market values public companies in much the same way.

A quality business is one that can grow earnings over time, for a long time, with a high degree of predictability.

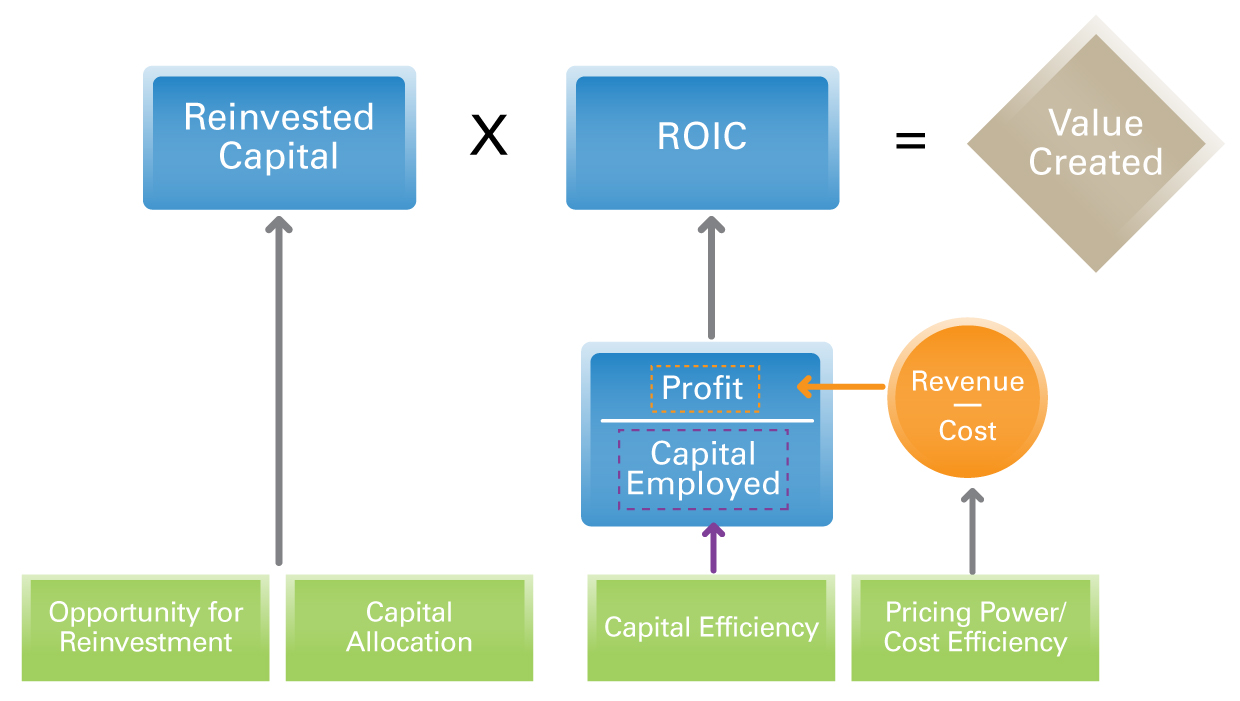

With this definition in mind, we can trace new value creation to its most fundamental components: reinvestment and return on invested capital (ROIC). ROIC reflects profit (or in a growth scenario, incremental profit) and the capital required to generate that profit. Profit, in turn, is a function of revenue and cost. It follows that highly profitable, high-return businesses must therefore maintain an advantage in either pricing power or cost/capital efficiency – and must make sound capital allocation decisions to reinvest capital at similarly high rates to grow.

The following section examines these key drivers as well as several of the competitive advantages, commonly known as “moats,” that enable companies to maintain and grow their intrinsic value over time.

As depicted in the nearby graphic, the “R” in ROIC represents some measure of profit. There are two primary levers a business can pull to increase profitability: pricing power and cost efficiency. Advantages that enable businesses to exert pricing power include:

- Innovative/desirable products and services: Perhaps the most common source of pricing power is the ability to provide a product or service that customers value more than others. Such products can be vertically differentiated (objectively better – like a computer with more processing power) or horizontally differentiated (subjectively better – like the aesthetic appeal of an iPhone). In both cases, customers convinced of this differentiation are typically willing to pay more for it.

- Essential products and services: Certain products are required for individuals and enterprises to function. Pricing power therefore results from the demand inelasticity of customers: Whereas most people might decide to take fewer cruises if they became too expensive, restraint is less realistic in the case of basic food items, trash collection, or lifesaving medicine. These products understandably command pricing power – ideally within reason – due to their everyday necessity.

- Brand/customer loyalty: Brand loyalty helps products in the two previous categories exert additional pricing power, even when little actual difference exists between competitors. This is arguably even more important for interchangeable consumer staples, like deodorant or dog food. While the product class itself may be essential, superior brand loyalty is what allows certain producers to escape price competition and raise unit prices.

- Switching costs: This powerful moat occurs when the inconvenience or difficulty of changing service providers outweighs any potential changes in consumer preference. Switching costs apply to most enterprise software solutions: Once a large organization has taken pains to implement a new payroll or accounting platform, the prospect of repeating the process for anything less than a far superior competitor becomes unappealing, leading to strong customer captivity and price tolerance.

- Network effects: Two-sided platform businesses, social media sites, and other customer “ecosystems” benefit from demand-side economies of scale, where a given service’s utility increases with each additional user. Beyond a certain tipping point, these network effects create extensive customer captivity: If Sotheby’s and Christie’s attract the greatest number of high-quality sellers and bidders of any auction house, it makes sense for prospective new sellers and bidders to also choose their services, even if prices are higher.

In addition to these more top-line-oriented moats, other competitive advantages allow businesses and industries to operate at lower cost than their competitors:

- Unique resource captivity: While undifferentiated commodity producers are not often considered quality businesses, exceptions exist in the case of those with access to one-of-a-kind resources that allow them to produce at much lower cost. Israel Chemicals (ICL), for example, “mines” potash and bromine from the bottom of the Dead Sea, which is far cheaper than traditional terrestrial extraction methods; as a result, ICL sits at the bottom of the fertilizer cost curve and can price below competitors while remaining profitable.

- Economies of scale: Dominant size within relevant markets can confer valuable scale advantages in several ways. Walmart, as the largest customer of its smaller, more fragmented suppliers, wields immense negotiating power that keeps costs low. Meanwhile, high-volume players in any industry requiring large startup investments and fixed costs will benefit from the flywheel of scale: By producing or selling more than a competitor with the same fixed cost base, high-scale businesses will have better margins and, in turn, more money to spend on research and development and marketing to further widen their lead.

- Scalable products: Some products/services are inherently more scalable than others. Whereas even a high-scale hardware company will still have considerable variable costs – additional materials will be needed to make more widgets – once an IT company has built its core software product, it can sell additional “units” ad infinitum at little to no additional cost.

- Lean culture/business models: Finally, there is nothing like good old-fashioned frugality, whether through cost-conscious culture (Buffett himself operates with a tiny corporate staff in Berkshire Hathaway’s Omaha, Nebraska, headquarters), lean manufacturing innovation (Toyota’s famous Kanban inventory control system made it the giant it is today), or both.

These operational characteristics allow certain high-quality companies to be more profitable than others, putting the “R” in ROIC. The role of the “C,” meanwhile – the working capital and capital expenditures required to generate these profits – completes the picture.1

Some businesses are naturally more capital intensive than others; in addition to their expenses, such companies must invest heavily in expensive assets in order to operate. On the other hand, capital-light companies require far fewer assets to realize equal or superior profits. For example, traditional hardware-producing businesses must invest in expensive machinery and a large factory, both of which require periodic repair and replacement. They must also tie up cash in assets like inventory. Software companies, by contrast, might have close to zero major physical assets – their products and, by extension, revenues are the result of primarily intellectual labor.

Some businesses even operate with negative working capital, meaning they receive upfront payments for their services, which can be used to self-finance the company absent any external investment. As an insurance company that collects “float” from customer premiums, Berkshire Hathaway is a textbook example. Although capital expenditures do not immediately affect net income (they reduce accounting earnings over time via noncash depreciation), capital spending requires cash – so all else being equal, capital-light businesses will create more value.

A business with a legacy moat and high historical ROIC is all well and good, but without the continued ability to compound value at high rates of return, great companies will quickly become stable, static cash cows – and ideally, we would like our owner earnings to grow over time. Thus, high-quality companies must also possess the potential for returns on new invested capital, which requires the following:

- Opportunities for reinvestment: To keep growing, dominant companies need room to expand. These opportunities can come in the form of vulnerable competitor market share, new markets to tap, new products to bring to market, or accretive acquisitions. Weak legacy substitutes, rather than competing products with similar functionality, often provide the most appealing opportunities.

For example, Visa and Mastercard – excellent companies with market capitalizations worth hundreds of billions of dollars – nevertheless still have immense runways for growth as cash usage fell 8% globally in 2023 and is expected to decline at a 6% compound annual growth rate (CAGR) through 2027.

- Skilled capital allocation: Opportunities for reinvestment have little value if management cannot identify them in the first place. Long-term value creators are typically helmed by astute capital allocators who can go where the returns are – as well as avoid where they are not – by buying back shares at low prices, paying dividends, or simply preserving cash in the absence of compelling reinvestment opportunities.

- Long-term orientation and incentive alignment: Operating successful franchises requires a long-term view. While quality investors may disagree about the necessity of near-term profitability, all would likely acknowledge that the best business owners think far beyond quarterly earnings. The best external enabler of such long-term thinking is proper incentive alignment: When management teams are themselves large shareholders with substantial portions of their net worth invested in the company, there is far less temptation to mortgage the company’s future to temporarily boost short-term results.

The thoughtful pursuit of growth is easier said than done. To be clear, attempting growth without strong incremental ROICs that surpass the cost of that capital can be deadly – businesses that do so will not only fail to create value, but will in fact destroy it.

It is the crucial combination of high returns and growth that leads to additional value creation, which is why finding talented stewards of capital is such an essential (and often rare) part of successful quality investing.

The final component of Buffett’s quality mantra is perhaps the most difficult for investors to gauge. What company, if any, can generate 20 years of “virtually certain” earnings growth? Numerous first-moving, otherwise high-quality companies have dominated their respective industries for years, only to be quickly upended due to a major technological disruption or change in consumer sentiment (for example, Gillette, Research in Motion, Blockbuster, Kodak, and Yahoo).

For an investor hoping to own a company for five, 10, or even 20 years, it is essential to identify not only a large competitive position, but also a durable one that can prevent excess returns from being unexpectedly captured by new entrants.

Contributors to durability include the “customer captivity” moats explored earlier.

- Incumbent structural advantages like network effects and high switching costs can prevent new entrants from reaching scale.

- The sale of essential goods and services reduces the odds that a fleeting new substitute might suddenly render a company’s product obsolete.

- Industries involving more mature technologies invite less disruption: It is much more difficult to imagine an overnight revolution in the trash collection business than in computing memory or semiconductors.

- Recurring revenue business models are also valuable because they allow companies to reliably extract revenues monthly or yearly without repeat customer acquisition efforts. By contrast, a company that sells one-off products must recompete for every sale, leading to far less predictable business, particularly in the absence of other competitive advantages.

Profitability, growth, and predictability – this is by no means an exhaustive list. Strong balance sheets, honest management, and many other traits can be important components of quality as well. Ultimately, all contribute to a business’s ability to consistently compound earnings at high rates of return and create shareholder value.

Why Does Quality Matter?

While high growth, high margins, and high returns on capital are obviously appealing attributes, there are plenty of high-quality companies that have made for lousy investments and plenty of low-quality companies that have made their investors very wealthy. Without considering the price paid, quality is far from a guarantee of positive returns.

For argument’s sake, however, let’s suppose we are confident in our ability to buy high-quality companies at prices that enable returns approximating long-term operating performance. Even then, it is worth asking why we choose to seek returns this way.

First, quality businesses that compound intrinsic value over time are well-suited to BBH’s long-term disposition. Purchased at the right price, such investments can experience share price appreciation for many years without losing their margin of safety. By definition, such holdings tend to be lower turnover, allowing investors to defer taxes and minimize transaction costs. This low-turnover approach also eliminates the need for constant idea replenishment, which in higher-activity strategies often strains analyst bandwidth and the opportunity set available in the market at any given time.

High-quality businesses can also be more resilient in the face of economic recession. Their essential products, lean cost structures, locked-in customers, and clean balance sheets all increase the likelihood of survival and success following downturns, even if their share prices become temporarily depressed. On the upside, high-quality companies run by excellent owner-operators often possess some degree of embedded option value. While we would never predicate an investment thesis on far-off greenfield opportunities alone, great capital allocators and visionary CEOs are more likely to create new value sources over the long term, often in ways that could not have been predicted during the original underwriting.

Clearly, many of the considerations listed in this article – moat durability, management skill, reinvestment runway, and so forth – are more qualitative than quantitative. This subjectivity is part of what makes the market for high-quality companies more inefficient in the short term. Higher frequency, data-driven traders must compete with their peers to glean an edge from objective, ubiquitous information. In contrast, quality investors compete on their ability to better judge a business’s long-term strategy and holistic potential.

Even when a company’s qualitative strengths are clear, patient investors can still arbitrage negative short-term sentiment to buy long-term winners at discounted prices. When buying undervalued but fundamentally weak “cigar-butt” businesses, time is often an enemy rather than an ally, making this approach far less viable.

An emphasis on quality also reduces the likelihood that a portfolio company could implode or lose most of its value due to fraud, disruption, or other types of permanent impairment. This enables investors with the right temperament to build more concentrated portfolios – which, when executed correctly, can amplify returns while reducing risk (in the truest sense of the word – not volatility) compared with diversified, low-conviction portfolios that have been thinly researched.

Finally, we believe quality investing is just plain fun. Noncontrol, nonactivist investors rely on their sourcing ability and good judgment to make successful investments, and we find it stimulating to look for and partner with exceptional owner-operators who oversee unique, advantaged business models, particularly for the long term. To borrow from Buffett one last time, “When we own portions of outstanding businesses with outstanding managements, our favorite holding period is forever.”

To learn more about our approach to quality investing, reach out to your BBH relationship team.

Contact Us

1 For more on this framework and the individual advantages listed, see McKinsey & Company’s “Valuation: Measuring and Managing the Value of Companies,” particularly chapter three, or Michael Porter’s “Competitive Strategy: Techniques for Analyzing Industries and Competitors.”

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2024. All rights reserved. PB-07604-2024-07-23