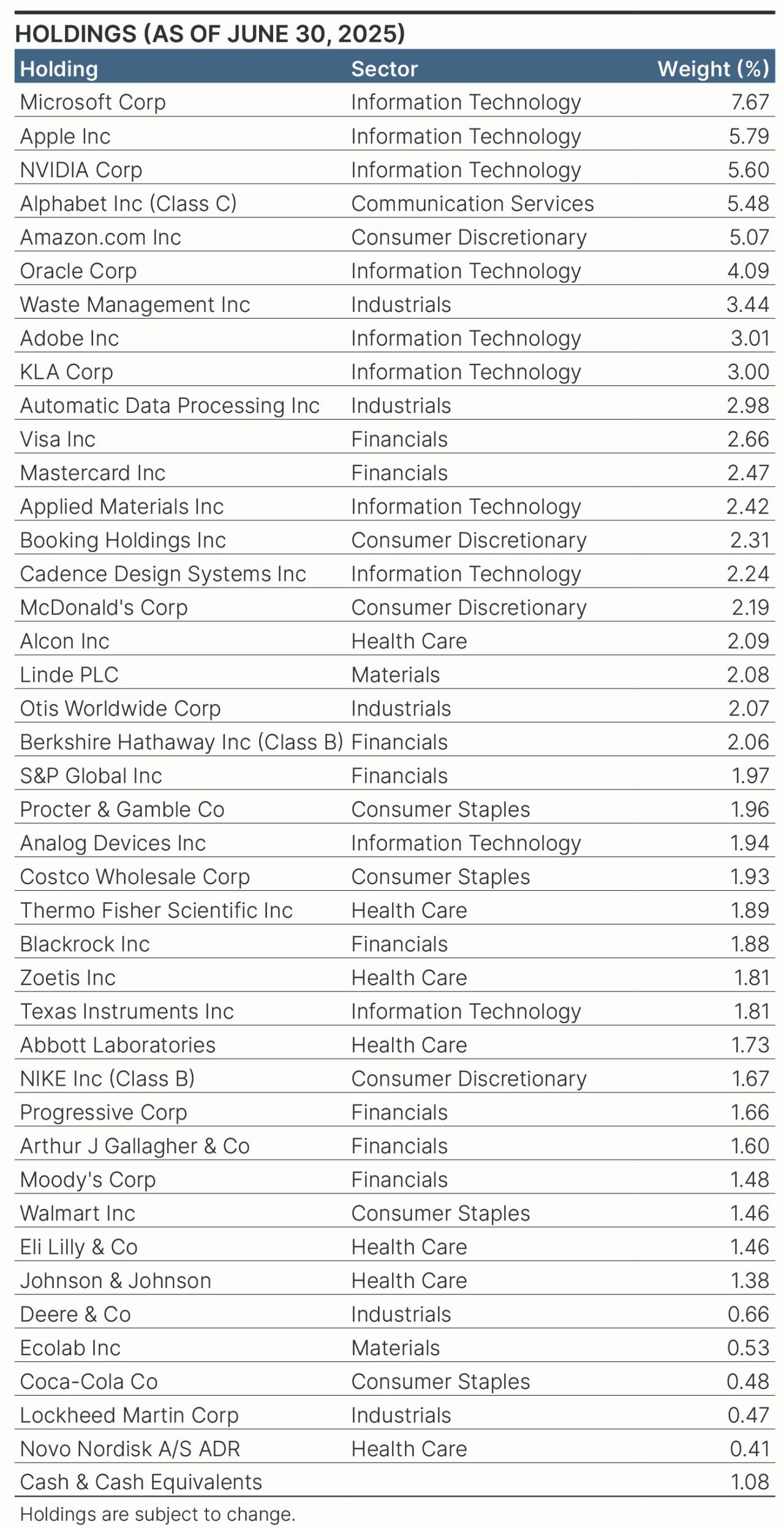

HOLDINGS (AS OF JUNE 30, 2025) |

||||||

Holding |

Sector |

Weight |

|

Holding |

Sector |

Weight |

Microsoft Corp |

Information Technology |

7.67% |

|

Procter & Gamble Co |

Consumer Staples |

1.96% |

Apple Inc |

Information Technology |

5.79% |

|

Analog Devices Inc |

Information Technology |

1.94% |

NVIDIA Corp |

Information Technology |

5.60% |

|

Costco Wholesale Corp |

Consumer Staples |

1.93% |

Alphabet Inc (Class C) |

Communication Services |

5.48% |

|

Thermo Fisher Scientific Inc |

Health Care |

1.89% |

Amazon.com Inc |

Consumer Discretionary |

5.07% |

|

Blackrock Inc |

Financials |

1.88% |

Oracle Corp |

Information Technology |

4.09% |

|

Zoetis Inc |

Health Care |

1.81% |

Waste Management Inc |

Industrials |

3.44% |

|

Texas Instruments Inc |

Information Technology |

1.81% |

Adobe Inc |

Information Technology |

3.01% |

|

Abbott Laboratories |

Health Care |

1.73% |

KLA Corp |

Information Technology |

3.00% |

|

NIKE Inc (Class B) |

Consumer Discretionary |

1.67% |

Automatic Data Processing Inc |

Industrials |

2.98% |

|

Progressive Corp |

Financials |

1.66% |

Visa Inc |

Financials |

2.66% |

|

Arthur J Gallagher & Co |

Financials |

1.60% |

Mastercard Inc |

Financials |

2.47% |

|

Moody's Corp |

Financials |

1.48% |

Applied Materials Inc |

Information Technology |

2.42% |

|

Walmart Inc |

Consumer Staples |

1.46% |

Booking Holdings Inc |

Consumer Discretionary |

2.31% |

|

Eli Lilly & Co |

Health Care |

1.46% |

Cadence Design Systems Inc |

Information Technology |

2.24% |

|

Johnson & Johnson |

Health Care |

1.38% |

McDonald's Corp |

Consumer Discretionary |

2.19% |

|

Deere & Co |

Industrials |

0.66% |

Alcon Inc |

Health Care |

2.09% |

|

Ecolab Inc |

Materials |

0.53% |

Linde PLC |

Materials |

2.08% |

|

Coca-Cola Co |

Consumer Staples |

0.48% |

Otis Worldwide Corp |

Industrials |

2.07% |

|

Lockheed Martin Corp |

Industrials |

0.47% |

Berkshire Hathaway Inc (Class B) |

Financials |

2.06% |

|

Novo Nordisk A/S ADR |

Health Care |

0.41% |

S&P Global Inc |

Financials |

1.97% |

|

Cash & Cash Equivalents |

|

1.08% |

Holdings are subject to change.