Performance |

|||||||

|---|---|---|---|---|---|---|---|

|

Total Returns |

Average Annual Total Returns |

|||||

Composite/Benchmark |

3 Mo. |

YTD |

1 Yr. |

3 Yr. |

5 Yr. |

10 Yr. | Since Inception |

BBH Core Plus Fixed Income Composite (Gross of Fees) |

2.86% |

2.86% |

6.30% |

2.33% |

2.85% |

3.93% |

6.29% |

BBH Core Plus Fixed Income Composite (Net of Fees) |

2.80% |

2.80% |

6.03% |

2.08% |

2.59% |

3.67% |

6.03% |

Bloomberg US Aggregate Bond Index |

2.78% |

2.78% |

4.88% |

0.52% |

-0.40% |

1.46% |

5.54% |

Past performance does not guarantee future results. Strategy Inception: 01/01/1986 Returns of less than one year are not annualized. |

|||||||

| The Bloomberg US Aggregate Bond Index is comprised of U.S. dollar-denominated investment grade fixed income securities with maturities of at least one year. The index includes corporate, government, and mortgage-backed securities. One cannot invest directly in an index. Sources: Bloomberg and BBH & Co. | |||||||

Highlights

|

Market Environment

First quarter 2025 may have been the calm before the storm. Treasury rates declined across the yield curve as concerns about muted growth prospects emerged due to indications the U.S. government planned to introduce protectionist trade policies. These concerns impacted investor predictions for forward-looking Fed interest rate decisions, indicating one additional Fed rate cut was expected and bringing the tally of expectations to four cuts by year end. The next Fed decision is scheduled for May 7th, and investors predict no change to the federal funds rate at that meeting.

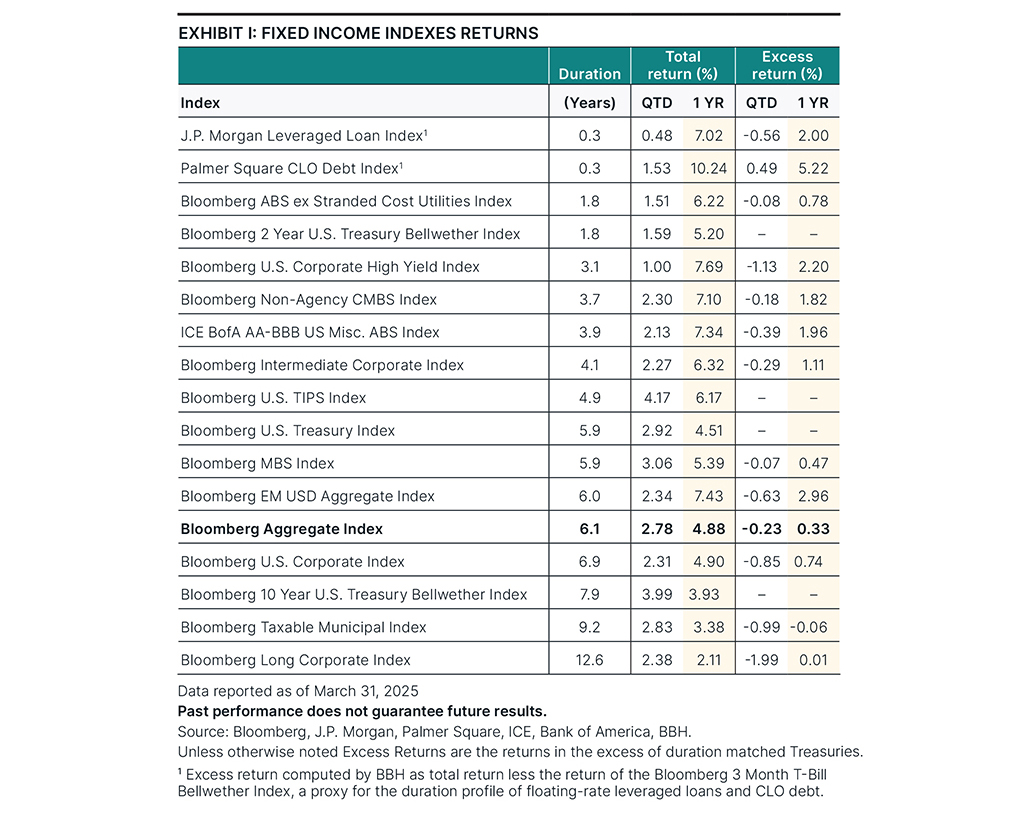

The Bloomberg U.S. Aggregate Index returned 2.8% during the first quarter as interest rates declined and credit spreads widened modestly from a low base. Riskier market segments underperformed high-quality bonds. The Bloomberg U.S. Corporate High Yield Index returned 1.0%, and the S&P 500 Index returned -4.3%. All major credit segments of the Bloomberg U.S. Aggregate Index had negative excess returns during the quarter.

Credit issuance remained robust during the quarter, with issuers refinancing short maturities amid low credit spreads, muted volatility, and strong demand. High-grade corporate bond issuance increased 19% while high yield issuance (bonds plus loans) was flat year over year. Asset-backed securities (ABS) issuance was flat, but nontraditional ABS volumes increased 10% from 2024’s pace. Commercial mortgage-backed securities (CMBS) volumes jumped 139% off a lower base year over year. Net issuance was modest but positive in all credit sectors.

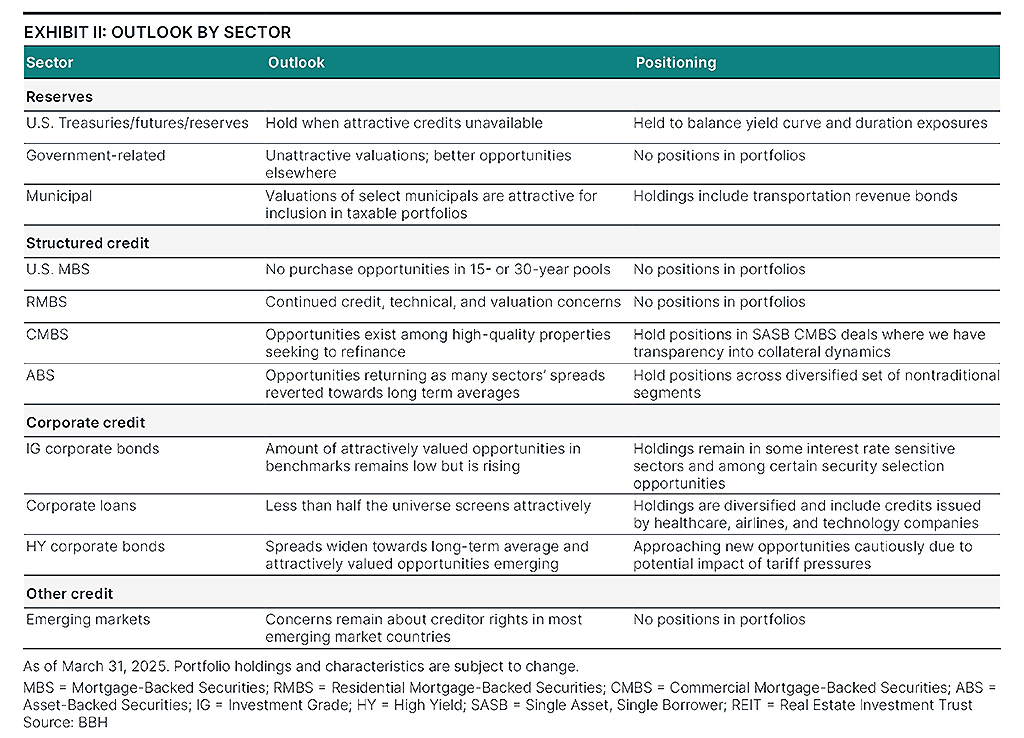

With spreads wider and positive net issuance, opportunities are emerging in pockets of the market. The percentage of credits that screened as a “buy” increased to 11% from 4% for investment-grade corporate bonds and to 38% from 16% for high yield corporate bonds. The percentage of loans screening as a “buy” decreased though to 45% from 58%. Within the investment-grade corporate credit market, interest rate sensitive sectors like life insurance, finance companies, and banks continue to screen attractively, while opportunities are also emerging in consumer cyclical companies. Tariff pressures should have a greater effect on more leveraged businesses in the high yield market, which drove credit spreads toward more appropriate ranges.

Away from credits in mainstream indexes, spreads in some ABS subsectors increased toward their long-term averages. Most nontraditional ABS continue to screen attractively in our valuation framework and offer appealing yield prospects. Data center ABS spreads widened from very low levels as concerns over long-term data center demand arose from artificial intelligence (AI) efficiency improvements and potential tariffs. CMBS spreads in select opportunities remain disconnected from their credit profiles, as property-level dynamics remain imperative for performance.

Exhibit I: Fixed income index returns for various indexes as of December 31, 2024, displaying duration, total return, and excess return.

Valuations

Valuations are not yet broadly attractive, and caution is still warranted in several areas of the market. Agency mortgage-backed securities (MBS) valuations remain broadly unattractive as spreads compressed further, with no cohort of the 15- or 30-year MBS market screening as a “buy” candidate. Negative excess returns remain possible for most of the investment-grade corporate bond universe. Less than half of the high yield corporate bond and loan markets screen attractively, highlighting the importance of a selective approach. Spreads on collateralized loan obligation (CLO) debt widened from very narrow levels to below-average levels. Emerging market credits remain unappealing due to concerns over creditor rights in most countries and its impact on their durability, compounded with the uncertainties that tariffs may impose on supply chains. We believe nonagency residential mortgage-backed securities (RMBS) remain plagued by poor issuance trends, unattractive valuations, and weak fundamentals.

Valuations reflect a growing belief that the U.S. economy is slowing. GDP estimates declined and suggested a recession is possible. Changing global tariff policies have weighed on business and consumer sentiment while also driving concerns about inflation.

Credit performance of business loans have been strong, although recent tariff policies may challenge future credit performance. Defaults trended lower, while recoveries improved. U.S. business bankruptcies remain low, and business loans held at banks are performing well. There has been an increase in pay-in-kind (PIK) interest for loans held in some private credit structures. We are monitoring the increase in PIK loans closely to distinguish between unique borrower business models vs. inabilities to service debt.

Performance

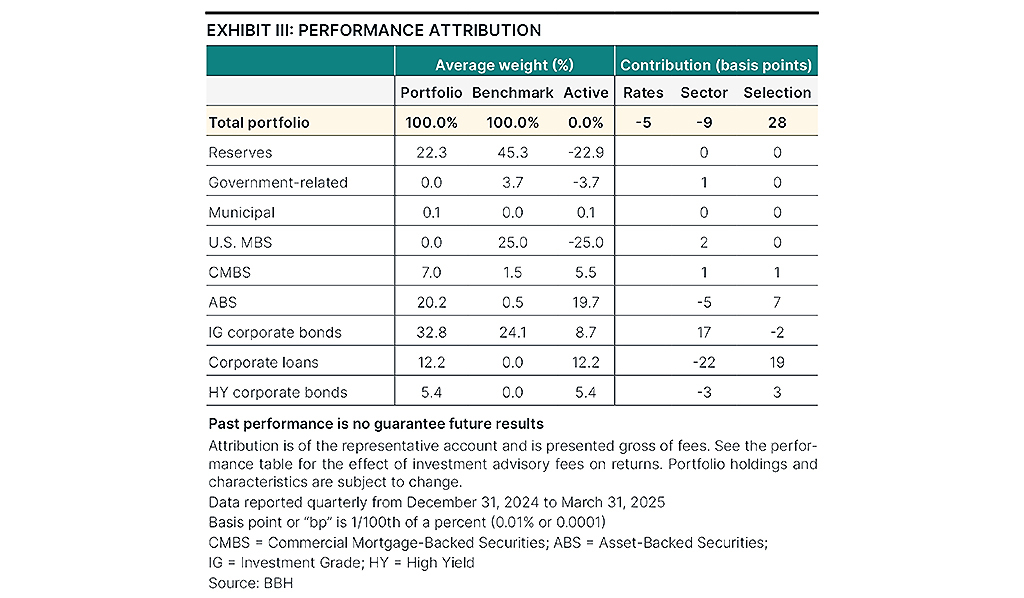

- The portfolio outperformed its benchmark during the quarter with selection effects driving overall positive contribution.

- Interest rates and sector effects had a small but negative impact on relative performance. Favorable selection in corporate loans and ABS impacted performance positively.

- Positions in high yield corporate bonds and corporate loans to technology companies and electric utilities were additive, as were holdings of CLOs.

- Sector exposures hindered results, with overweight positions to corporate loans, ABS, and high yield corporate bonds detracting from performance.

- The portfolio enjoyed a contribution from its sector and rating positioning in investment-grade corporate bonds.

- No subsector had a meaningful negative impact on selection results during the quarter.

Exhibit III: Attribution as of March 31, 2025, showing average portfolio weight and gross contribution displayed in basis points.

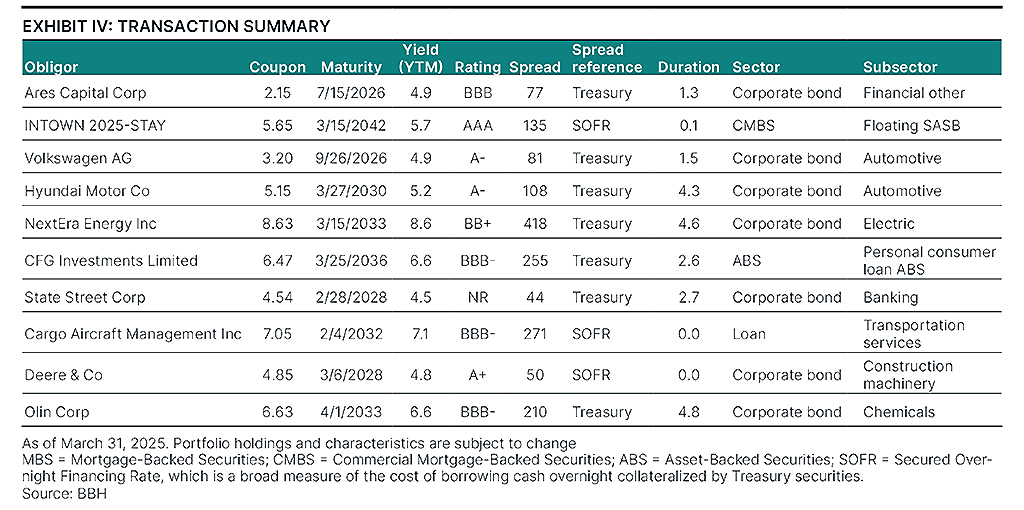

Transaction Summary

We continued to find durable credits offering attractive value even as valuations reflect a growing belief that the U.S. economy is slowing. The table below summarizes a few notable portfolio additions.

Characteristics

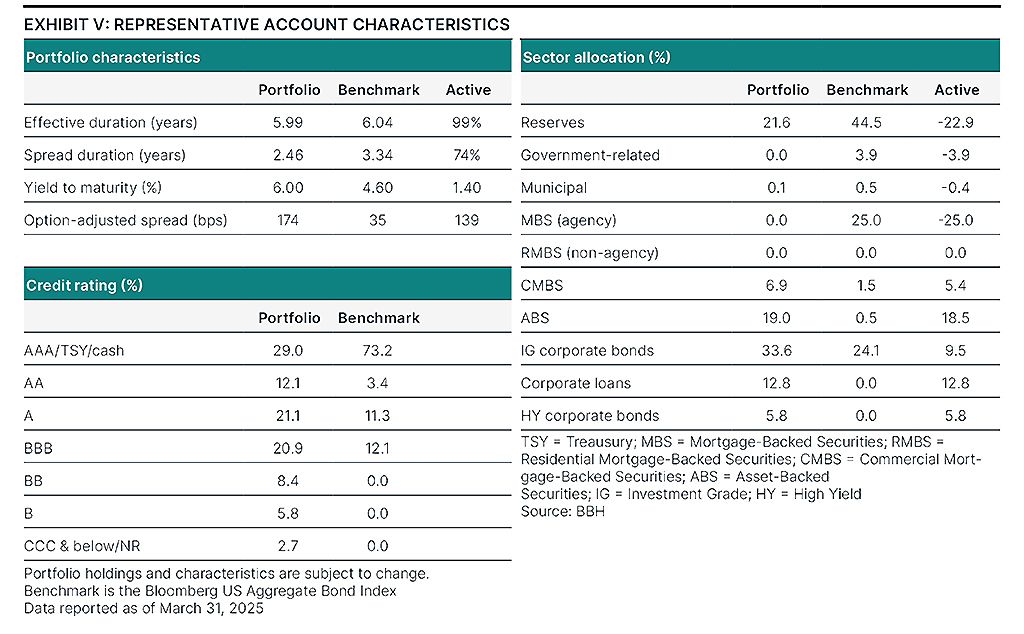

- The portfolio had a lower spread duration than the benchmark, reflecting less sensitivity to changes in credit spreads.

- Over the quarter, holdings of reserves increased while holdings of ABS and investment-grade corporate bonds decreased.

- The portfolio held 17% in high yield and nonrated credit instruments, similar to last quarter’s level.

- The portfolio held no exposure to agency MBS due to valuation concerns.

Exhibit V: Characteristics as of March 31, 2025, including credit rating and sector allocation.

Concluding Remarks

Uncertainty over tariffs is already having a recessionary impact on business activity and could pressure the performance of many industries and companies. We remain steadfast in our approach, focusing on identifying durable credits1 – those that can withstand the worst environments faced by their issuer’s industries – at attractive yields. We do this by evaluating individual opportunities bottom-up and not allowing top-down sentiments to alter the application of this approach. We believe this decision-making structure serves our clients well in all environments, whether markets are calm and complacent or volatile and uncertain.

1 Obligations such as bonds, notes, loans, leases, and other forms of indebtedness, except for cash and cash equivalents, issued by obligors other than the U.S. Government and its agencies, totaled at the level of the ultimate obligor or guarantor of the Obligation. Durable means the ability to withstand a wide variety of economic conditions

Totals may not sum due to rounding.

The securities do not represent all of the securities purchased, sold, or recommended for advisory clients and you should not assume that investments in the securities were or will be profitable.

Issuers with credit ratings of AA or better are considered to be of high credit quality, with little risk of issuer failure. Issuers with credit ratings of BBB or better are considered to be of good credit quality, with adequate capacity to meet financial commitments. Issuers with credit ratings below BBB are considered speculative in nature and are vulnerable to the possibility of issuer failure or business interruption.

Purchase and sale information provided should not be considered as a recommendation to purchase or sell a particular security and that there is no assurance, as of the date of publication, that the securities purchased remain in a portfolio or that securities sold have not been repurchased.

Opinions, forecasts, and discussions about investment strategies are as of the date of this commentary and are subject to change without notice. References to specific securities, asset classes, and financial markets are not intended to be and should not be interpreted as recommendations.

Definitions

Bloomberg US Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs, and total return performance of fixed-rate, publicly placed, dollar denominated, and non-convertible investment grade debt issues with at least $300 million paramount outstanding and with at least one year to final maturity The index is not available for direct investment.

Duration is a measure of the portfolio’s return sensitivity to changes in interest rates.

An index is not available for direct investment

“Bloomberg®” and the Bloomberg indexes are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the indexes (collectively, “Bloomberg”) and have been licensed for use for certain purposes by Brown Brothers Harriman & Co (BBH). Bloomberg is not affiliated with BBH, and Bloomberg does not approve, endorse, review, or recommend the Strategy. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to the Strategy.

Risks

Investors should be able to withstand short-term fluctuations in fixed income markets in return for potentially higher returns over the long term. The value of portfolios changes every day and can be affected by changes in interest rates, general market conditions, and other political, social, and economic developments.

Asset-Backed Securities (“ABS”) are subject to risks due to defaults by the borrowers; failure of the issuer or servicer to perform; the variability in cash flows due to amortization or acceleration features; changes in interest rates which may influence the prepayments of the underlying securities; misrepresentation of asset quality, value or inadequate controls over disbursements and receipts; and the ABS being structured in ways that give certain investors less credit risk protection than others. Below investment grade bonds, commonly known as junk bonds, are subject to a high level of credit and market risks.

SASB lacks the diversification of a transaction backed by multiple loans since performance is concentrated in one commercial property. SASBs may be less liquid in the secondary market than loans backed by multiple commercial properties.

The Strategy invests in derivative instruments, investments whose values depend on the performance of the underlying security, assets, interest rate, index or currency and entail potentially higher volatility and risk of loss compared to traditional bond investments.

Foreign investing involves special risks including currency risk, increased volatility, political risks, and differences in auditing and other financial standards. Prices of emerging market securities can be significantly more volatile than the prices of securities in developed countries, and currency risk and political risks are accentuated in emerging markets.

The Strategy may engage in certain investment activities that involve the use of leverage, which may magnify losses.

A significant investment of assets in one or more sectors, industries, securities and/or durations may increase its vulnerability to any single economic, political, or regulatory developments, which will have a greater impact on returns. Illiquid investments subject the investor to the risk that she may not be able to sell the investments when desired or at favorable prices.

Portfolio Characteristics are of the Representative Account. The Representative Account is managed with the same investment objectives and employs substantially the same investment philosophy and processes as the Strategy.

One basis point or bp is 1/100th of a percent (0.01% or 0.0001).

Brown Brothers Harriman Investment Management (“IM”), a division of Brown Brothers Harriman & Co (“BBH”), claims compliance with the Global Investment Per¬formance Standards (GIPS®). GIPS® is a registered trademark of CFA Institute. CFA Institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

To receive additional information regarding IM, including a GIPS Composite Report for the strategy, contact John W. Ackler at 212 493-8247 or via email at john.ackler@bbh.com.

Gross of fee performance results for this composite do not reflect the deduction of investment advisory fees. Actual returns will be reduced by such fees. Net of fees performance results reflects the deduction of the maximum investment advisory fees. Returns include all dividends and interest, other income, realized and unrealized gain, are net of all brokerage commissions, execution costs, and without provision for federal or state income taxes. Results will vary among client accounts. Perfor¬mance calculated in U.S. dollars.

The objective of our Core Plus Fixed Income Strategy is to deliver excellent after-tax returns in excess of industry benchmarks through market cycles. The Representative Account is managed with the same investment objectives and employs substantially the same investment philosophy and processes as the strategy. The Composite included all fully discretionary, fee-paying core fixed income accounts over $10 million that are managed to a duration of approximately 4.5 years and are invested in a broad range of taxable bonds. Accounts that subsequently fall below $9.25 million are excluded from the Composite.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved.

Not FDIC Insured No Bank Guarantee May Lose Money

IM-16561-2025-05-06 Exp. Date 07/31/2025