Clients often come to us when they are considering how best to address the pressing needs in their communities. Many use private foundations or donor-advised funds (DAFs) to make grants to organizations that are addressing the issues they are concerned about. Others may volunteer their services or expertise for the betterment of an organization.

Still others, recognizing that a need is not being met by an existing organization, may wish to start a charity with a mission that serves their goal. If you are considering this option, you should be aware of the steps involved in establishing a new charitable organization. Here, we summarize them in five points to help clients who have identified the type of charity they would like to establish and are on the path to doing so.

Organize Under State Law

State law governs nonprofit status. Most states permit nonprofit organizations to organize as a corporation, trust, or unincorporated association. For most public charities, a corporation is the preferred form. Most states have a statute governing nonprofit corporations; as a result, organizations structured as corporations have the benefit of clear guiding law.

Corporations are also flexible. If administrative changes need to be made – such as a change in the number of prescribed board members – they can be made by majority vote of the board of directors. Organizing as a corporation requires filing with the secretary of state. Required filings generally are simple and clear. You will also need to file the articles of incorporation with your secretary of state, which includes the name of the nonprofit, its board of directors, the office address, and its purpose.

Public charities may also be structured as a trust. That structure is not uncommon for private foundations but is less common for public charities. If structured as a trust, the trust must be irrevocable so the grantor cannot take back the assets. The trust structure leaves more control in the hands of its founders. Proponents of this structure might tout this as a benefit, while critics might argue it is inflexible.

Seek IRS Recognition

There are many benefits to being recognized by the IRS as a charity. One significant benefit is that charities generally are not subject to federal income tax. Another is that contributions to charitable organizations may be deductible by the donor. The ability for donors to receive a tax deduction enhances the charity’s ability to fundraise. Other benefits include the possibility of reduced postage rates, tax-exempt financing, and special pension plans.

In order to be recognized by the IRS as a charity, an organization must file a Form 1023, Application for Recognition of Exemption under section 501(c)(3). Form 1023 requires detailed, precise information regarding the organization’s purpose, financial data, and governance, and the organization must also apply for an Employer Identification Number (EIN). Finally, in order to qualify as a public charity (instead of a private foundation), the organization must demonstrate sufficient support by the general public. More information about filing for tax-exempt status with the IRS, along with frequently asked questions, can be found on the IRS website.

Once the Form 1023 is filed, the IRS indicates its recognition of the organization’s charitable status by issuing a letter, known as a determination letter. It can take up to six months to receive a response from the IRS, which is unsurprising given the volume of Form 1023 applications it receives each year – over 95,000, according to the agency.

Prepare to Raise Money

As noted, one of the benefits of being recognized as a charity is the tax deduction your donors may receive. There are a number of fundraising considerations, including solicitation, substantiation, and restriction on fundraising strategies.

Regarding solicitation, most states require you to file for a solicitation license. A license generally is required in any state where funds are solicited. This requirement can be tricky when you consider the prevalence of online giving.

Consider, for example, a charity located in Tennessee that provides services to Tennessee residents. If a donor from Oregon sees its website and makes an online contribution, will the organization be deemed to be soliciting in Oregon? There are different rules for each state, and many states have a de minimis exception. Often, sophisticated organizations use third-party vendors to manage solicitation licensure requirements.

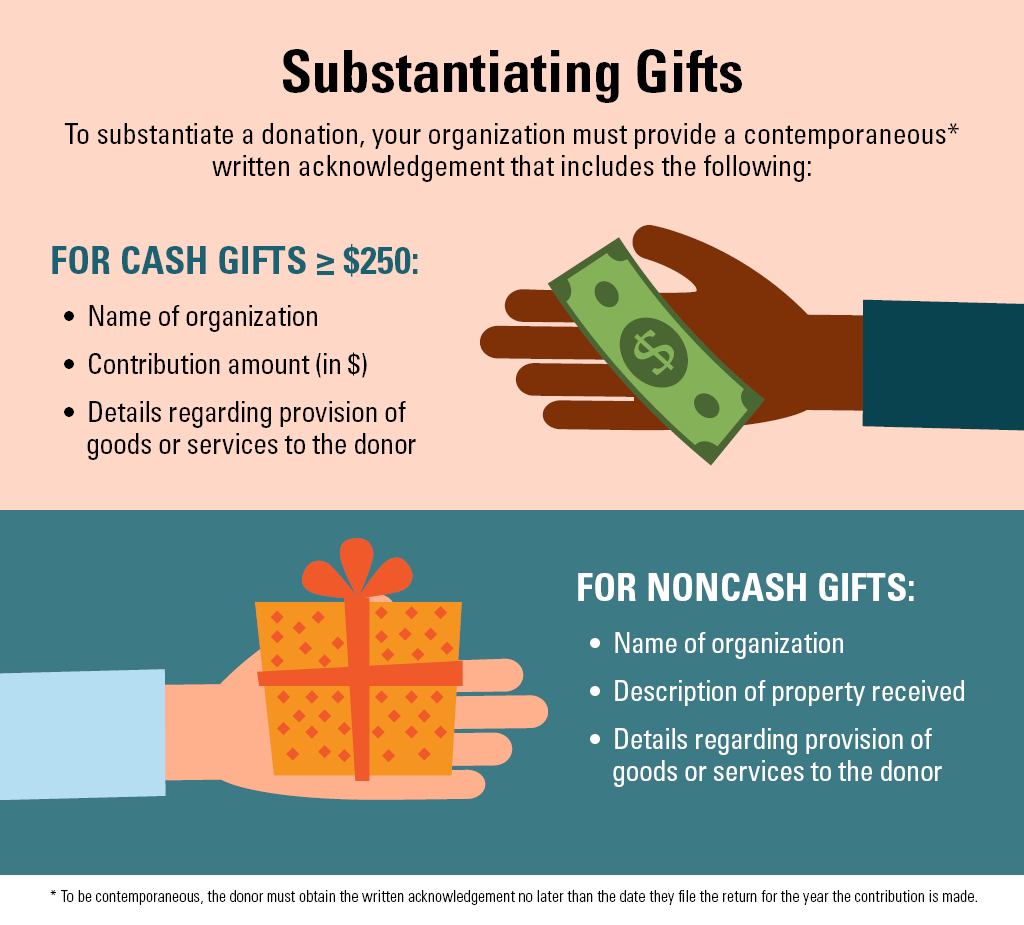

Regarding substantiation, when a donor makes a gift to a charity. the charity must substantiate that gift by providing specific documentation to the donor. The rules are specific, and failure to follow them results in negative tax implications for the donor (and a decreased likelihood she will make another gift).

For cash gifts of $250 or more, the charity must provide a written acknowledgement that must be contemporaneous with the gift. The acknowledgement must include the name of the organization, the amount of the contribution, and details regarding whether any goods or services were provided to the donor. For noncash gifts, the acknowledgement must include all of the above information, except a description of the property received (for example, 100 shares of Apple stock) instead of the dollar amount of the contribution.

Certain fundraising strategies, such as raffles or bingo, may be subject to restrictions at the state level. For example, a charity may be permitted to hold raffles, provided it does so no more than twice a year. Other fundraising strategies, such as the sale of items unrelated to the charity’s mission, might generate income that is subject to a tax known as unrelated business income tax (UBIT).

Consider, for example, a science museum with a mission to promote science and STEM education. If the gift store sells model dinosaur kits, those kits likely are aligned with the charity’s mission and not subject to UBIT. If the gift store sells silver-plated picture frames, plaid scarves, or crystal wine glasses, those items may not be aligned with the charity’s mission and may be subject to UBIT.

Establish Governance Provisions

Like any organization, a charity needs to establish effective governance practices, including board structure and development of policies and procedures. Developing an effective board is crucial to the success of the organization.

The role of the board is multifaceted. Board members must provide fiduciary oversight by overseeing the budget and audit, reviewing tax returns, and establishing effective risk management practices. In addition, board members have development responsibilities and must act as ambassadors for the organization. They may be expected to introduce people in their networks. Furthermore, board members have oversight of the executive director and will influence the organization’s vision and strategy for carrying out that vision. Charities should recruit board members who can fill these roles effectively.

The charity should also consider adopting policies that establish guidelines for operation and could reduce risk. It is important to have a policy in which board and staff members are asked to identify and disclose any potential conflicts of interest. Many charities have a gift acceptance policy, which identifies the type of gifts the organization will receive and how these gifts will be used.

For example, if the charity receives a bequest, do those funds go into the endowment, or can they be used for general operating? If the charity receives stock, does it sell immediately or hold? Will the charity accept illiquid assets, such as automobiles or art? Many charities adopt employment policies, which cover sexual harassment, dating within the workplace, nepotism, and equal opportunity. Charities may have policies covering a range of other topics, such as document retention and social media.

Consider Alternatives

Because establishing a new public charity is not without meaningful administrative requirements, anyone considering it should also consider alternatives. There are several options:

- An existing local charity might be willing to undertake a new programmatic initiative to address an unmet need in the community.

- An existing charity in another community that has demonstrated its effectiveness at addressing an issue might be willing to expand its geographic reach.

- A person might consider using his or her existing private foundation or DAF to make a grant to fund a charitable purpose, even if the funding does not go through an existing public charity. The foundation or DAF would need to exercise expenditure responsibility, which is an enhanced level of due diligence, but may require less administrative oversight than creating a new charity.

How to Set Up a Charity

Creating a new charity is not difficult, but it does require thoughtful planning and execution. In our Philanthropic Advisory practice at Brown Brothers Harriman (BBH), we advise philanthropists, foundations, and endowments on effective strategies for meeting their goals.

We invite you to reach out to your BBH wealth planner if you would be interested in having a conversation regarding your goals.

Contact Us

Brown Brothers Harriman & Co. (“BBH”) may be used as a generic term to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2024. All rights reserved. PB-07447-2024-05-24