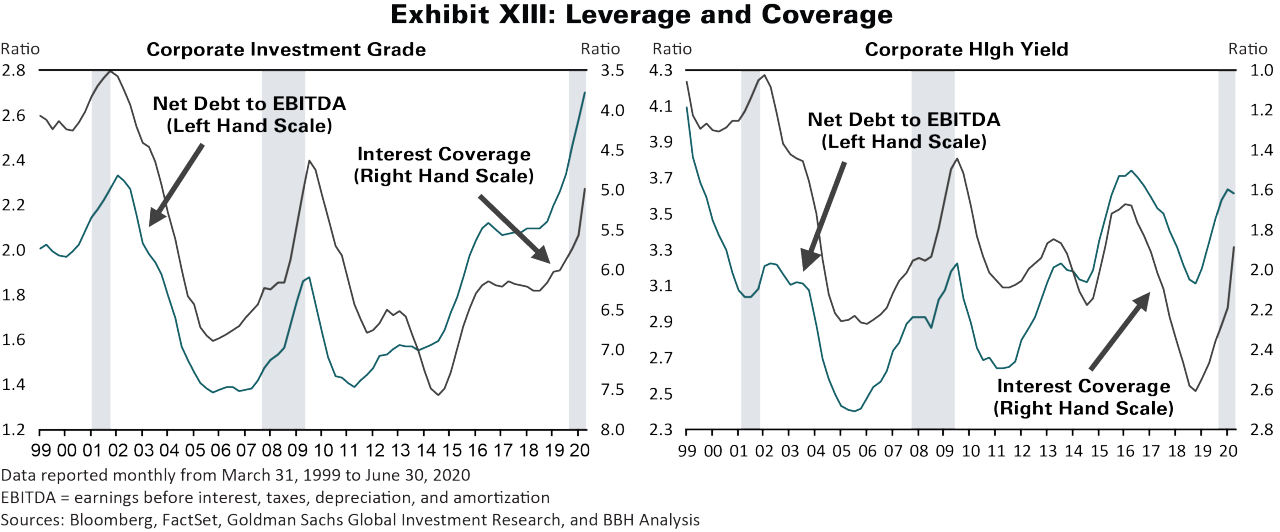

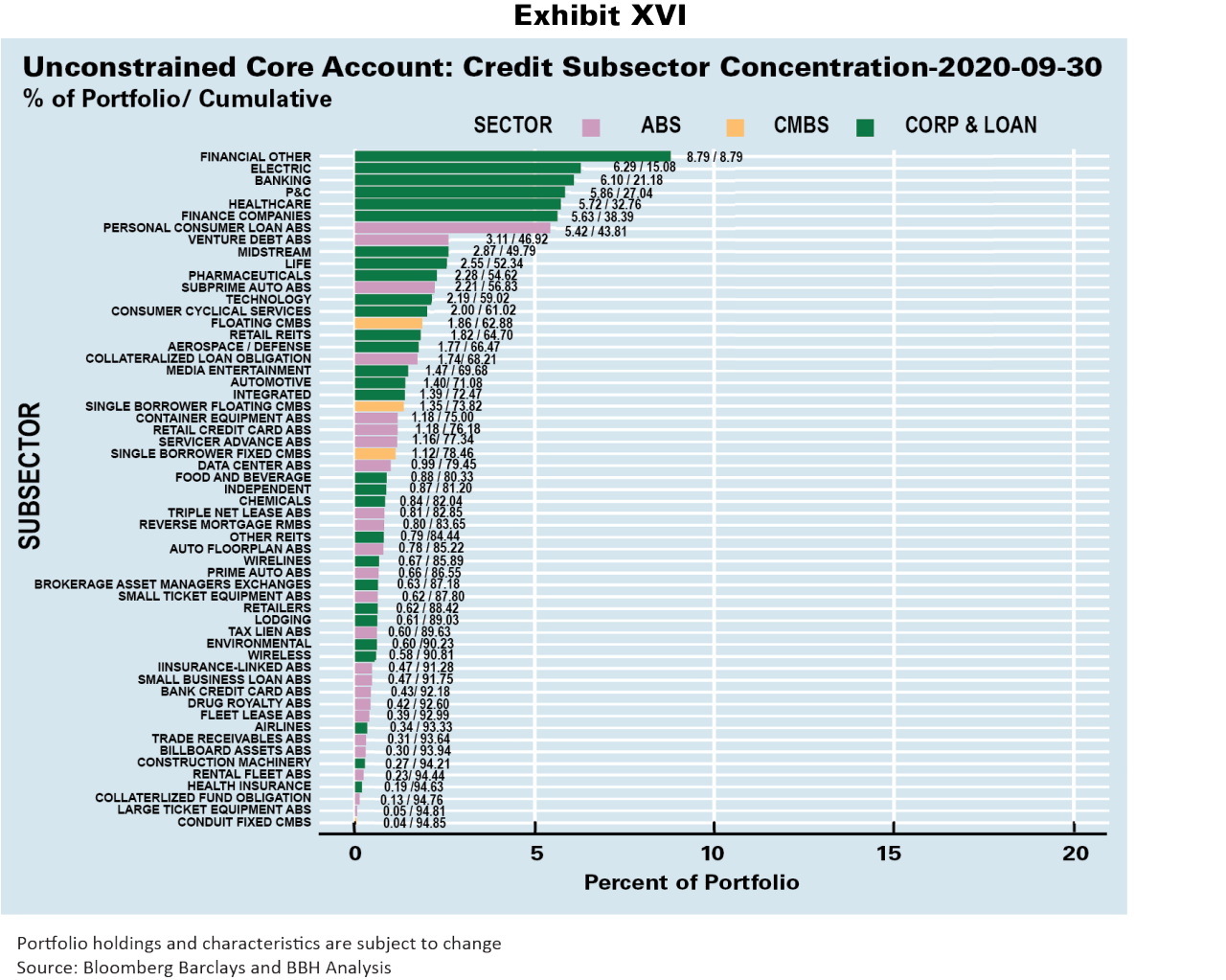

As our clients know, we don’t aspire to look like the index, and we would not have developed as strong a long-term track record if we did. As the opportunity set has narrowed and moved into a few corners of the credit market, we have developed some sizable concentrations in high-spread sectors with durable issuers. In the appendix which follows, we review seven subsectors, each of which make up more than 5% of the unconstrained Core portfolio, and together constitute nearly 44% of the portfolio.

In each case, there are certainly factors that are driving spreads wider, or holding them wide, some of them technical, some fundamental. But in each of these subsectors, we believe we have a strong grasp of the potential downside, and we are taking advantage of the sector weakness to invest in durable credits4 that we believe are likely to survive even a very difficult future scenario for the rest of this recession and the pandemic. It is our hope that this gives you a window into how our credit selection strategy has evolved in this stage of investors’ pandemic trauma.

Conclusion

We are still in the first half of the pandemic’s effect on the world economy. With another fiscal package highly uncertain, and prospects for continued hotspots or even a second wave, there will be more bad news on the business and consumer credit fronts. Nonetheless, the pandemic will ultimately end, and even without the Fed there is abundant capital to support the survivors of this recession, even in sectors like lodging and air travel. In this phase of the pandemic-driven credit cycle, while market-timing investors are still in the “bargaining” or “denial” phases of processing the pandemic, we are sorting out the long-term winners, many of which still offer compelling credit value. The ‘no-brainer’ values of April are gone, but we typically find this phase of a credit cycle the most interesting and energizing. We look forward to sharing it with you as we meet virtually over the coming months.

Andrew P. Hofer

Portfolio Co-Manager

Neil Hohmann, PhD

Portfolio Co-Manager

Paul Kunz PhD

Portfolio Co-Manager

Appendix – Description of Key Investment Concentrations

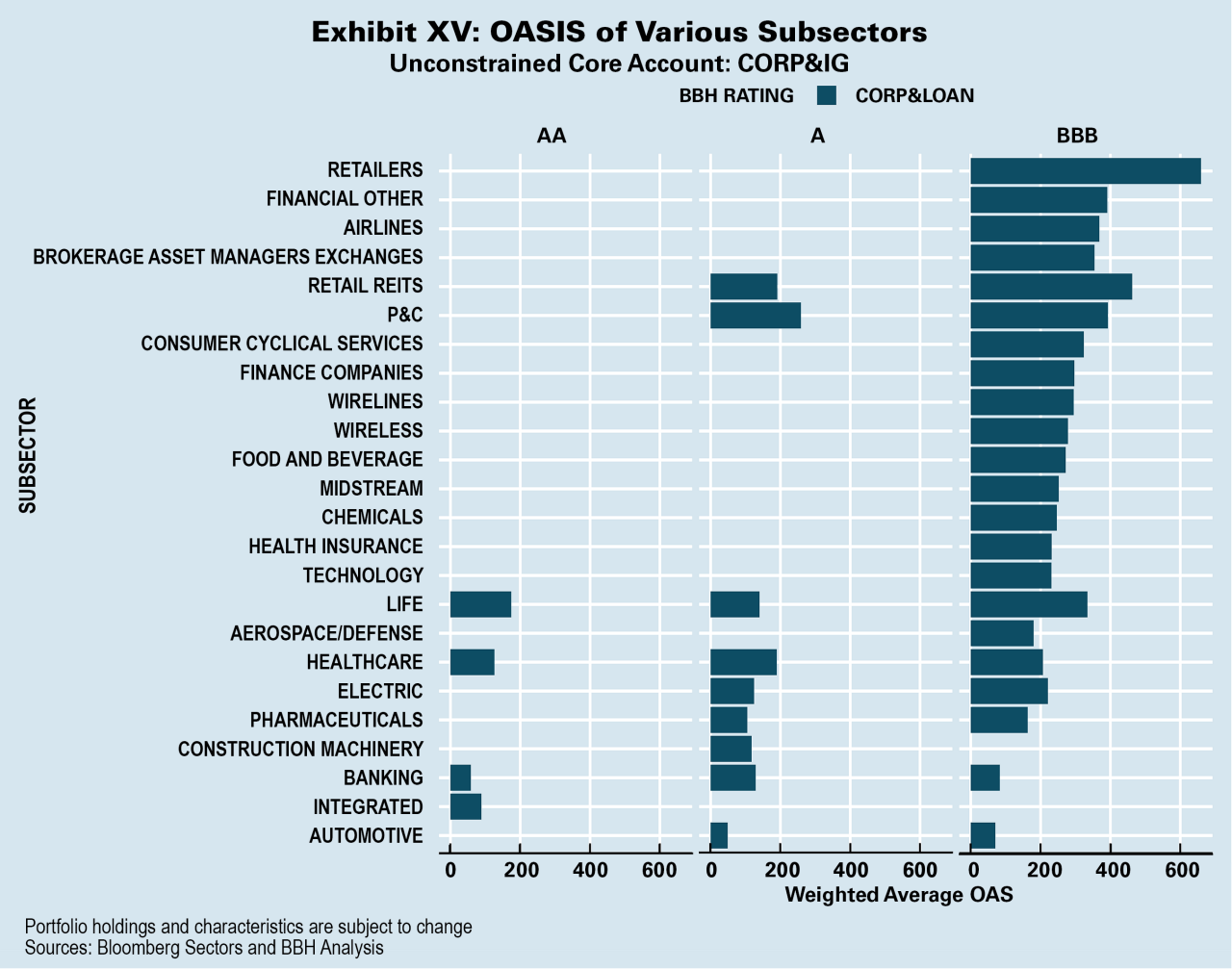

BDCs (“Financial Other”)

Business Development Companies (BDCs) are low leverage finance companies that originate direct loans to middle market companies across a diverse range of U.S. industries. BDCs, like real estate investment trusts (REITs), are SEC-regulated investment vehicles, and investors benefit from full transparency of holdings and operations, as well as a hard, statutory limit on financial leverage. The BDCs we invest in have large well-established credit platforms generally ranging from $5 billion to $40 billion in size with highly experienced direct lending teams. These include Blackstone, Blackrock, Ares, Golub, and Franklin Templeton

The unsecured debt of BDCs is at a very low leverage point for a financial company that has such stable asset performance. The debt-to-asset ratio for the BDCs in which we invest is generally near or below 50%; i.e. leverage is only 1x or less. As result, the resulting coverage of unsecured debt by unencumbered

assets of the BDC is high and can range from 2.5x-5x. Furthermore, the BDCs we invest in have substantial liquidity in cash and available credit lines, generally amounting to 10% to 20% of total assets.

Electric Generation

We focus on utilities that have strong regulatory relationships with a track record of good cost recovery either through real time riders or frequent rate filings. We also focus on utilities that have limited their non-rate regulated operations and have maintained healthy balance sheets. We focus on merchant generators that are critical pieces of infrastructure for their region with low starting leverage and stable cash flows. We tend to look for merchant generators that have some form of hedging, contracts, or other mechanism to maintain stable cash flows during weak commodity periods.

After initial spread widening in March and April, spreads for regulated electric utilities have steadily compressed. The compression has primarily been driven by strong existing balance sheets of most rate-regulated utilities as well as substantial liquidity. Operationally, electric utilities have benefited from being able to pass through COVID-related losses through multiple channels. They have either been allowed to directly pass on the costs associated with COVID through rate riders or they have been given permission by their regulators to place those costs into their regulated rate base and recover them in their next rate filing. Additionally, volumetric declines from commercial and industrial electric usage has been modestly offset by residential usage as many have switched to work-from-home arrangements.

Banking

We invest in banks with balance sheets that are strong enough to withstand severe economic downturns. These banks are well capitalized, have good asset quality with adequate reserves, solid liquidity, diverse sources of revenues, and well-respected management teams. The mid-March to early May widening in spreads allowed us to add bank bonds to our portfolios at very attractive spreads. Subsequently, they have tightened considerably.

The banks we invest in entered the coronavirus-induced economic downturn in a much better financial condition than they did during the GFC in 2008. Stress tests for large banks are routinely done to assess their ability to withstand severe economic downturns. Their regulatory capital ratios are generally between 2-3 times the levels at the end of the first quarter of 2009.

Asset quality has improved, with stronger underwriting standards, particularly for retail mortgages. The securities portfolios of the large banks have far less level 3 (marked-to-model) securities, and stronger risk controls. Loan losses were near multi-year lows prior to the pandemic, and the banks have markedly increased their loan loss reserves during the first half of 2020.

Property & Casualty (P&C) Insurance

We favor non-monoline businesses, management teams with a strong history of price-sensitivity in underwriting, prudent reserving practices, access to capital markets, and an investment approach consistent with the company’s underwriting posture. Our holdings include mostly large hybrid North American, Bermuda, and Swiss insurer/reinsurers, a title insurance company, a coastal property specialist. We have moved down in the capital structure in some of the large hybrid companies.

Investors have driven spreads wider due to large pandemic-related losses, increased storm and wildfire frequency and severity, and rising reinsurance costs. This is the second year of substantial price increases across most lines of business – companies describe this as the best “hard market” in the last 20 years, and these rising prices will be good for profitability. P&C companies are also accessing both the equity and debt markets easily, raising additional capital for the hard market. Finally, Covid losses are emerging as an earnings event, not a capital event.

Healthcare

While temporarily suspended non-essential services and increased expenses for COVID patient care drove industry margins down, government funding and service resumption have begun to stabilize profitability. Indeed, most of the service providers in our portfolios have already reached near pre-COVID patient volumes and net patient revenues. We believe that our strategy of focusing on market leaders provides protection against the leading credit concerns, such as the ongoing reimbursement pressures which may be exacerbated by political change.

Spreads on the taxable not-for-profit hospital systems, such as Bon Secours Mercy Health and Orlando Health, continue to be wider relative to their ratings, as these are taxable municipal bonds which, due to a smaller investor base, typically must offer higher yields. Also, some credits we hold continue to have excess spreads due to company-specific reasons. For example, InnovaCare, the leading health insurer in Puerto Rico with a growing business in Florida, still offers a Puerto Rico premium which, given that almost all its earnings before interest, taxes, depreciation, and amortization (EBITDA) comes from the federal government, we do not believe is appropriate. Likewise, spreads on Mednax and Tivity Health still reflect the significant corporate restructuring and management changes both companies have gone through; we believe that they are stronger credits at this time than these spreads may indicate. Finally, AdaptHealth was new in the bond market this summer and some of the initial issuer premium it had to offer lingers, even though the dollar price of the bond has risen by over 4% since issuance. All these illustrate our strategy of purchasing durable credits at attractive yields.

Aircraft Leasing (“Finance Companies”)

While spreads in the aircraft leasing sector were initially hit as hard as the airline sector, investors have begun to realize that the business models of these two sectors are very different. The key differences are that aircraft leasing companies have more flexible cost structures than airlines, and they also have bargaining power over suppliers and customers by virtue of their scale and customer diversity. These tenets of their business model have been severely tested since the beginning of 2020, and the largest industry lessors have responded well to the challenges.

Our investments in the sector have been focused on the largest lessors because they have the most financial flexibility. That flexibility derives from proactive efforts to lower leverage and to protect the balance sheet, combined with creating long liquidity runways. AerCap, Avolon, Air Lease, and ACG Capital are among the top-10 leasing companies globally and have deep relationships with original equipment manufacturers (OEMs), airlines, and capital providers. They were able to push their aircraft orders back, and in some instances cancel orders altogether in order to conserve cash. They drew down the entirety of their revolving credit lines and renegotiated their financing terms with banks to bolster cash availability. Finally, they have been renegotiating rent deferments and payment terms with airlines, which has led to some of the highest collection rates in the industry.

Our liquidity stress tests for these credits suggested that the above-mentioned lessors have adequate liquidity sources to address their full cash needs for the next two years. As a result, we became comfortable with short maturity lessor debt that was yielding around 8% for BBB- rated bonds with less than two years to maturity. We also stressed the collateral value that supported the secured term loans for some of those issuers and increased our exposure to existing loan positions. As more information became available from these lessors in the quarter, we learned that our initial stress scenarios were overly conservative, and that these issuers have even greater liquidity runways than estimated. In mid-summer, these issuers started to test the capital markets with new bond deals, and we participated in many primary deals with yields around 5.5% for 5-year tenors that trade today in the 4.5%-5.0% range.

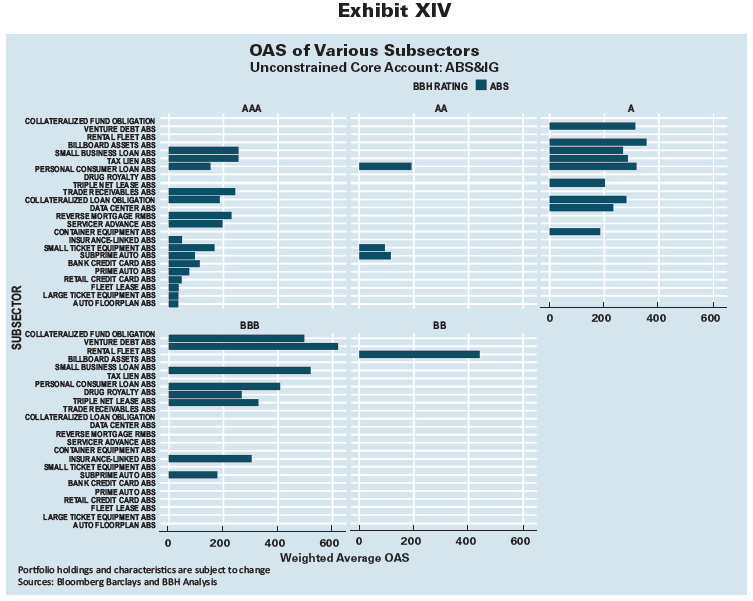

Personal Consumer Loan ABS

Our investments in personal consumer ABS issuers have been focused on brick and mortar (i.e. branch office) lenders with long operating histories, strong management and ownership and a focus on effective servicing delinquent borrowers. Our investments typically have credit enhancement of 30%-50%, sufficient to absorb even depression-level losses and still repay us. Historically, brick and mortar consumer lenders have been able to limit ultimate losses in downturns with successful servicing. Brick and mortar lenders’ net losses and delinquencies have tracked similarly to credit card trust performance, showing continued strong performance. Unsecured consumer loans typically realize low recoveries following defaults, so borrower engagement through servicing programs is essential to prevent losses.

The economic recovery since the peak of the pandemic shutdown has led payment rates on unsecured consumer loan ABS to improve significantly. Stimulus and enhanced unemployment benefits initially supported borrowers; however, lenders were quick to provide payment deferral and loan modification programs to impacted borrowers. The end of the Coronavirus Aid, Relief, and Economic Security (CARES) Act stimulus and uncertainty around further stimulus may create economic drag that causes unemployment to rise or more financial pain for borrowers, especially those that have already lost their jobs. However, any further pandemic effects on unemployment are likely incremental, and unemployment is the key driver of consumer loan performance.

Current low levels of delinquency and high levels of cured deferrals suggest that significant incremental delinquencies and losses due to the pandemic are unlikely. This creates a survivorship bias in the remaining loan pools, which is an important credit positive. For new originations, lenders have tightened underwriting standards, increased interest rates and tightened employment verification. Origination volume decreased significantly in Q2 but increased in Q3 as lenders are continuing to be more selective in extending credit. This should cause new originations to have stronger performance than recent vintages.