A Structured Credit Strategy offers yield and credit advantages that are difficult to find today within fixed income

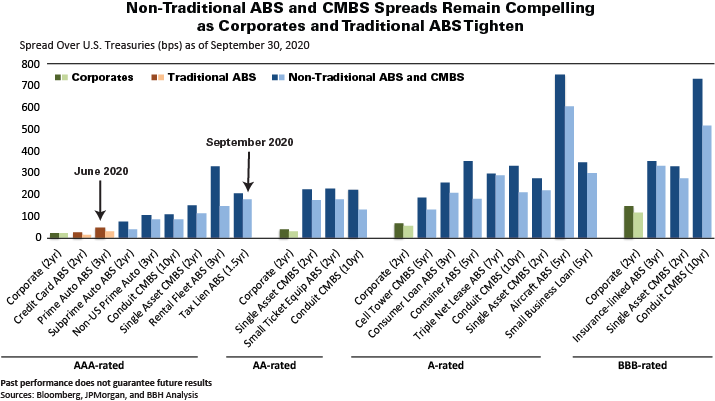

Back in late March, we drew confidence from our many direct conversations with the senior management teams of our issuers. It’s been gratifying to see our credit performance expectations confirmed in monthly remittance reports over the last six months. With the exception of aircraft ABS, we now see little scope for impairments or downgrades across the entire ABS market. We expect investment grade tranches of CMBS and CLOs to perform, with the possible exception of a handful of BBB-rated tranches with outsized COVID concentrations. Yet compensation available across structured credit remains compelling, both in absolute terms and against the norm of the last decade. As BBH’s Strategy exemplifies, a short duration portfolio of non-traditional ABS, diversified across 20 subsectors with an average A-rating, can provide today’s investors a yield over 4%.

We look forward to sharing more credit observations and purchase examples with our investors in the coming months.

Sincerely,

Portfolio Management Team

Neil Hohman, PhD

Head of Structured Products

Chris Ling

Structured Products Trading

Andrew P. Hofer

Head of Taxable Fixed Income

Definition

Bloomberg Barclays US Corporate Bond Index (BBG IG Corp) measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility and financial issuers

Bloomberg Barclays US Corporate High Yield Index (BBG HY Corp) is an unmanaged index that is comprised of issues that meet the following criteria: at least $150 million par value outstanding, maximum credit rating of Ba1 (including defaulted issues) and at least one year to maturity.

Bloomberg Barclays ABS Index (BBG ABS) is the ABS component of the Bloomberg Barclays US Aggregate Index. The ABS Index has three subsectors: credit and charge cards, autos and utility. The index includes pass-through, bullet, and controlled amortization structures. The ABS Index includes only the senior class of each ABS issue and the ERISA-eligible B and C tranche.

Bloomberg Barclays Non-AAA ABS Index (bbg Non-AAA ABS) is the non-AAA ABS component of the Bloomberg Barclays U.S. Aggregate Bond Index, a market value-weighted index that tracks the daily price, coupon, pay-downs, and total return performance of fixed-rate, publicly placed, dollar-denominated, and non-convertible investment grade debt issues with at least $300 million par amount outstanding and with at least one year to final maturity.

Bloomberg Barclays CMBS Index (BBG CMBS) is the CMBS component of the Bloomberg Barclays U.S. Aggregate Bond Index, a market value-weighted index that tracks the daily price, coupon, pay-downs, and total return performance of fixed-rate, publicly placed, dollar-denominated, and non-convertible investment grade debt issues with at least $300 million par amount outstanding and with at least one year to final maturity

JP Morgan Other ABS Index (JPM Other ABS) represents ABS backed by consumer loans, timeshare, containers, franchise, settlement, stranded assets, tax liens, insurance premium, railcar leases, servicing advances and miscellaneous esoteric assets (that also meet all the Index eligibility criteria) of the The JP Morgan ABS Index. The JP Morgan ABS Index is a benchmark that represents the market of US dollar denominated, tradable ABS instruments. The ABS Index contains 20 different sub-indices separated by industry sector and fixed and floating bond type. The aggregate index represents over 2000 instruments at a total market value close to $500 trillion dollars; an estimated 70% of the entire $680 billion outstanding in the US ABS market

JP Morgan CLO Index (JPM CLO) is a market value weighted benchmark tracking US dollar denominated broadly-syndicated, arbitrage CLOs. The index is comprised solely of cash, arbitrage CLOs backed by broadly syndicated leveraged loans. All CLOs included in the index must have a closing date that is on or after January 1, 2004. There are no weighted average life (WAL) limitations. There are no minimum tranche size restrictions and includes only tranches originally rated from AAA/Aaa through BB-/Ba3.

The securities discussed do not represent all of the securities purchased, sold or recommended for advisory clients and you should not assume that investments in the securities were or will be profitable. Quality ratings reflect the credit quality of the underlying issues in the fund portfolio and not of the fund itself. Issuers with credit ratings of AA or better are considered to be of high credit quality, with little risk of issuer failure. Issuers with credit ratings of BBB or better are considered to be of good credit quality, with adequate capacity to meet financial commitments. Issuers with credit ratings below BBB are considered to be of good credit quality, with adequate capacity to meet financial commitments. Issuers with credit ratings below BBB are considered speculative in nature and are vulnerable to the possibility of issuer failure or business interruption. The Not Rated category applies to Non-Government related securities that could be rated but have no rating from Standard and Poor’s or Moody’s. Not Rated securities may have ratings from other nationally recognized statistical recognized statistical rating organizations. For purpose of complying with the GIPS® standards, the firm is defined as Brown Brothers Harriman Investment Management ("IM"). IM is a division of Brown Brothers Harriman & Co. ("BBH"). IM claims compliance with the Global Investment Performance Standards (GIPS®). To receive a list of composite descriptions of IM and/or a presentation that complies with the GIPS standards, contact John W. Ackler at (212) 493-8247, or via email at john.ackler@bbh.com. Gross of fee performance results for this composite do not reflect the deduction of investment advisory fees. Actual returns will be reduced by such fees. "Net" of fees performance results reflect the deduction of the maximum investment advisory fees. Performance calculated in U.S. dollars. The Composite is comprised of fully discretionary, fee-paying structured products accounts over $10 million that are managed in the Structured Fixed Income strategy. The target duration may range from 1 to 4 years. Investments are focused on asset-backed and related structured fixed income securities. Holdings are primarily investment grade but non-investment grade securities may be held. Investments may include non-dollar fixed income. Accounts are benchmarked to the Barclays Capital Asset-Backed Index or equivalent. Standard deviation measures the historical volatility of a returns. The higher the standard deviation, the greater the volatility. The Sharpe ratio is the average return earned in excess of the risk-free rate.