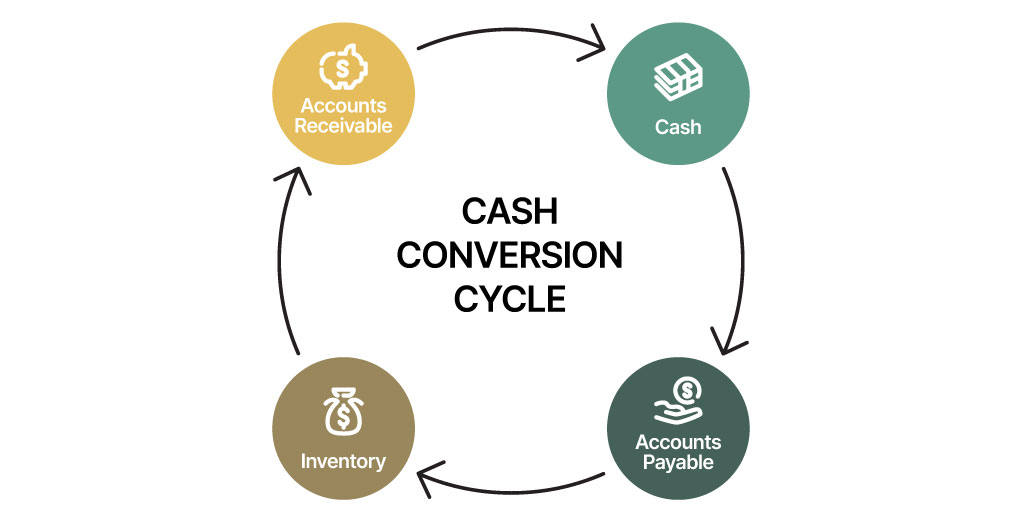

Graphic showing the flow of the cash conversion cycle (CCC) between cash, accounts payable, inventory, and accounts receivable.

For private businesses, maintaining sufficient liquidity is crucial for operations, growth, and navigating periods of uncertainty. While holding excess cash on the balance sheet can provide a comforting buffer, it can also be an inefficient use of excess capital. Business owners must judiciously manage this liquidity to balance security and strategic growth.

What Is Excess Liquidity?

Excess liquidity, or assets easily translated to cash, on a balance sheet is excess capital beyond the immediate, short-term operational needs of a business. Firms can engage in active liquidity management processes independent of the level of cash shown on their balance sheets.

Effective liquidity management can lead to lower financing costs, increased operational flexibility, and the ability to meet short-term obligations using assets that can be most readily converted into cash.

In this article, we lay out six critical considerations when effectively managing corporate liquidity.

A Historical Look During the credit market breakdown of 2008-09, firms’ inability to obtain external funding allowed researchers to look at corporate liquidity management at a time of acute liquidity scarcity. Prior to the financial crisis, bank regulation did not have explicit quantitative liquidity requirements on banks. During and immediately following the crisis period, banks began accumulating liquid assets. Following the crisis, in December 2010, Basel III introduced a requirement minimum liquidity coverage ratio (LCR) on the amount of unencumbered high-quality liquid assets (HQLA). The maintenance of large amounts of HQLA incurs an opportunity cost in the form of forgone income from higher-yielding and riskier investments such as term loans or non-HQLA securities. Following the introduction of the LCR requirement and other post-crisis regulations, the banking system has taken on a greater role as corporate liquidity provider through credit lines. Post-crisis regulations have increased resilience, as banks’ large liquidity positions ensure that drawdowns on credit lines are supported by higher liquidity levels. In addition, the Federal Reserve’s stress testing regime and the U.S. standardized regulation requires banks to account for undrawn credit lines in capital planning ways that were not done before the crisis. |

1. Cash Requirement Assessment

Active liquidity management first requires an understanding of a business’s cash requirements, from operational needs to emergency funds. A cash requirement assessment determines the next steps in liquidity management and can give insight into the business’s overall financial stability and outlook.

Operational Needs

It is crucial to evaluate a business’s working capital requirements, including inventory, receivables, and payables, to ensure that the cash obligations required to meet day-to-day operations are fully funded. Cash conversion cycles (CCC) are a helpful metric that can uncover inefficiencies and optimize cash flow.

Specifically, the CCC is segmented into three components:

- Days sales outstanding (DSO)

- Days inventory outstanding (DIO)

- Days payable outstanding (DPO)

Improvements in any of these areas can significantly enhance liquidity – and the lower the CCC, the better.

Emergency Funds

Maintaining a reserve to cover unexpected expenses or economic downturns is prudent. A common guideline is to hold cash reserves sufficient to cover three to six months of operating expenses. However, the actual reserve level should be tailored to the industry’s volatility, the company’s risk tolerance, and historical cash flow patterns. A Monte Carlo1 simulation can provide insights into the adequacy of the reserve by modeling various economic scenarios.

2. Business Reinvestment

Identifying opportunities for reinvestment can enhance a company’s long-term value.

Capital Expenditures

Investing in new technology, equipment, or facilities can enhance productivity and growth potential. A cost-benefit analysis, including net present value and internal rate of return metrics, should underpin these decisions. Sensitivity analysis can further refine these projections by evaluating the impact of key variables on project viability.

Research and Development (R&D)

Allocating funds to innovation can yield significant long-term benefits and keep the business competitive. Under the Inflation Reduction Act, eligible businesses can also earn R&D credits with qualifying activities. Evaluating the potential for intellectual property generation and market differentiation can further inform the scale and focus of R&D investments, while employing a real options analysis can value the flexibility and potential future benefits of R&D projects.

Acquisitions and Expansions

Strategic acquisitions or expanding into new markets can drive growth and diversify revenue streams. A comprehensive due diligence process, including financial, operational, and strategic fit assessments, is crucial for successful execution. Discounted cash flow analysis and comparables can provide robust valuation metrics to inform acquisition decisions.

4. Debt Management

Evaluating the cost of debt vs. the return on investments is essential to effective liquidity management.

Pay Down Debt

Paying down high-interest debt can be a prudent use of excess cash, reducing interest expenses and improving the balance sheet. Conducting a comparative analysis of the effective interest rates and projected returns on potential investments can guide optimal debt management strategies.

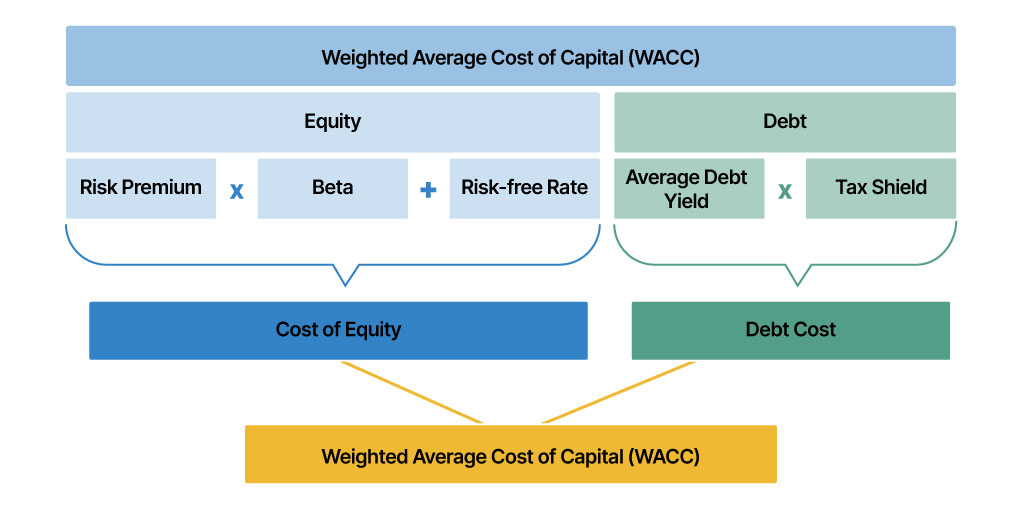

As shown in the nearby graphic, the weighted average cost of capital (WACC) can serve as a benchmark for these decisions.

Graphic breaking down the formula of the weighted average cost of capital (WACC).

WACC = Cost of Equity + Debt Cost, where:

- Equity = Risk Premium x Beta + Risk-Free Rate

- Debt = Average Debt Yield x Tax Shield

Leverage Opportunities

Conversely, in a low interest rate environment, retaining some debt while investing excess cash can amplify returns. Scenario analysis and stress testing can help determine the optimal debt-to-equity ratio under varying economic conditions. Additionally, leveraging financial ratios such as the debt-to-EBITDA ratio can provide insights into the firm’s leverage capacity without compromising financial stability.

5. Investment Opportunities

After assessing your business’s liquidity needs, reinvestment opportunities, and debt management, you might consider further investment opportunities. Excess cash can be strategically invested to generate returns in the short and/or long term.2

Short-Term Investments

Treasury bills, commercial paper, and money market funds offer liquidity and lower risk while providing modest returns. Analyzing the yield curves and market conditions will inform the optimal mix and duration of these instruments. For example, duration matching can align the maturity of investments with anticipated liquidity needs.

Long-Term Investments

For surplus cash that is not needed in the short term, longer-term investments such as bonds or structured notes can be considered. These can offer higher returns but come with increased risk.

A thorough risk-reward analysis considering metrics like the Sharpe ratio, Sortino ratio, and value at risk is essential for making informed decisions. Additionally, strategic asset allocation can be optimized using mean-variance analysis to balance the expected return and risk.

| Index | 0-3 Month Treasury Index | 3-6 Month Treasury Index | 6-9 Month Treasury Index | 9-12 Month Treasury Index | 1-3 Year Treasury Index | Municipal Bond Index | 3-5 Year Treasury Index | US IG Corporate Index | US High Yield Corporate Index |

| Yield to Maturity | 5.36% | 5.33% | 5.12% | 5.04% | 4.67% | 4.09% | 4.30% | 5.39% | 7.97% |

6. Risk Management

Throughout the liquidity management process, it is essential to remain aware of potential risks. Risk management strategies include the following:

Liquidity Buffers

While investing excess cash, it is crucial to maintain sufficient liquidity buffers to handle economic volatility without needing to liquidate investments at inopportune times. Contingency planning and liquidity stress tests can help define adequate buffer levels. The application of cash flow at risk can quantify potential liquidity shortfalls under adverse scenarios.

Diversification

As we have said in past commentaries on asset allocation, spreading investments across different asset classes and geographies can mitigate risk and protect the company’s financial health.

Conclusion

Effective corporate liquidity management is about striking a balance between security and growth. By assessing cash requirements, exploring investment opportunities, managing debt judiciously, reinvesting in the business, providing shareholder returns, and mitigating risks, private businesses can optimize their excess cash. This not only strengthens financial stability, but also positions the company for sustained growth and success in a competitive marketplace.

At Brown Brothers Harriman, we understand the complexities of liquidity management and are here to guide you in making informed, strategic decisions that align with your business objectives. Our tailored solutions are designed to maximize the efficiency and profitability of your excess cash while ensuring robust risk management. To learn more about strategies for liquidity management, please reach out to the Corporate Advisory & Banking team.

Contact Us

1 A Monte Carlo analysis runs multiple simulations of a financial plan against future market conditions. The trial runs produce a range of potential results and are one way of illustrating and evaluating the statistical probability of your planning strategies.

2 Yield to maturity is the total rate of return earned when a bond makes all interest payments and repays the original principal.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2024. All rights reserved. PB-07482-2024-06-10