Investing is a broad and sometimes overwhelming topic that can take many years to understand, so it is important to broach the topic with your children early. But where do you start when it comes to teaching your child about investing?

We outline some basic key points that parents can share with their children to help navigate that first discussion about investing, answer their initial questions, and improve financial literacy. This is meant to touch the surface, as we hope conversations continue throughout their early years and into adulthood.

What is investing?

Investing means using your money to buy something in hopes that it will grow in value, or appreciate, over time. Instead of spending your money right away, you put it into things like a business or property so it can earn more money in the future.

What can you invest in?

You can invest in many things: cars, art, real estate, sports memorabilia, and more. For this guide, we will explore the basics of the most common asset classes: stocks and bonds.

Why do people invest?

People invest with the hope that their assets will grow in value over time. For example, you might buy a pack of baseball cards with an up-and-coming player inside. You can choose to either sell the card to your friend right away or hold on to it. If next season, the player is named MVP or wins the World Series, the card’s value will rise. As a result, it can be sold for a higher price, allowing you to profit.

Stocks

What are they?

Stocks represent ownership in a company and can be bought and sold on stock exchanges. Stock exchanges are essentially a marketplace for individuals and institutions to sell and buy public stocks from one another.

Each share of stock signifies partial ownership of a corporation, representing a claim to part of the corporation’s assets and earnings. Think about what you use frequently. For example, the toothpaste you use every day might be a product of Colgate-Palmolive, a publicly traded company that you can purchase shares of.

How do they work?

Companies will issue, or sell, stock to the public in order to raise cash to fund projects and allow the company to grow. Your shares can appreciate or depreciate in value based on the company’s performance. For example, if “Frozen 3” is a box office hit, the Disney stock price may increase.

Why invest in stocks?

Historically, stocks have had higher long-term returns than other asset classes. Stocks have the ability to continuously rise in price if demand remains strong, which creates the opportunity for high returns.

However, this does not mean that all stocks are created equal – not all stocks will deliver high returns! A company may go out of business or underperform, and you can lose money on your investment. Returning to the previous example, this would be the equivalent of the baseball player becoming seriously injured, lowering the card’s value. Investing in the stock market involves an inherent amount of risk and volatility (fluctuations in the price of your stock).

Bonds

What are they?

A bond is like an IOU. When a company, government, or municipality needs money, they borrow it from people by selling bonds. The organizations that lend the money are known as issuers. For the purposes of this example, we will focus on bonds issued by companies, otherwise known as corporate bonds.

How do they work?

Bonds, like stocks, are issued to the public as a way for the company to generate capital. Continuing with a previous example, Colgate-Palmolive could be an issuer of bonds. If you, the lender, purchase those bonds, you are lending Colgate-Palmolive money, with the promise of repayment at a predetermined time in the future, along with interest payments, called coupons, each year. The predictable stream of income received is why bonds are known as fixed income.

Why invest in bonds?

Depending on the issuer, bonds can be lower risk investments that can offer steady investment income. Like stocks, however, some bonds can be riskier than others. Some companies are less stable as others, and it is possible that a company could go bankrupt and you would not be repaid.

How can I start investing?

There are three potential methods for beginning to invest: buying an individual stock or bond, a mutual fund, or exchange-traded funds (ETFs).

- Individual stocks or bonds: If you buy stocks or bonds, you are making a direct investment in a public company or organization. There may be a small brokerage fee to execute the trade to purchase it, but the investment can be any size, depending on the price of the stock or bond.

- Mutual funds: These pool money from investors to invest in a basket of equities and/or fixed income. These funds typically are actively managed, require a minimum investment, have a management fee, and are priced only once daily.

The benefit of a mutual fund is that you will have access to many securities instead of having to buy each one individually. For example, as of August 15, 2025, Amazon cost $231 a share . Instead of spending $213 to purchase one share of Amazon, you could buy $231 worth of a mutual fund that owns Amazon but also has other stocks in its portfolio. - ETF: This is a marketable security that tracks an index. For example, if you purchased an S&P 500 ETF, these ETF shares would track all the companies listed in the S&P 500 stock market index. ETFs are passively managed, are priced constantly throughout the day, and have high daily liquidity and generally lower fees than mutual funds.

Why should I start investing early?

Investing earlier in life allows you the opportunity to benefit from the power of compound interest. Compounding occurs when positive returns build on each other over time to create even greater returns.

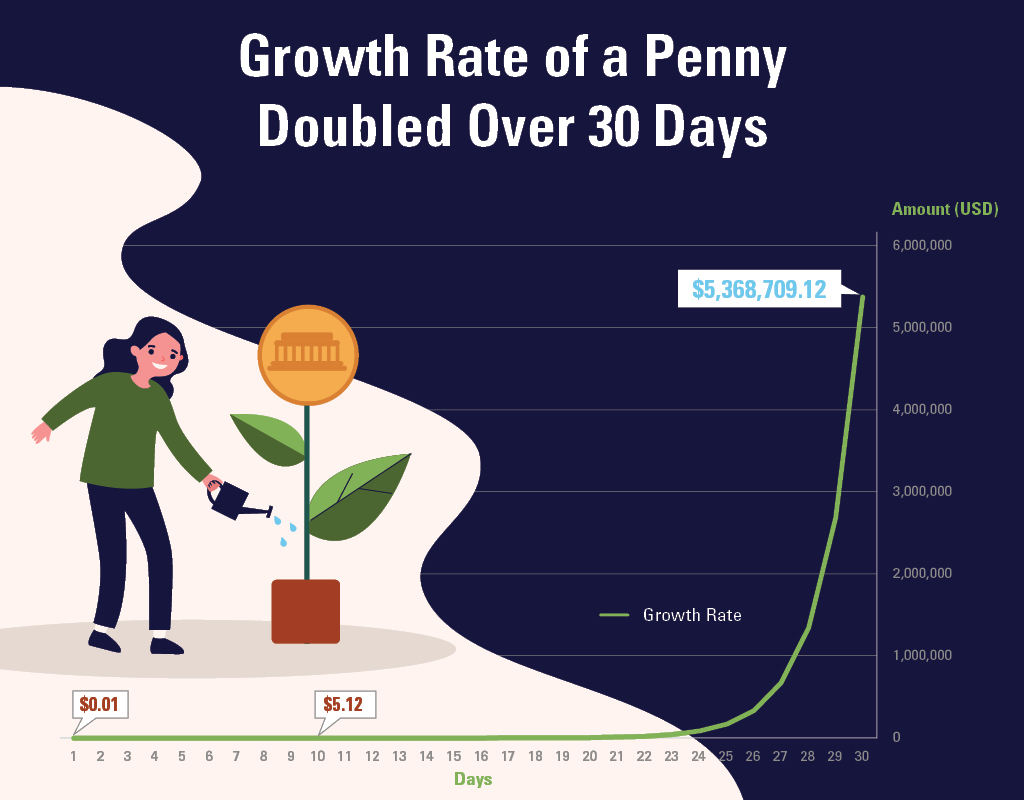

One way to visualize this is to map out a penny doubled for a month. After 10 days, the value is only $5.12, but by day 30, its value reaches $5,368,709.12. Therefore, if you invest earlier in life, you allow ample time to grow your wealth over the long term. This key concept is critical when thinking about savings. Starting to invest in your 20s – even with small monthly contributions – can grow your money significantly more than if you wait until your 30s or 40s, thanks to the power of compounding.