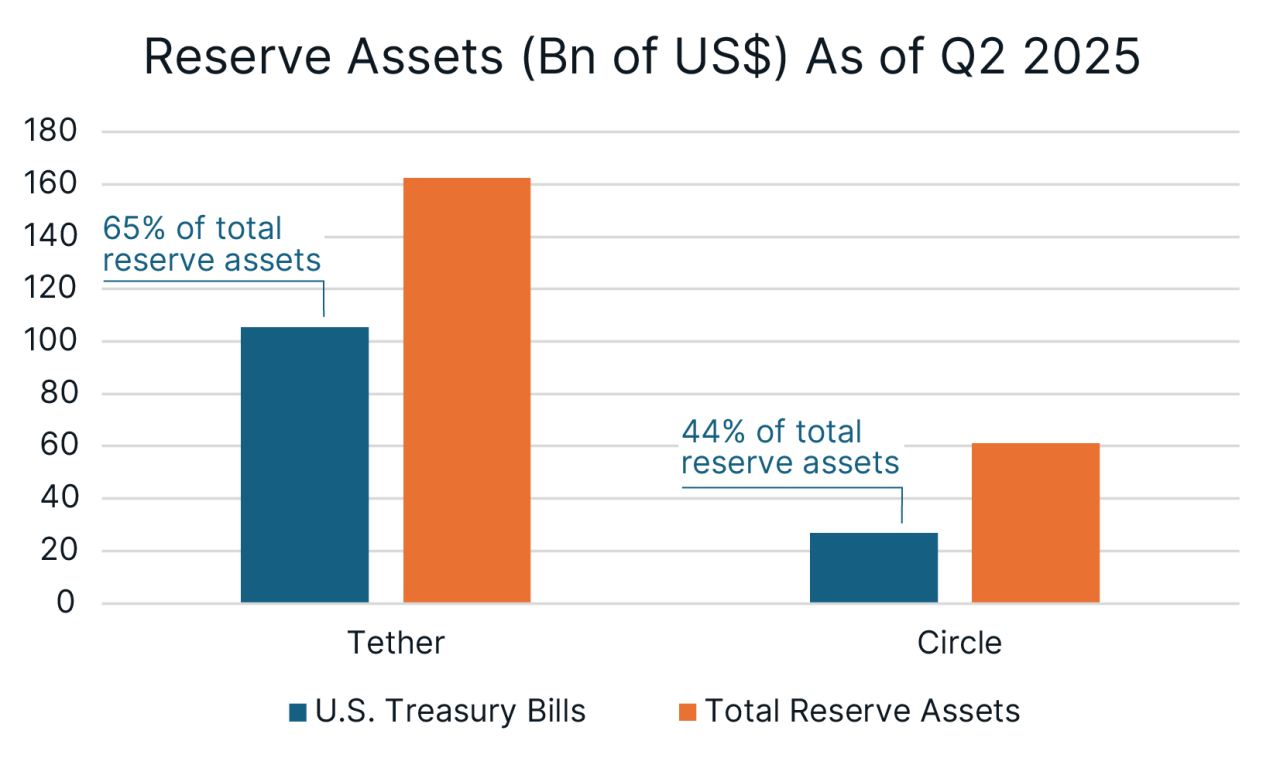

For instance, as of Q2 2025, Treasury bills accounted for 65% of reserve backing for Tether and 42% for Circle (Chart 2). The rest of the assets in reserves are split between repurchase agreements, cash and bank deposits, Bitcoin, and precious metals.

In our view, the potential growth in stablecoins will not have a meaningful impact on the US dollar or Treasuries for the following reasons:

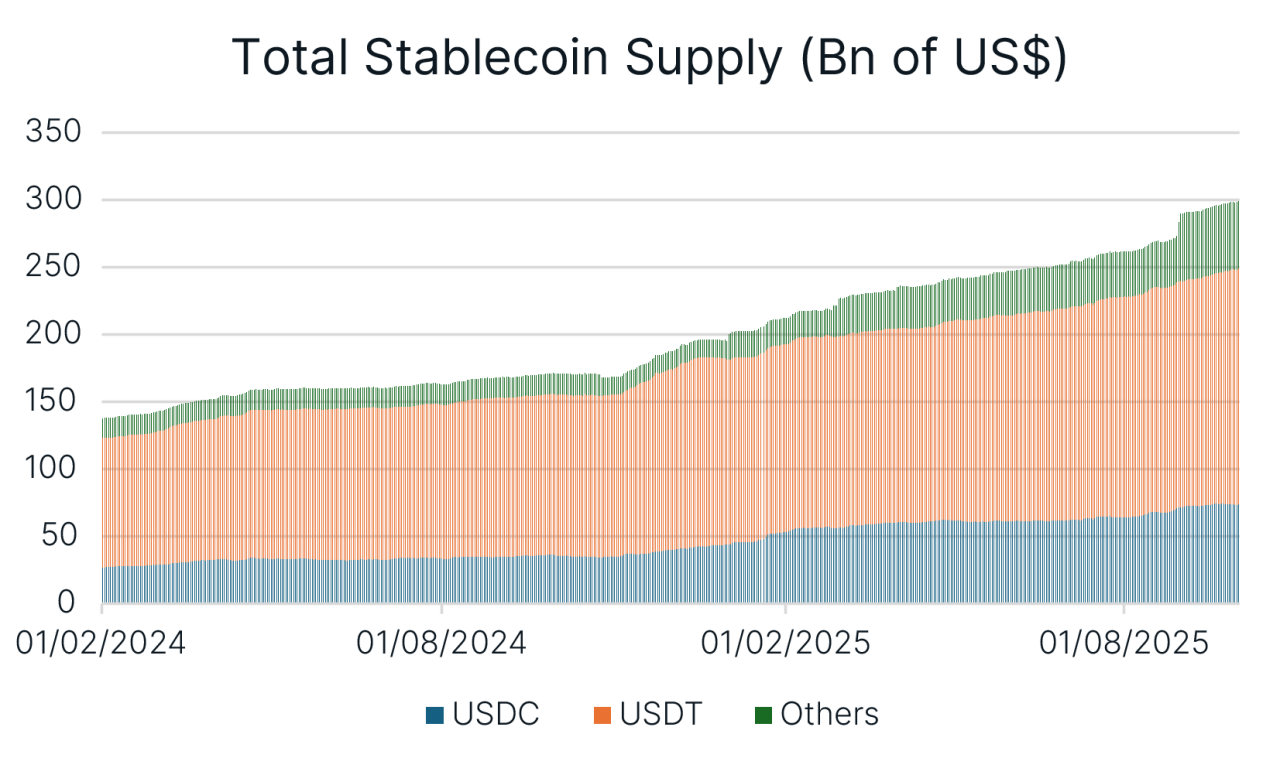

Firstly, stablecoins capitalization will remain relatively small. Even under the overly optimistic scenario of a $2 trillion market in stablecoins, it is still dwarfed by the $9.6 trillion in daily foreign exchange turnover, nearly $6 trillion in outstanding Treasury bills, and over $28.4 trillion of total supply of Treasury securities. Moreover, the Treasury market will only get bigger as the Congressional Budget Office projects US debt to swell by roughly $23 trillion by 2035 to $52 trillion.

Secondly, stablecoins inflow will likely be recycled money, not fresh capital. Stablecoins are prohibited from paying any interest or yield (whether in cash, tokens, or other consideration) and do not benefit from Federal Deposit Insurance Corporation (FDIC) protection - which insures deposits up to $250,000 per depositor, per ownership category at FDIC-insured banks. As a result, stablecoins offer limited incentives for new investors to move bank deposits or physical cash into them.

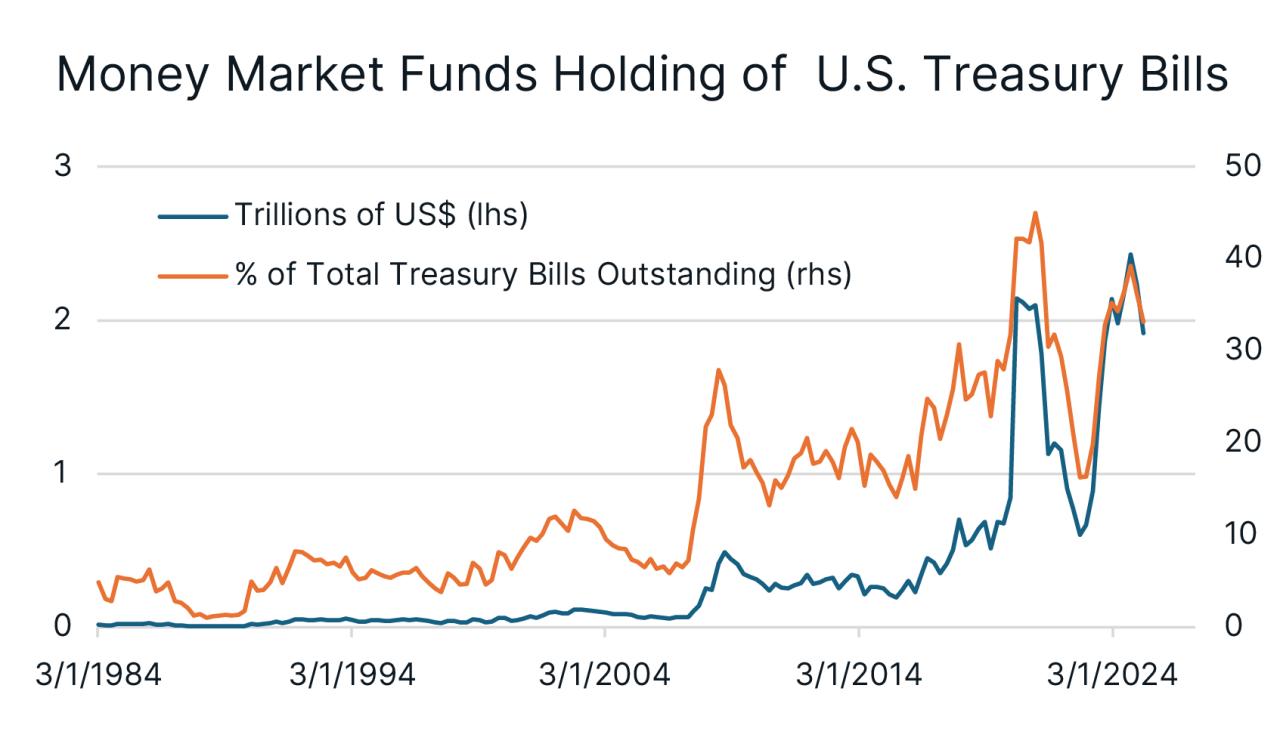

Instead, stablecoin inflows will largely be dependent on funds being shifted from existing money market funds given their overlapping characteristics. Like stablecoins, money market funds are not covered by the FDIC and are largely backed by Treasury bills.