Dodd-Frank legislation, interagency guidance on leveraged lending, required capital boosts, and liquidity requirements have all shifted banks away from lending to leveraged and smaller companies and below-super-prime borrowers. Hence the prominence and growth of independent finance companies, and their related BDC, collateralized loan obligations (CLO), and asset-backed securities (ABS) financing sources, over the last 15 years.

Another change agent is the dynamism and vast capital of the private equity (PE) and private credit ecosystem, which finances not just the borrowers marginalized by the banks but also competes directly for the larger loans and prime borrowers that banks target. The pace of business and structural development in privates is far more rapid than at the utility-like banks, suggesting privates’ outsized growth and competitive pressure may continue, particularly as investors discover value in direct private opportunities.

A final force is the continued evolution of securitization as both financing source and investment, along with its supporting legal framework. Like any technology, the structural safeguards and flexibility afforded by securitizations have evolved and improved through successive market tests like the GFC and the COVID-19 pandemic. The bankruptcy-remoteness of securitization trusts continues to be definitively affirmed by U.S. courts. Application of ABS, commercial mortgage-backed securities (CMBS), CLOs, and other securitizations should continue to outpace broader lending market growth.

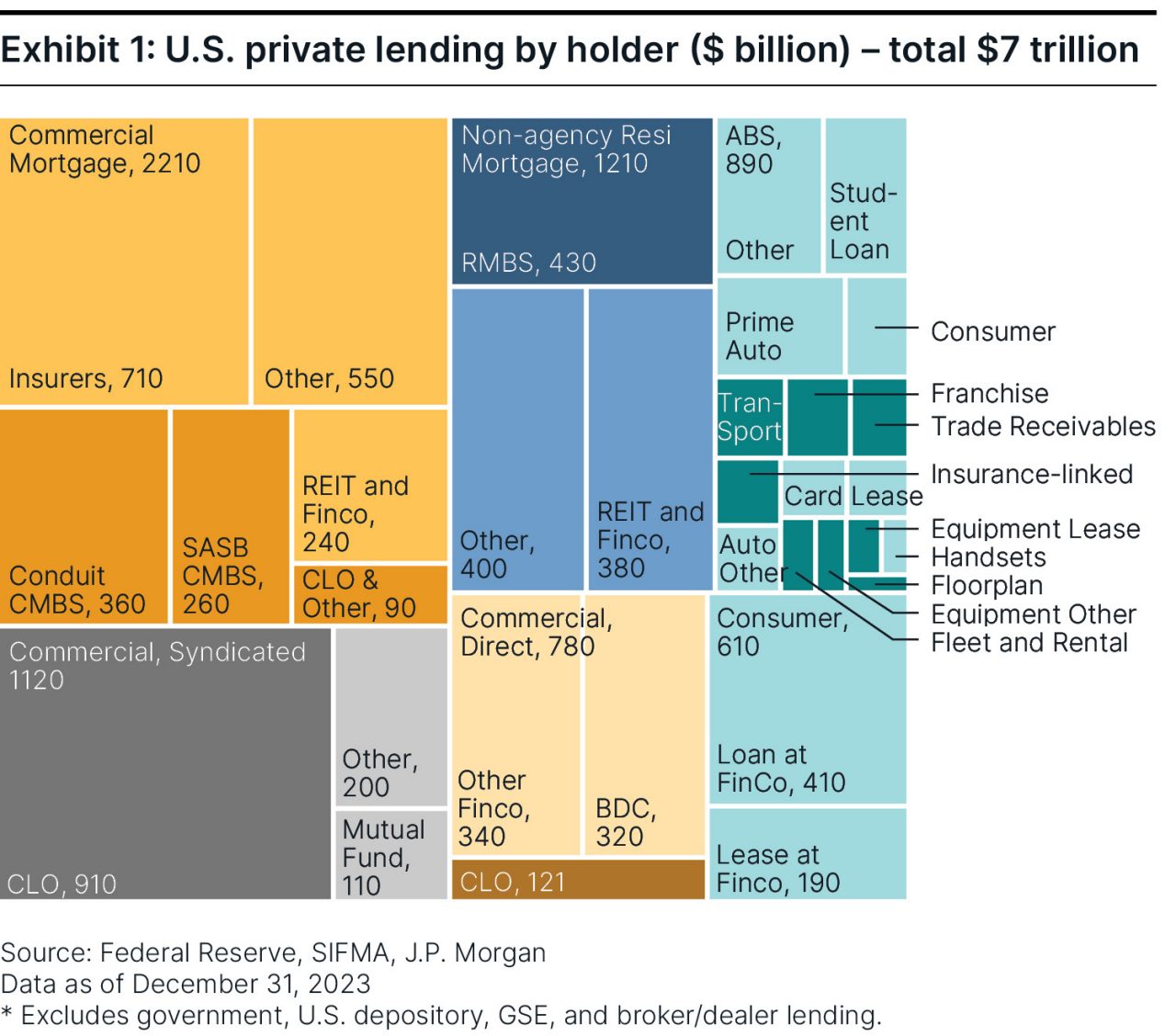

The evolution of the nonbank ecosystem

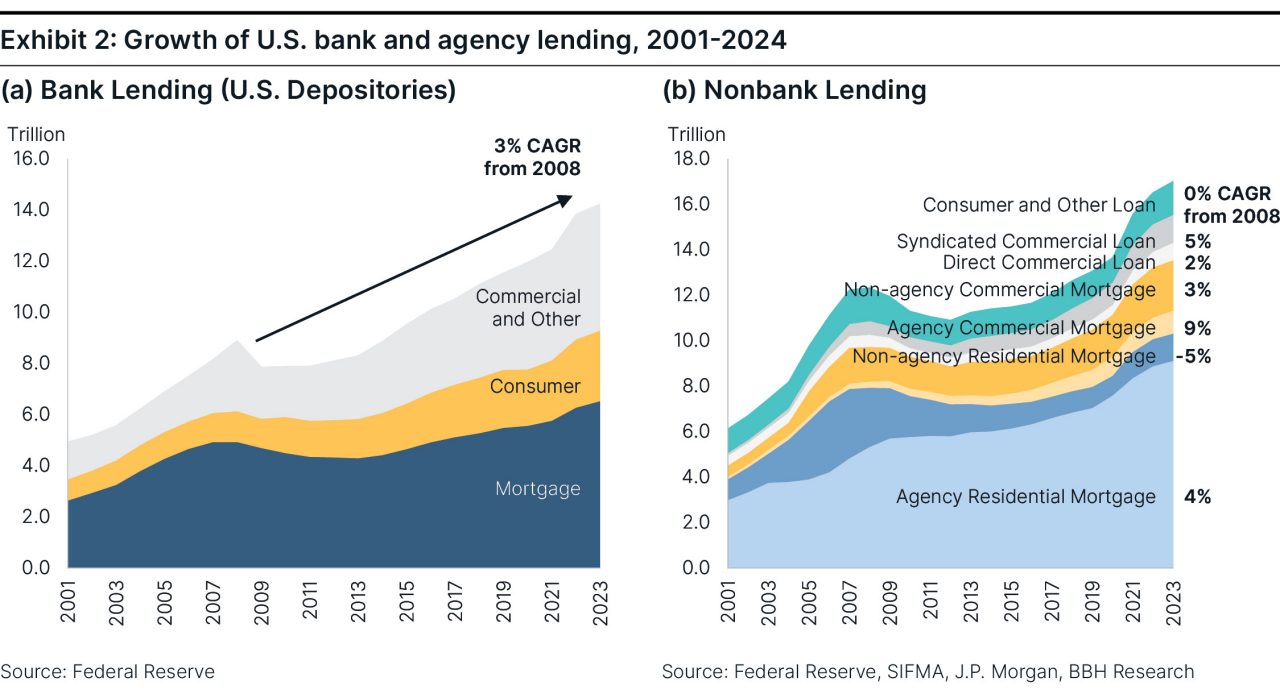

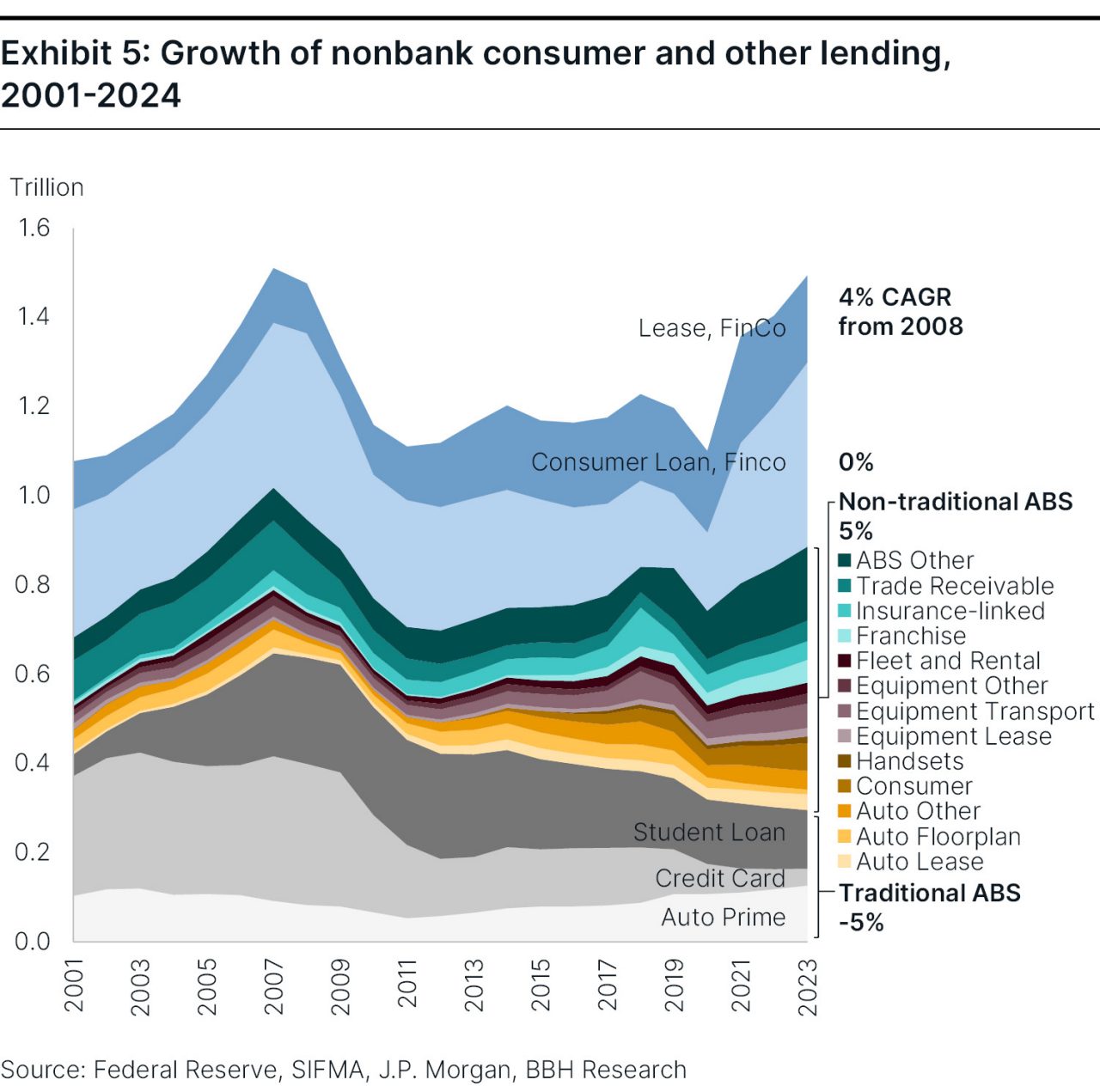

It’s useful to chart not just the current landscape of NBL but also its evolution over the last 20 years. Oddly, annual growth in the “dynamic” nonbank sector (2% annual) has trailed bank lending (3%) since the GFC. Hence, each sector is about the same size as it was at the end of 2008, adjusting for inflation.

The stall in bank lending growth is understandable. Since the early 1990s, consolidation has magnified average bank size. A greater share of a typical bank’s business is focused today on large commercial customers and higher quality consumer borrowers than in the past. Post-GFC regulation forced banks to de-lever, exit their higher leverage loans, and hold more liquid securities at the expense of loans. Large systemically important banks are capped in size, while the deposit stability advantage of regional and smaller banks has recently come into question.

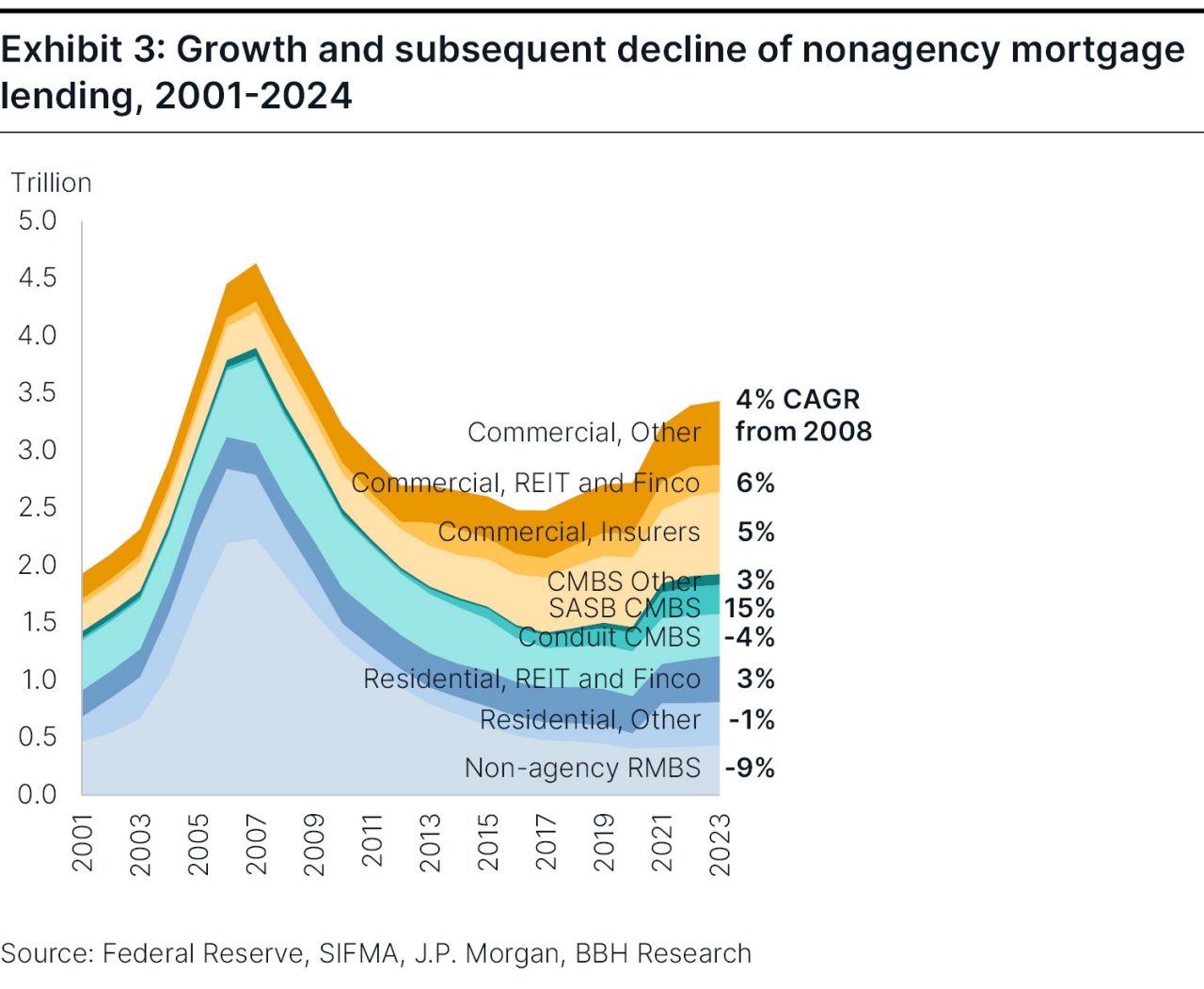

The slower growth of NBL since the GFC is more surprising. It’s a compositional effect from the burst of the early 2000s bubble in nonagency mortgage lending, which had reached $3 trillion in size by 2008. As housing prices declined, mortgage performance deteriorated, new origination shut down, and the sector cratered to its $1 trillion size today.

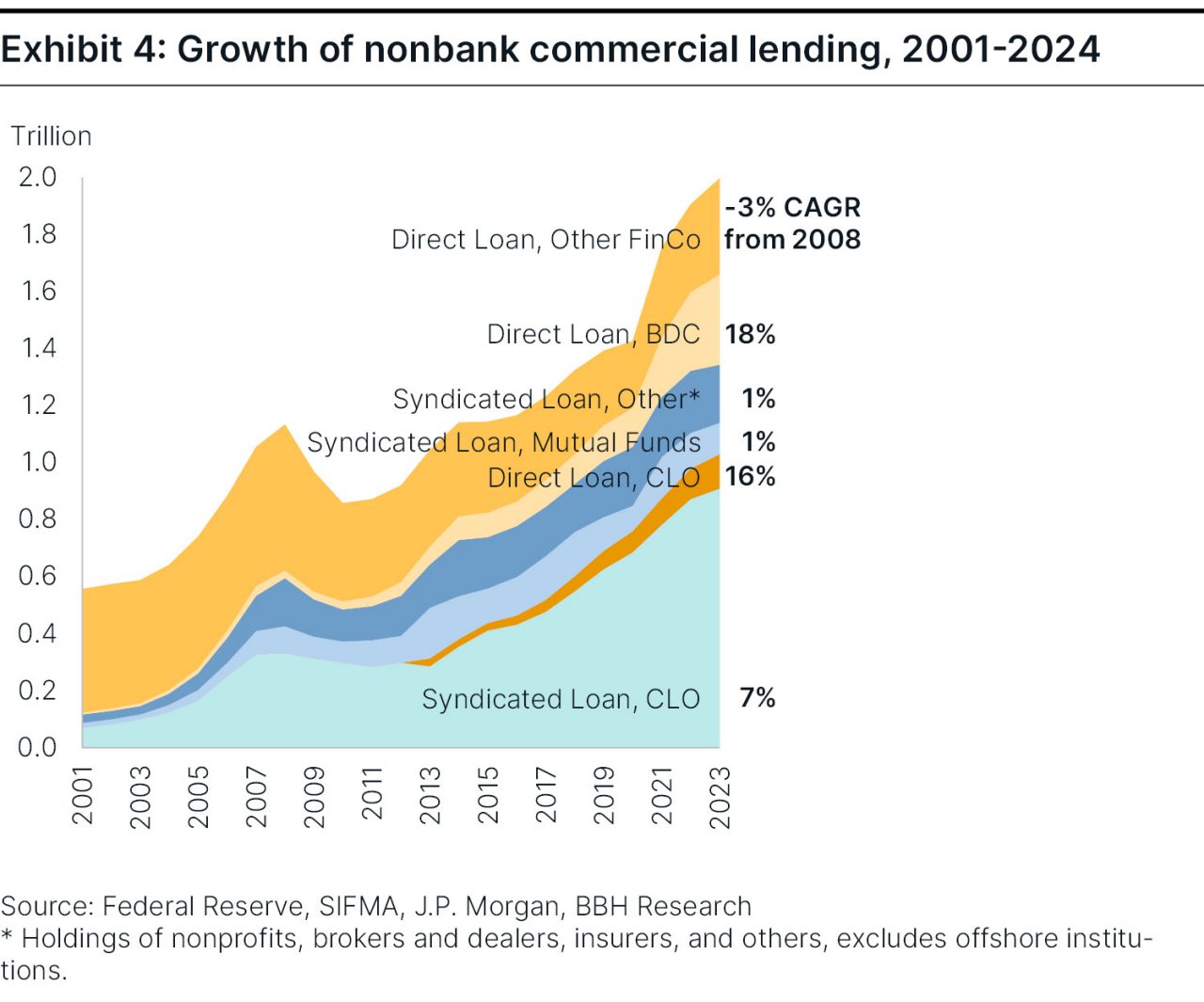

Remove residential mortgages and one finds that the other segments of NBL have grown like or faster than bank loans. NBL growth has hastened particularly in the last five years: agency pools by 6% annually, nonagency commercial mortgages by 6%, syndicated commercial lending by 7%, direct commercial lending by 11%, and by 10% or more in many specialized lending segments commonly financed with ABS (e.g., consumer installment, auto and equipment lease, franchise, data centers and fiber, venture and recurring revenue debt, rental and fleet, and other specialized segments).

NBLs have stepped in where banks have retreated, particularly in middle-market commercial lending, personal lending to below-super-prime borrowers, and specialized lending. New required disclosures have shrunk the number of U.S. exchange-listed companies. In reaction, new lending models are being pioneered by private lenders to be more flexible in underwriting. PE and credit providers are filling the gap left by the banks and exchanges.