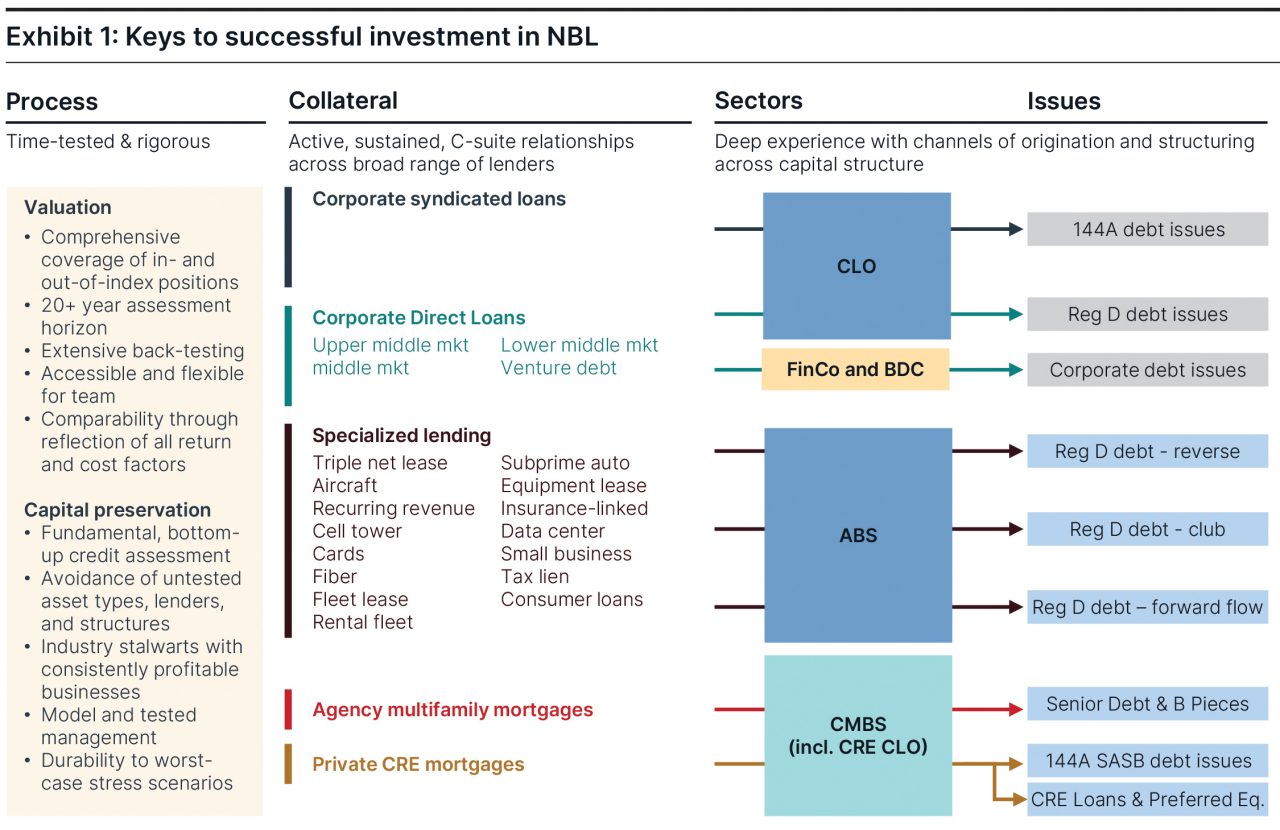

A table describing the keys to successful investment in NBL, from process (time-tested and rigorous) to collateral (active, sustained, C-suite relationships across broad range of lenders), to sectors and issues (deep experience with channels of origination and structuring across capital structure).

Expanding horizons in U.S. nonbank lending

The U.S. has the most dynamic financial system and capital markets in the developed world. Borrowers and lenders can access and extend credit through plentiful bank and capital market channels. The Global Financial Crisis (GFC) and its legislative repercussions curtailed banks’ risk-taking activities. Nonbank lenders (NBL) stepped into the vacuum, growing and evolving to maintain the credit creation vital to consumer and economic health. Yet as its economic importance grows, much of the NBL sector remains poorly understood and sparsely invested, offering investors attractive compensation amidst some unfamiliar risks.

In a series of whitepapers, we dive into the NBL sector and its opportunities. Here, we discuss a prudent time-tested approach to applying the BBH investment principles across the vast landscape of NBL.

Investing against loan portfolios would seem entirely different than corporate and municipal investment. Based on 150 years of credit investing at BBH, we find that certain investing principles hold true for all types of debt:

- A priority of preserving investors’ capital

- The necessity of thorough fundamental position-level research

- Assurance of durability to worst-case conceivable macroeconomic and industry stress

- Ceaseless risk-adjusted value focus in longer-horizon context

- Fullest access to and transparency with issuers’ senior management

Alongside proper analysis, abundant sourcing (i.e., having deep issuer relationships and the widest channels of origination) is likewise critical to investment success.

Capital preservation focus

For loan-related investing, preserving capital means avoiding the risk of credit loss by:

- Sticking to decades-established lending products with stable observed industry loss experience through crisis periods (e.g., the 1980s recession, the 2000s dot-com bubble, the GFC, the commodity collapse of 2014, and the COVID-19 pandemic)

- Investing only in loan and lease pools of profitable well-established lenders with time-tested management teams, stable underwriting criteria over time, and observable performance data extending back through periods of extreme stress

- Requiring “skin in the game,” i.e., investing only against pools where the lender has a substantial, pivotal first-loss position, and aligning incentives appropriately

- Investing with lenders where a strong channel of communication and trust exists with the management C-suite

- Thoroughly reviewing transaction documents and structural safeguards

- Seeking to assure that investors’ capital is preserved in the most severe conceivable macro and industry stress1

These strict criteria may seem to rule out a swath of attractive lending opportunities. Likewise, a great deal of industry experience and time-consuming research is necessary to implement them; however, examples prove that deviating from any one of these may result in substantial loss.

A common alternative approach to these criteria is simple breakeven analysis. Position-level structural safeguards and credit enhancement would seem to protect an investment at, say, two times or three times modeled base case loss. Little analysis of asset type, lender, or pool need be performed. We strongly caution against this narrow approach. In our approach, elevated risk of capital loss isn’t acceptable in credit investing.

While principles for investing may be common across debt types, the process for assuring capital preservation in loan-based investments is different in some ways. Corporate analysts assess a company’s ability to generate cash flow to repay its debt, while asset-based investors ensure that pools of loan assets (i.e., the collateral) generate sufficient cash flow to comfortably meet debt service or expected return targets. Cash flow durability is assessed using deal structure analytics tools and applying proprietary models to stress-test cash flows across economic stress scenarios. A key advantage to investing in these markets is that the assets are typically held in a bankruptcy-remote vehicle, which can shield from many external risks.

The importance of a strong lender sponsor is often under-appreciated in the credit underwriting process. Partnering with trusted and long-established sponsors of securitizations historically leads to better investment outcomes. When sponsors retain an economic stake, it aligns their interests with investors and provides a strong incentive to maintain collateral performance. Working with long-established sponsors provides an added benefit of access to comprehensive data sets, important in due diligence. A thorough review of transaction documents is necessary to ensure that cash flows are distributed appropriately and fairly across the capital structure. Finally, it is important to have structural safeguards within the investment structure, so that as a collateral pool may begin to underperform relative to expectations, mechanisms can redirect cash flows as needed to ensure equitable distribution.

Valuation focus

Having narrowed investments to those highly likely to return capital, a rigorous, consistent valuation framework is important to order and size positions for portfolio construction. Based on long experience and extensive back-testing, we believe a suitable valuation approach should be:

- Comprehensive: It is important that a valuation framework encompasses and accurately treats the entire universe of lending-related opportunities. Given its vast size and complexity, this is a challenging proposition that requires familiarity with and access to the dozens of segments in this market, as well as historical experience with pricing metrics and product evolution. An effective framework should include not just outstanding index- and exchange-listed positions, but also new issue, over the counter, private, and restructured trades. For scope, our quantitative team values over 9,000 potential positions daily.

- Consistent: Arguably the greatest challenge in valuing loan-backed investments is appropriate comparison across the medley of disparate investment types. Experience and ample data are needed to adapt each investment type to the important metrics (see below) that allow common comparison. Care must also be taken in defining the ultimate value measure on which to order and size (for example, we use cost-adjusted one-year expected return over Treasuries).

- Inclusive: Making investments on simple value metrics can be a particular problem in the lending space, exposing investors to misleading compensation or omitted costs. For example, a collateral loan obligation (CLO) spread margin can paint too rosy a picture of expected performance. Long experience suggests that a useful framework should at the least reflect carry, potential price and spread change, and roll-down on the return side; and expected credit loss, liquidity, optionality, volatility, and effective tax rate on the cost side.

- Focused on the long view: Our experience suggests that investing based on relative value across opportunities at a given point in time is misleading and dangerous. While no evaluation horizon is perfect, our back-testing and performance suggests it’s effective to evaluate current compensation against long-term 25-year average levels and volatility for securities at the same industry/asset, same rating, and similar maturities. Although simple in concept, implementing this requires a skilled quantitative team analyzing constituent-level index data over several decades.

- Rigorously applied: An effective framework should be the key tool in a team’s investment process, applied without exception, providing a common viewpoint among portfolio managers (PMs), analysts, and traders. Buy and sell decisions should follow the valuation metric and positions should be sized in portfolios accordingly.

- Handy: For effective use, valuation results should be at hand through a simple yet versatile interface. To accommodate secondary and new issue loans, valuing novel positions and variants should be quick and easy. A dedicated quantitative team needs to continually adapt the framework for developments in markets, new investment types, and recent market data.

Without applying an appropriate valuation framework, investment in lending-related opportunities is likely to be uneven and volatile at best, and costly at worst.

Abundant sourcing

While capital preservation and valuation focus are necessary for investment success, access to markets and origination capability are key to exploiting value. Effective origination of loan-based investments requires strong direct relationships with the senior management of hundreds of lenders – much more so than in corporate credit.

In loan-backed sectors, issuers are frequently private companies in specialized markets that seek and value direct investor relationships rather than rely on the dealers’ broad syndication process. The investor set is smaller and more concentrated. Lenders are accordingly incentivized to understand their investor’s individual appetites and conditions, and dealers are often asked to show issuance just to a club of investors rather than market widely. Seeing the range of opportunities is impossible without existing familiarity and relationships with the sizable issuer universe, a major barrier to inexperienced investors.

Nor do the largest investors generally have an advantage. To the contrary, smaller deal sizes below $500 million offer them limited opportunity. Issuers are more in control of syndication and tend to allocate favorably to consistent investors, not be directed by banks to the largest bond buyers, as in corporate markets. Frequent issuers may still have brought just a dozen or fewer transactions to market, reinforcing their loyalty to their earliest and most consistent investors. These investors typically have earliest notice of new transactions, greater opportunity to participate in private deals via reverse inquiry, and more encouragement to structure private transactions and whole loan purchases.

Dealer channels: The vast bulk of loan-related investments, both more and less traditional, are issued and traded through commercial bank dealers. Given the specialized nature of investing in nonagency mortgage, commercial loan, and consumer opportunities, a reputation for investing and personal experience with the dealer, banking, and syndication desks is important. Frequent investors’ opinions of the banks are important to issuers, reinforcing their influence.

In the more traditional agency mortgage-backed securities (MBS), cars and cards ABS, conduit CMBS, and bank-syndicated loan (BSL) CLO markets, issuers’ programs may be more established and investor numbers higher, lessening the importance of an investor’s historical presence in the market. In the less-traditional public and private markets, existing relationships with dealers and issuers are essential to seeing opportunities and allocations. Bid-side liquidity is often decent, but given the importance of insurers and other buy-to-hold investors in many less-traditional loan-backed investments, secondary availability is low, which further raises the importance of issuer relationships in the primary issuance market.

Private channels: There are multiple approaches to accessing private opportunities:

- A reverse inquiry, or directly engaging with a lender or asset originator to shape the asset pool and structure the transaction

- Working with a financial intermediary, such as an investment bank or broker-dealer, which syndicates a private investment to either a single investor or a small club of investors

- Here, the assets backing the private investment can come directly from bank’s balance sheet or from the lender with whom they have the relationship

- A forward-flow agreement, where an asset originator agrees to provide a predetermined number of future originations over a specified period to an investor

While there are several ways to source and structure private investments, having strong relationships with key players in the market is essential. Such relationships generally develop over time by teaming up on multiple transactions.

A major advantage of private investments vs. a public offering for buyers and sellers is the ability to customize and streamline the process. Familiarity between parties involved can create trust and ease the process.

Private debt investors should be mindful of the structural safeguards, and conduct thorough reviews of underwriting standards on the asset pool, as some lenders may sacrifice underwriting quality to expedite deal closings. Caution is warranted in private transactions, where alternative managers are securing the loan assets of an owned or affiliated documentation and support.

Conclusion

A prudent approach to loan-based investing demands rigorous credit analysis, robust valuation frameworks, and deep relationships with trusted lenders. By prioritizing capital preservation and sourcing investments through well-established channels, investors can navigate the complexities of NBL with confidence. Success hinges on discipline, transparency, and long-term alignment between issuers and investors.

The author would like to thank Thomas Brennan, John Ackler, Tim Rourke, Chris Ling, Vaidas Nutautas, and Anthony Sylvester for their contributions to this piece.

Contact Us

1 A typical BBH stress is to 1930s Great Depression-level conditions, including prolonged 25% unemployment

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved. PB-08872-2025-08-28