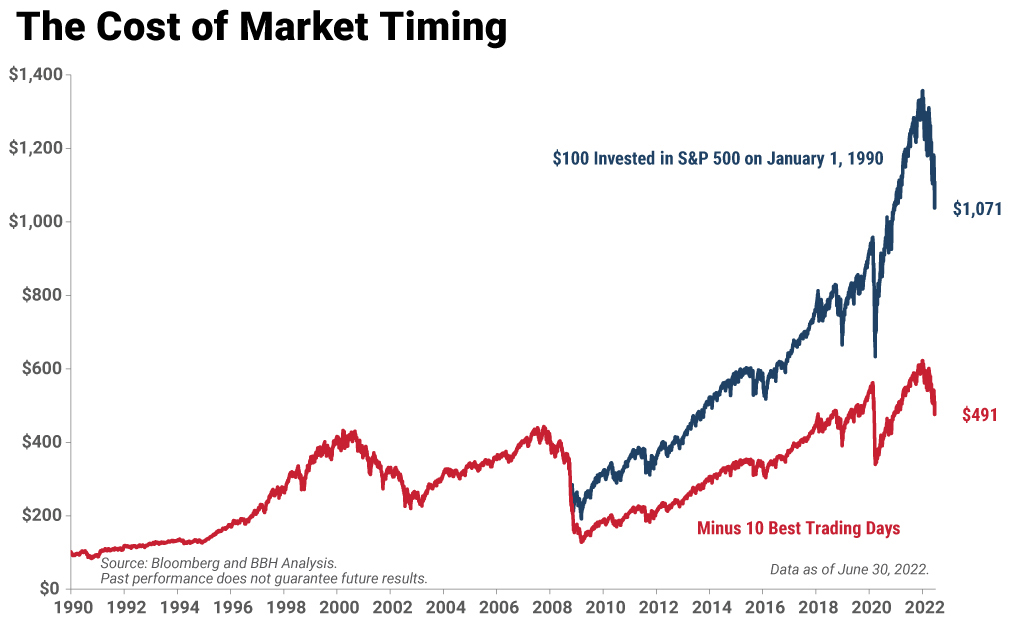

A cynical reader of this analysis might understandably respond, “Ah, but you’ve cherry-picked the 10 best days to remove from the analysis. I wouldn’t be so foolish as to miss out on the best days!” Behavioral psychology argues otherwise. The perverse reality is that all 10 of these days occurred during either the global financial crisis or the early days of the COVID-19 pandemic, amid market environments in which news flow was awful. To make matters worse, many of these “best” days happened in close proximity to the “worst” days, exacerbating the psychological stress of market timing. As a single example, consider the second week of March 2020, when the fog of pandemic uncertainty was settling thickly over the world. The S&P 500 dropped 9.5% on March 12, rebounded 9.3% on March 13, only to fall again by 12% on March 14. U.S. equities looked like an emerging market for a few weeks. Trying to time such concentrated volatility is impossible, and failure is expensive.

Complicating the timing challenge, bear markets usually end well before headlines turn positive. The market bottom in the global financial crisis took place in March 2009, although the government had just raised its stake in Citibank to an unimaginable 36%, evidence that the banking crisis was far from over. The recession continued into the summer of that year, and the unemployment continued to rise through October, touching 10% at the peak. Despite the drumbeat of bad news throughout the year, the S&P 500 rose 68% from the March bottom through the end of 2009.

In the most recent cycle, the market bottomed on March 23, 2020, a date on which the United States was closing its borders to international air travel in order to combat COVID-19, and New York City was building a field hospital in Central Park. There were no vaccines or treatments, and the global economy had all but ground to a halt. Once again, the news flow was apocalyptic. Nevertheless, from that date, the market rallied 70% through the end of the year.

The good news is that ultimately timing isn’t all that important, at least for a long-term investor. Let’s flip the script and consider the hypothetical investment experience of the unluckiest investor imaginable. What if you invested all your money in the S&P 500 the day before the World Health Organization declared COVID-19 a pandemic? Your near-term returns would have looked awful, but patiently holding that stake through June 30, 2022, would have resulted in a total return of 16%, or 9% annualized. Investing in the equity market the day before Lehman Brothers declared bankruptcy would have been similarly painful for close to a year, but you would nonetheless have made 320% since then, or 16% compounded. One last example: Investing all your money into stocks the day before 9/11 yielded a return to date of 420%, or 12% compounded, despite the aftereffects of 9/11, the entirety of the global financial crisis, a worldwide pandemic and whatever we’re going through now.

It's not about timing the market. It’s about time in the market.

The idiosyncrasy of market cycles makes it impossible to identify peaks and bottoms in the moment. Instead, your asset allocation should strategically reflect your liability allocation. What you need your money to do for you (and when) determines how the funds should be allocated, and that allocation should change only if your needs change. For example, if part of your portfolio is needed to meet nearer-term spending needs, those assets are best deployed in shorter-term and higher-quality fixed income, or even cash. These assets offer modest returns but plenty of liquidity. On the other hand, assets intended to fund longer-term needs, such as retirement, legacy spending, philanthropic goals and so forth, need to be protected against inflation, which requires more of an equity exposure.

Market volatility does have implications for rebalancing, as diverging returns may drive asset allocation out of balance. Not only does rebalancing help to restore a long-term strategic allocation, it usually requires an investor to add to assets that have underperformed and perhaps sell assets that have outperformed. The discipline of selling into strength and buying into weakness, although psychologically taxing, is an added ingredient of investment success.

Implications for Investment Allocation

Whereas elevated price volatility and bear markets don’t have a direct implication for asset allocation, market disruptions do influence investment implementation. To be successful in the long run, an investor must assess the fundamental quality of an asset, and then wait for the market to price that asset at an appropriate discount to its intrinsic value. Quality alone is not enough: Buying a good asset at the wrong price is a surefire way to lose money. All else being equal, rising price volatility means that more assets are trading at a discount to their intrinsic values, thereby providing more opportunities for the patient and disciplined investor to exploit the difference between price and value.

The efficient market hypothesis argues that price and value shouldn’t deviate, or, if they do, the difference should be quickly competed away in a market where information is instantly disseminated and rapidly incorporated into prices. This arbitrage increasingly doesn’t even require human action, as algorithms and artificial intelligence can digest news and update price models in a literal blink of an eye. The so-called “strong” form of the efficient market hypothesis therefore concludes that there is no exploitable gap between price and value, and that active management is futile.

Empirical data doesn’t bear this out. From 1990 through 2021, the intra-year price volatility of the S&P 500 has averaged 29.3%, calculated as the difference between the highest and lowest price points of the year, regardless of when they occurred. For comparison, the same analysis of corporate earnings reveals average annual volatility of 19.9%. Stock prices, therefore, show more volatility than earnings, and both show far more volatility than changes in nominal GDP, where the intra-year volatility is a mere 4.0% (even including the sharp drop and recovery of the pandemic). This range of price volatility calls into question how efficient markets actually are. The price of U.S. stocks may fluctuate 29.3% on average, but it is impossible to believe that the underlying value demonstrates similar volatility.

Investor sentiment explains the conundrum. Market prices reflect fundamentals plus the entire range of human emotions – fear, greed, hope, excitement, anger, despair and so on. Markets are ultimately only as efficient as people are. People are generally efficient, but not all the time, and markets are therefore generally efficient, but not all the time. A weaker form of the efficient market hypothesis holds that markets tend toward efficiency over time but that emotions cause prices to overshoot on the upside and the downside, as emotions swing from unbridled optimism to abject despair. Herein lies the opportunity for the patient and disciplined investor in the present market environment.

An old adage in the investment business holds that the secret to success is to buy low and sell high. What this simple adage doesn’t capture is the psychological challenge inherent in this approach. If done correctly, neither action should feel comfortable. We are a herd species; we take comfort in being part of the crowd. To buy what others are selling, or sell what others are buying, is to go against the crowd and stand alone, which is psychologically unsettling. Hence the importance of discipline, which can act as an antidote to the vagaries of human emotion and allow an investor to benefit from price volatility rather than be victimized by it.

Price volatility is the friend of the patient and disciplined investor.

Parting Thoughts

We observed earlier that the 20% drop in the S&P 500 for the first half of 2022 was the worst first half for equities since 1970. The comparison is ominous, as investors rarely look back fondly on the economic or investment environment of the 1970s. The business section of The New York Times for July 1, 1970, offered the following bleak outlook:

At midyear the United States economy is sliding into a recession. Unemployment, which reached 5 per cent of the labor force in May, almost certainly climbed higher in June. With hundreds of thousands of young people entering the job market at a time when employers are laying off workers, unemployment will go higher this summer and threatens to hit 6 per cent by the end of the year. The most disturbing aspect of the immediate economic outlook is the sag in spending on industrial and commercial construction and on inventories. A fall in business investment would turn this mild slump into something more serious.

[New York Times, p. 44, The Economy at Midyear, 1 July 1970.]

Not the most obvious investment environment to say the least. Yet someone who invested in the S&P 500 on the date of this article would have enjoyed a 29% return by the end of the year, 41% over the subsequent full year and 57% over the next three years. Don’t let headlines determine your investment approach.

Economic uncertainty and market volatility is unpleasant. Yet time and again history demonstrates that price volatility is a feature of financial markets, not a bug, and the ability to withstand the slings and arrows of outrageous ups and downs is essential to long-term investment success.

Keep calm and carry on.