Chart depicting two different paths to retirement, one with full max/parent-help, and one with half max/no-help. In the end, the full max/parent helps results in $16.2 million in tax-sheltered accounts at age 70. The half max/no-help scenario results in $4.8 million in tax-sheltered accounts by age 70.

We often speak about ways to maximize total family wealth. There are many facets to this process, including choosing the right companies and managers with whom to invest, entering and exiting investments at the right time, setting up an appropriate asset allocation, and, of course, investing in a tax-efficient manner. As clients have undoubtedly heard us say, it takes a lifetime of 6% returns on investment to outpace income and estate tax rates approaching 50%. For this reason, a responsible wealth management discussion includes not only asset allocation but, perhaps more importantly, asset location. The more you can transfer to charity, children, grandchildren, and others during life, especially into income tax-favored accounts, the less you will transfer to federal and state governments at your death.

Many raise objections to estate planning. Some worry that complex planning may inadvertently disincentivize their children and grandchildren from becoming hard-working, productive members of society. Others feel their financial lives are overly complex and are hesitant to put additional structures in place. No matter your objection to estate planning, if you are interested in transferring wealth to the next generation in a tax-efficient way with no long-term commitment, trusts, or legal fees, read on!

Objection 1: “I get it. I want to transfer assets to my children and grandchildren, but my financial life is already too complex. I understand the value of trusts, but it’s too much trouble to set them up and keep track of ongoing administration."

We hear you! There are some very simple ways to transfer significant wealth to your family during life without complex planning structures, thereby increasing the overall wealth transferred to children and grandchildren and decreasing taxes paid.

As an example, meet Mr. and Mrs. Client, a married couple in their 60s. They have two children, Son and Daughter, both of whom are married. They have three young grandchildren, all of whom currently attend nursery school.

To the chagrin of their wealth planner, Mr. and Mrs. C do not have the time or patience for grantor retained annuity trusts (GRATs), spousal lifetime access trusts (SLATs), or qualified personal resident trusts (QPRTs). The documentation and annual interest payments required for an intra-family loan make them cringe. Despite (or because of!) these feelings, they were savvy enough to call their relationship manager and set up some automatic payments to take advantage of the medical, educational, and annual exclusions from gift tax. Here is a copy of their annual account statement for the first half of the year.

Date | Description | Amount |

1/1/2025 | Paid to Account XXX f/b/o Daughter - 2025 Gift | $38,000 |

1/1/2025 | Paid to Account XXX f/b/o Son-in-Law - 2025 Gift | $38,000 |

1/1/2025 | Paid to Account XXX f/b/o Son - 2025 Gift | $38,000 |

1/1/2025 | Paid to Account XXX f/b/o Daughter-in-Law - 2025 Gift | $38,000 |

1/1/2025 | Paid to 529 Plan f/b/o Grandson1 - 2025 Gift | $38,000 |

1/1/2025 | Paid to 529 Plan f/b/o Granddaughter - 2025 Gift | $38,000 |

1/1/2025 | Paid to 529 Plan f/b/o Grandson2 - 2025 Gift | $38,000 |

1/1/2025 | Paid to United Healthcare - Medical Insurance Premium for Daughter and Family | $2,200 |

1/1/2025 | Paid to Blue Cross - Medical Insurance Premium for Son and Family | $2,000 |

1/1/2025 | Paid to Aetna - Dental Insurance for Daughter and Family | $150 |

1/1/2025 | Paid to Aetna - Dental Insurance for Son and Family | $100 |

2/1/2025 | Paid to United Healthcare - Medical Insurance Premium for Daughter and Family | $2,200 |

2/1/2025 | Paid to Blue Cross - Medical Insurance Premium for Son and Family | $2,000 |

2/1/2025 | Paid to Aetna - Dental Insurance for Daughter and Family | $150 |

2/1/2025 | Paid to Aetna - Dental Insurance for Son and Family | $100 |

3/1/2025 | Paid to United Healthcare - Medical Insurance Premium for Daughter and Family | $2,200 |

3/1/2025 | Paid to Blue Cross - Medical Insurance Premium for Son and Family | $2,000 |

3/1/2025 | Paid to Aetna - Dental Insurance for Daughter and Family | $150 |

3/1/2025 | Paid to Aetna - Dental Insurance for Son and Family | $100 |

4/1/2025 | Paid to United Healthcare - Medical Insurance Premium for Daughter and Family | $2,200 |

4/1/2025 | Paid to Blue Cross - Medical Insurance Premium for Son and Family | $2,000 |

4/1/2025 | Paid to Aetna - Dental Insurance for Daughter and Family | $150 |

4/1/2025 | Paid to Aetna - Dental Insurance for Son and Family | $100 |

5/1/2025 | Paid to United Healthcare - Medical Insurance Premium for Daughter and Family | $2,200 |

5/1/2025 | Paid to Blue Cross - Medical Insurance Premium for Son and Family | $2,000 |

5/1/2025 | Paid to Aetna - Dental Insurance for Daughter and Family | $150 |

5/1/2025 | Paid to Aetna - Dental Insurance for Son and Family | $100 |

5/1/2025 | Paid to School - 1/2 Tuition for 2025 School Year for Grandson1 | $10,000 |

5/1/2025 | Paid to School - 1/2 Tuition for 2025 School Year for Granddaughter | $11,100 |

5/1/2025 | Paid to School - 1/2 Tuition for 2025 School Year for Grandson2 | $9,000 |

6/1/2025 | Paid to United Healthcare - Medical Insurance Premium for Daughter and Family | $2,200 |

6/1/2025 | Paid to Blue Cross - Medical Insurance Premium for Son and Family | $2,000 |

6/1/2025 | Paid to Aetna - Dental Insurance for Daughter and Family | $150 |

6/1/2025 | Paid to Aetna - Dental Insurance for Son and Family | $100 |

$322,800 | ||

| Full Year | $645,600 | |

Continue Program for 20 years | $12,912,000 | |

Subject to certain restrictions, individuals may pay the tuition and necessary (nonelective) medical expenses for an unlimited number of persons per year, without gift tax liability, without utilizing their annual per recipient gift tax exclusion, and without using their lifetime gift exemption. To qualify, payments must be made directly to an educational institution (for example, nursery school, secondary school, college, university, and so forth), medical provider (that is, to the providing doctor, hospital, dentist, and so forth), or to an insurance company for the payment of a medical/dental insurance premium.

Merely setting up automatic payments for annual exclusion gifts, medical care, dental care, and tuition has allowed this family to transfer over $645,000 per year to descendants, free of transfer tax or use of the federal gift/estate tax exemption (which remains available to shelter nearly $13.99 million1 of assets in the survivor’s estate). Conservatively assuming that these clients live at least 20 more years, into their 80s, even without inflation adjustments, they are able to pass over $12.9 million to their heirs free of gift tax, estate tax, or use of lifetime gift/estate tax exemption – all without a single trust agreement!

Not even factored into this calculation is increased tuition or appreciation on the annual exclusion gifts, assuming the children invest the funds in a responsible manner (a plan for which is described more fully later in this article). Based solely on this strategy, Mr. and Mrs. C will have successfully diverted nearly $13 million from the federal and state government to their family over 20 years without even contacting an attorney.

Objection 2: “$38,000 a year is a lot to transfer outright to each child and in-law. I don’t want them to quit pursuing their advanced degrees/day jobs. I value hard work and education and want to transfer not only assets, but values."

The largest portion of this program, of course, is the annual exclusion gifts Mr. and Mrs. C make each year. Under current tax rules, each individual may transfer $19,000 to any individual free of gift tax or use of lifetime exemption. This means a married couple can transfer $38,000 to each child and grandchild tax-free. In order to ensure that they transfer values as well as wealth, Mr. and Mrs. C had a family meeting with the children and in-laws in order to discuss their wishes for the annual exclusion gifts. Most importantly, they would like the children to save for education and retirement in a responsible manner.

The children and their spouses all work hard, but given their relatively new careers (they are in their early 30s) and young children, they do not currently have the cash flow to lock up liquidity in long-term tax-favored accounts. Prior to Mr. and Mrs. C setting up this annual giving program, the children were saving some, but not enough, for retirement. For example, Son was setting aside 6% of his salary and diverting it to a 401(k) account in order to take advantage of the maximum amount his company would match. He would love to set aside more; however, the balance of his after-tax salary is spent almost immediately on (deductible!) mortgage interest payments as well as diapers, childcare, and family-sized barrels of animal crackers.

Armed with the knowledge that they will receive $38,000 each, tax-free, every year, the children have the confidence to lock up some liquidity in tax-favored accounts and allow it to grow, income tax-free, for decades. Now, not only do they max out their 401(k) contributions ($23,500 each, annually), but each of them also fully funds an after-tax IRA ($7,000 annually). Finally, even though Mr. and Mrs. C are paying for private nursery school and contributing to separate 529 plans for the grandchildren, the children know they may want to have the ability to help their children with college or even graduate school tuition. Both live in New York, where a state income tax deduction is available for amounts contributed to a 529 college savings plan, up to $10,000 per married couple. Mr. and Mrs. C live in New Jersey, where such deduction is only available to those who file tax returns showing gross income of $200,000 or less. For this reason, the children and in-laws also contribute $5,000 each to a 529 plan for each of their children, for a total deduction of $10,000 against state income taxes. With this plan in place, each $38,000 annual exclusion is apportioned as follows:

Child | Child’s Spouse | |

Maximum After-Tax IRA Contribution | $7,000 | $7,000 |

Maximum Pre-Tax 401(k) Contribution | $23,500 | $23,500 |

Maximum Deductible 529 Plan Contribution | $5,000 | $5,000 |

$35,500 | $35,500 |

This plan successfully transfers dollars that would otherwise be taxed in Mr. and Mrs. C’s estates to tax-deferred retirement and educational accounts. These are funds that will be available for children and grandchildren much later in life, and, without the annual exclusion gifts, would have gone unfunded due to present liquidity needs. The impact is incredibly meaningful once Son and Daughter reach retirement age, as their accounts have been growing tax-free for 30 years. This compounded accumulation allows them to continue the family tradition and transfer wealth to their grandchildren and more remote descendants and charity without the fear that they may not have enough in their own personal names to live comfortably.

Variations on this plan work for families with younger children or older grandchildren as well. We are realistic – a 16-year-old with a summer job is taking the money he earns scooping ice cream and spending it on first dates and video games. He is not opening a Roth IRA account. However, technically he should, since anyone with taxable income is eligible to begin funding these accounts, and tax-free compounding is an incredible tool for wealth preservation and growth. Especially assuming the ice cream parlor is not paying him more than $150,000 per year for his labor, this lucky 16-year-old is eligible to fund a Roth IRA, which grows income tax-free and does not require minimum distributions at any time. A parent or grandparent who is interested in tax-efficient wealth transfer can give IRA money to the 16-year-old, with the understanding that he will fund the account, invest it, and not touch it until retirement.

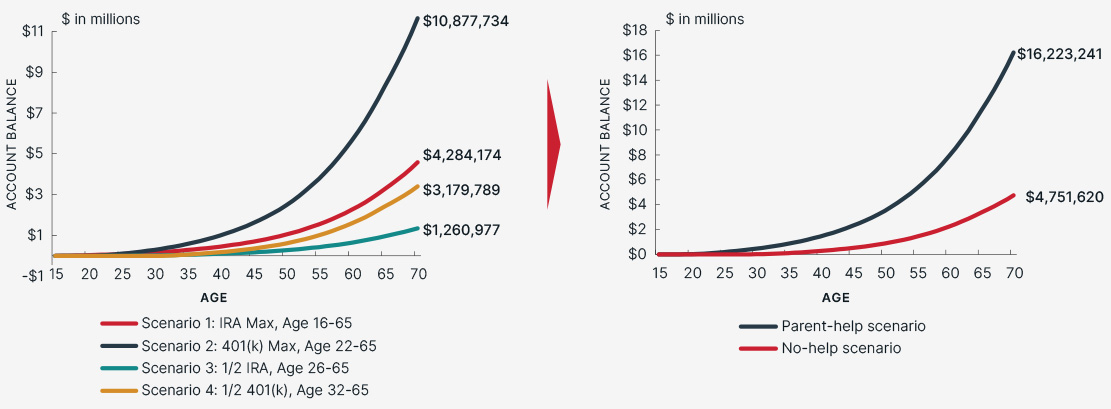

Two roads to retirement: Parents help vs. you’re on your own

Full Max/Parent-Help Scenario: In this chart, the child is able to max out both types of retirement accounts every year with help from her parents. The IRA starts at age 16 (i.e., when she has income from part-time jobs). The 401(k) starts at 22 – when the child graduates college/gets her first “real” job. This results in a total amount in tax-sheltered accounts by age 70 of $16.2 million. Half Max/No-Help Scenario: Here, the child does her best and opens her retirement accounts once she has more of a cushion – 10 years after the child who starts at the earliest possible age (26 for IRA and 32 for 401(k)). Every year after opening it, she contributes half the maximum amount. This results in a total amount in tax-sheltered accounts by age 70 of $4.8 million. In the end, the “no-help” child is still doing a fairly good job in saving half of the maximum starting relatively early. The true comparison is the child who does not put anything away for retirement – in this example, resulting in $0 in tax-protected retirement funds at age 70, vs. $16.2 million in the “parent-help” example. This hypothetical example is for illustrative purposes only. It assumes an annual rate of return of 7%. The assumed rate of return is not guaranteed. Your actual results will differ from the values being illustrated. |

Objection 3: “I understand that establishing trusts can be beneficial from a tax planning standpoint, but the whole concept of locking up funds in a trust makes me feel uncomfortable. I don’t want my descendants to feel like I’m controlling their financial affairs from the grave – why spend time and money setting up trusts, just to have my descendants potentially resent me after I die?"

You are certainly not alone in your outlook – many people are hesitant to set up complicated planning structures (for a variety of reasons). Effective estate planning should reflect and prioritize your values – and tax efficiency is just one of many important considerations. However, helping the next generation save for education, retirement, and healthcare, in a tax-efficient way, are generally causes most families can get behind, and the transfers described in this article do not require trusts, family corporations, or even a lawyer. Further, these strategies maximize income tax-free, or deferred compounding. Simply calling your BBH relationship manager and setting a few automatic payments may result in significant tax savings over the long term – without the headache of complicated administration, tax returns, or legal fees.

Withdrawals of taxable amounts are subject to ordinary income tax to the extent of gain, and a 10% federal income tax penalty may apply prior to age 59.5.

Contact Us

1 $13.99 million per person in 2025 under current tax rules ($27.98 million for a married couple). This amount will increase to $15 million per person ($30 million for a married couple) on January 1, 2026.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved. PB-08973-2025-10-13