“Understanding intrinsic value is as important for managers as it is for investors. When managers are making capital allocation decisions … it's vital that they act in ways that increase per-share intrinsic value and avoid moves that decrease it. ... Over time, the skill with which a company's managers allocate capital has an enormous impact on the enterprise's value.” – Warren Buffett, Berkshire Hathaway Letter to Shareholders, 1994.

Berkshire Hathaway Chairman Warren Buffett is widely regarded as one of the most successful investors in history; his management track record is arguably just as singular. A hallmark of Buffett’s management philosophy is his unusual attention to capital allocation. He advocates that capital allocation is equally, if not more, important than operating prowess in driving long-term shareholder value.

Studies show that companies that continually evaluate the performance of business units, acquire and divest assets, and adjust resource allocations based on relative market opportunities outperform those that do not. The development of a capital allocation framework is a strong catalyst for value creation. While capital allocation is generally perceived to be more relevant for public companies, it is just as important for private companies.

Capital allocation framework

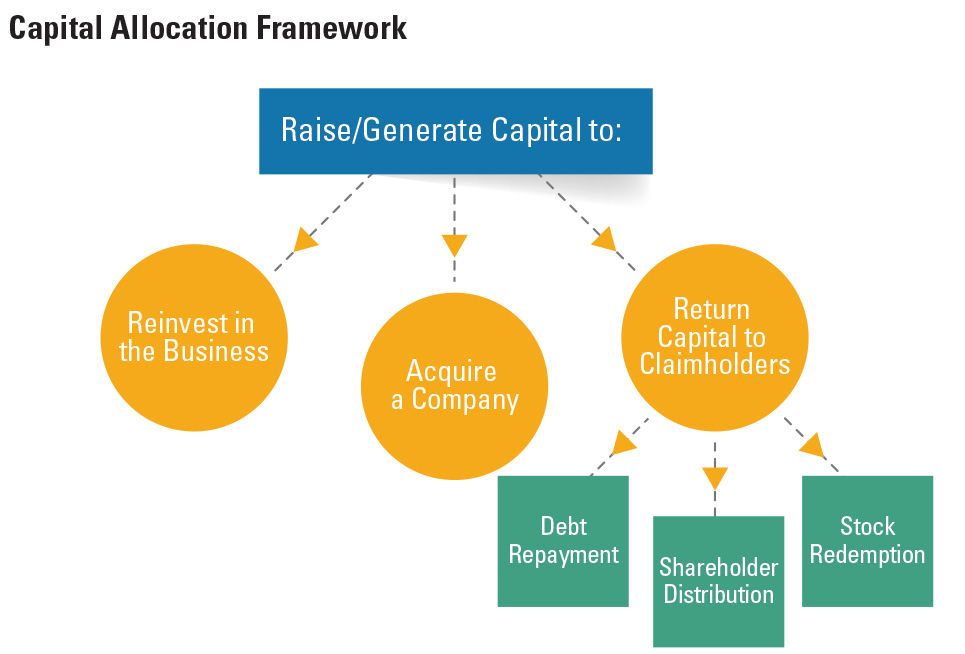

Capital allocation decisions are vital in determining a company’s future and, as such, are among management’s most important responsibilities. Managers have three basic choices for deploying capital:

- Reinvesting in the existing business (underwriting capital expenditures, funding research and development, or adding to the sales team)

- Acquiring another company

- Returning cash to claimholders (issuing dividends, redeeming shares, and repaying debt)