Line chart showing U.S. core PCE inflation (blue, left axis) and 3‑month change in nonfarm payrolls (red, right axis) from 2022 to mid‑2026. Core PCE declines from about 5.5% in 2022 to around 2.7–3.3% by 2025–2026, while payroll growth falls from roughly 500k to near zero, with intermittent volatility in both series.

Kevin Warsh was sworn in as Federal Reserve (Fed) chair on May 22, becoming its 17th chair since 1913, and its 11th since the modern Federal Open Market Committee (FOMC) structure was established in 1936. He inherits a Fed grappling with sticky inflation and a stabilizing labor market.

The June 16-17 FOMC meeting will mark Warsh’s first as Fed chair. That meeting also features an update to the Summary of Economic Projections (SEP), giving markets an early read on how Warsh intends to reshape the communication framework around the monetary policy outlook.

During his Senate hearing, Warsh stressed his desire for a regime shift in the Fed’s communication strategy leaning towards ‘strategic ambiguity’, questioning the value of regular post-meeting press conferences, and arguing for fewer speeches from Fed officials.

Importantly, Warsh does not believe in forward guidance, blaming it for compounding the inflation is “transitory” mistake of 2021–2022. As such, expect him to downplay the importance of the SEP and dot plots, at least until he can convince a majority of the FOMC to move away from them.

A clean break from the current communication framework will be challenging. A recent Brookings Institution survey of academic and private-sector Fed experts showed:

- 85% of 52 respondents regarded the post-meeting press conference as “extremely useful or useful”

- 56% said the same about the SEP (excluding dots) and dot plot

The Concensus

The market narrative is that Kevin Warsh will steer the FOMC in a more dovish direction, weighing on USD and steepening the yield curve. That is hardly a groundbreaking take given Warsh’s view on productivity, inflation, and the Fed’s balance sheet.

- Warsh expects the productivity boost from artificial intelligence (AI) to justify lower interest rates, noting “AI will be a significant disinflationary force, increasing productivity and bolstering American competitiveness.”1 During the current business cycle, starting in Q4 2019, labor productivity has grown at an annualized rate of 2.1%. As such, productivity is running strong enough to keep the roughly 4% annual wage growth consistent with the Fed’s 2% target.2

- Warsh said he preferred to follow “trimmed averages” inflation as opposed to core price index for personal consumption expenditures (PCE). The Dallas Fed trimmed mean PCE and the Cleveland Fed 16% trimmed mean CPI are currently below core PCE, implying room for the Fed to loosen policy.

Line chart (1985–mid‑2026) comparing three U.S. inflation measures: Dallas Fed trimmed mean PCE (blue, latest 2.40%), core PCE (red, 3.30%), and Cleveland Fed 16% trimmed mean CPI (green, 2.80%). All three declined from ~4% in the mid‑1980s to around 1.5–2% by the late 1990s, stayed near the 2% reference line through 2020, then spiked sharply to 4–5.5% during 2021–2022 before retreating toward 2.4–3.3% by 2026.

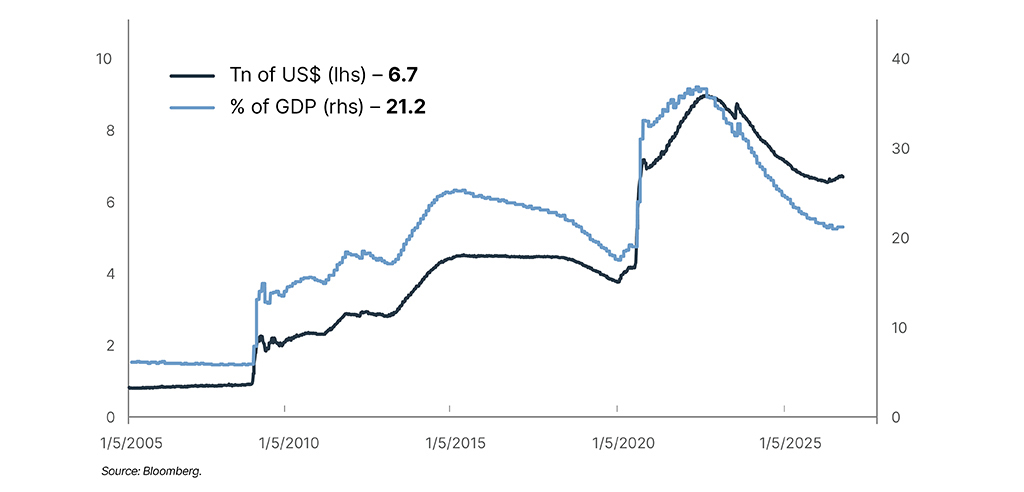

- Warsh favors slashing the Fed’s balance sheet to create scope for rate cuts. According to Warsh, “The Fed’s bloated balance sheet…can be reduced significantly. That largesse can be redeployed in the form of lower interest rates to support households and small and medium-size businesses.”3 He has also noted “the interest rate tool gets in the cracks. It’s fairer. The balance sheet tool disproportionately helps those with financial assets."4

Line chart (2005–2029) showing the Federal Reserve balance sheet in trillions of dollars (blue, left axis, latest $6.73T) and as a percentage of GDP (red, right axis, latest 21.20%). Both series rose in steps—from ~$1T/~6% pre-2008 to ~$4.5T/~25% after QE rounds—then surged to ~$9T/~36% of GDP during the 2020 pandemic response. Since 2022, both have declined as quantitative tightening progressed, with the balance sheet falling to ~$6.7T and ~21% of GDP by mid-2026.

The Constraints

Kevin Warsh faces two major constraints that could disappoint markets expecting a more dovish Fed tilt.

- FOMC is not a one man show. Warsh cannot simply dictate policy, which is made collectively by 12 voting members; 7 members of the Board of Governors, the president of the New York Fed, and 4 of the remaining 11 regional Fed presidents, who vote on a rotating basis. Non-voting regional Fed presidents still participate in discussions and can also influence the debate.

The center of gravity on the FOMC has already shifted from an easing to a more neutral bias. Regional Fed presidents Beth M. Hammack, Neel Kashkari, and Lorie K. Logan did not support inclusion of an easing bias in the April 29 post-meeting statement. Even dovish-leaning Fed Governor Chirstopher Waller pumped the brakes on cuts late last month highlighting “I can no longer rule out rate hikes further down the road if inflation does not abate soon.”5

Granted, if Jerome Powell decides to leave the Board of Governors, President Donald Trump will likely reappoint staunch dove Stephen Miran to the vacant seat as Warsh assumed Miran’s temporary board role. That would hand Trump appointees a majority on the board, but not enough overall votes to deliver a materially more dovish FOMC especially as the underlying disinflationary trend has stalled.

| Board of Goveernors - if Jay Powell resigns | ||

|---|---|---|

| Term | Appointed by | |

| Kevin Warsh | January 31 2040 | Trump |

| Stephen Miran? | January 31 2040 | Trump |

| Chris Waller | January 31 2030 | Trump |

| Michelle Bowman | January 31 2034 | Trump |

| Philip Jefferson | January 31, 2036 | Biden |

| Michael Barr | January 31, 2032 | Biden |

| Lisa Cook | January 31, 2038 | Biden |

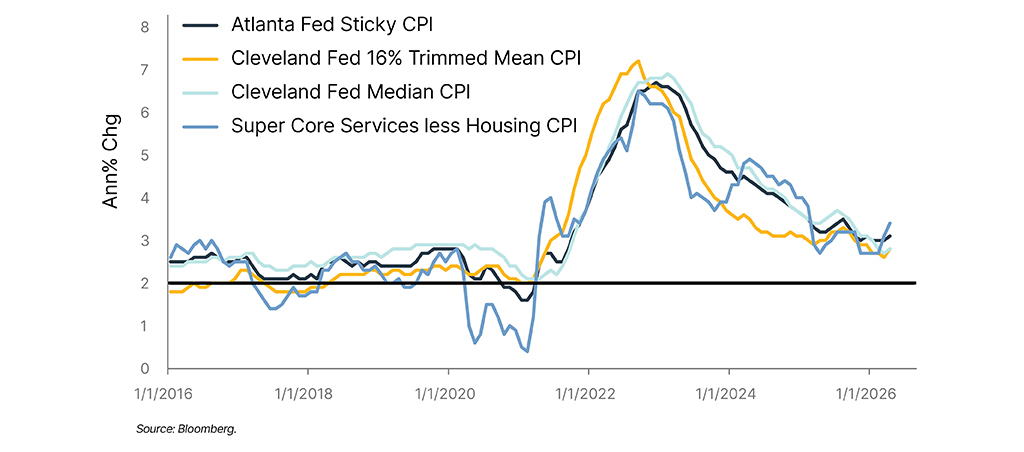

Line chart (2016–mid‑2026) comparing four U.S. underlying inflation measures: Atlanta Fed Sticky CPI (blue, latest 3.10%), Cleveland Fed 16% Trimmed Mean CPI (orange, 2.80%), Cleveland Fed Median CPI (black, 2.80%), and Super Core Services less Housing CPI (green, 3.40%). All four hovered near 2–3% pre-pandemic, then surged between 2021–2023—peaking at roughly 4–7%, with super core and sticky CPI reaching the highest levels. All have since retreated but remain above the 2% reference line, clustering in the 2.8–3.4% range by mid-2026.

- Funding market stress risk limits the Fed’s ability to reduce the balance sheet. To shrink the Fed’s balance sheet in a significant way would involve reducing reserve demand. Reserves are the funds that depository institutions hold in accounts at the Fed. They are the safest and most liquid asset in the financial system and give banks greater scope to settle payments in an orderly way.

Reserve balances make up the bulk of the Fed’s liabilities and are directly controlled by the Fed. By contrast, the other two big liabilities on the Fed’s balance sheet – currency outstanding and the Treasury General Account (TGA) – are outside the Fed’s control.

Reserves currently represent $3.1 trillion of the Fed’s $6.7 trillion in liabilities or about 10% of GDP. Before the 2008 global financial crisis, reserves totaled just $17 billion of the Fed’s $890 billion in liabilities. The surge in reserves reflects the Fed’s large scale asset purchases (quantitative easing), the Fed’s shift from a scarce to an ample reserve system to control short-term interest rates, and tighter bank liquidity regulations.

Stacked area chart of Fed balance sheet liabilities from 2005 to 2025, showing steady growth followed by a sharp surge in 2020 driven by reserves and other liabilities, then gradual decline; total peaks near $9 trillion and settles around $6–7 trillion.

Reserve balances are comfortably above levels the Fed judges consistent with adequate reserves, estimated to be around 9% of GDP or $2.7 trillion. The risk of operating at lower levels of reserves is that liquidity conditions can tighten abruptly as banks become less willing to lend reserves into funding markets to preserve liquidity buffers. That raises the risk of spikes to short-term market rates and heightened volatility, as seen during the September 2019 repurchase agreement (repo) crisis when reserves fell below 7% of GDP.6

Bottom line

The FOMC consensus driven structure and reserve-scarcity risks constrain the scope for a straightforward dovish regime shift under Warsh. Moreover, there is a real possibility that Warsh becomes the first modern Fed chair to be outvoted on policy. The result is likely a more volatile rates backdrop with the dollar facing structural credibility headwinds but proving more cyclically resilient than markets expect.

1WSJ “The Federal Reserve’s Broken Leadership,” November 16, 2025

2https://www.bls.gov/news.release/pdf/prod2.pdf

3Id, WSJ “The Federal Reserve’s Broken Leadership,” November 16, 2025

4Id, WSJ “The Federal Reserve’s Broken Leadership,” November 16, 2025

5Federal Reserve, Policy Risks Have Changed, May 22, 2026

6Federal Reserve, What Happened in Money Markets in September 2019?, February 27, 2020

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners.© Brown Brothers Harriman & Co. 2026. All rights reserved. IS-11579-2026-06-01