Bond yields have surged this year as the Federal Reserve (Fed) continues to fight a surge in inflation. Following many years of monetary policy suppression, fixed income valuations have become much more attractive. With all the attention on inflation, Fed tightening, and rising rates, we would like to shine a light on taxable municipal bonds, a growing, and often overlooked sector. Taxable municipal bonds offer an excellent way to diversify broader taxable bond portfolios through high-quality, durable credits1 that frequently offer higher yields than comparably-rated corporate debt. Strong credit resiliency further bolsters the case for taxable municipal debt in the face of ongoing economic uncertainties. BBH portfolios often include allocations to taxable municipal bonds based on their attractive risk-adjusted return benefits and the more efficient portfolio outcomes they help create.

First of All… Taxable Munis?

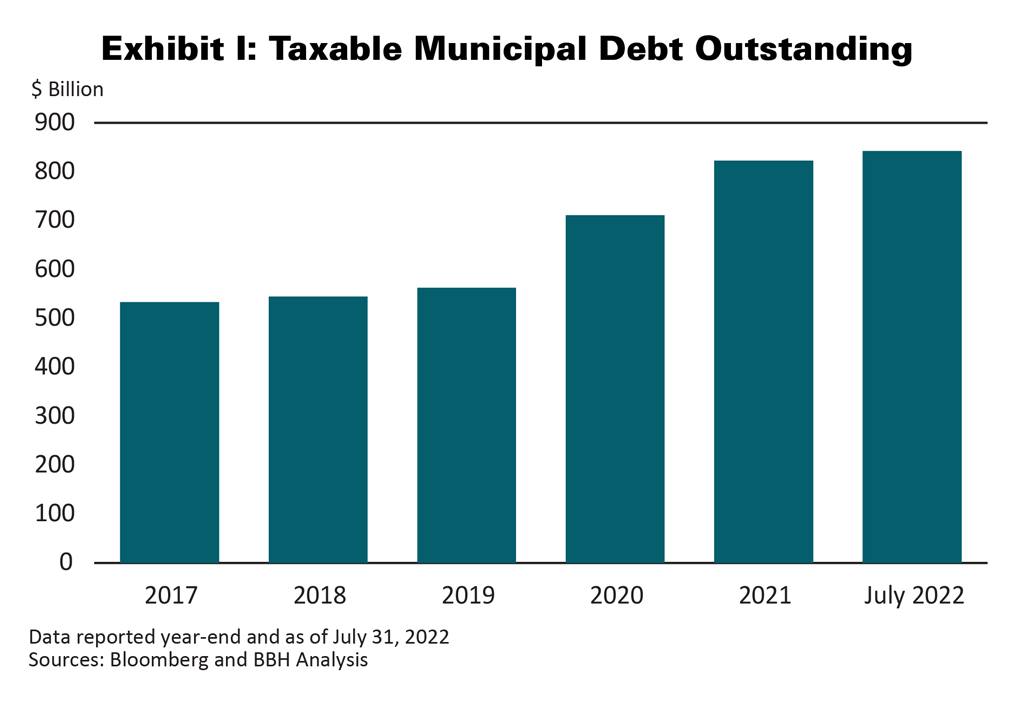

The Tax Reform Act of 1986 placed a limitation on the purpose type for which municipal bonds could be sold tax-exempt, thus paving the way for federally taxable municipal bonds to emerge. These types of issues generally provide for pension funding, working capital, and refunding of tax-exempt debt. Build America Bonds (BABs), Recovery Zone Economic Development Bonds, and Qualified School Construction Bonds were introduced via the American Recovery and Reinvestment Act of 2009. These types of issues are federally taxable municipal bonds where issuers receive direct payments from the U.S. Treasury to subsidize their interest costs. The Tax Cuts and Jobs Act of 2017 provided another catalyst for taxable issuance by eliminating tax-exempt advance refunding transactions. Even though the overall size of the municipal market has remained steady for the past decade, the taxable portion of it has grown steadily. Currently, taxable bonds comprise 21% of the outstanding municipal market, up from 14% at the end of 2017.

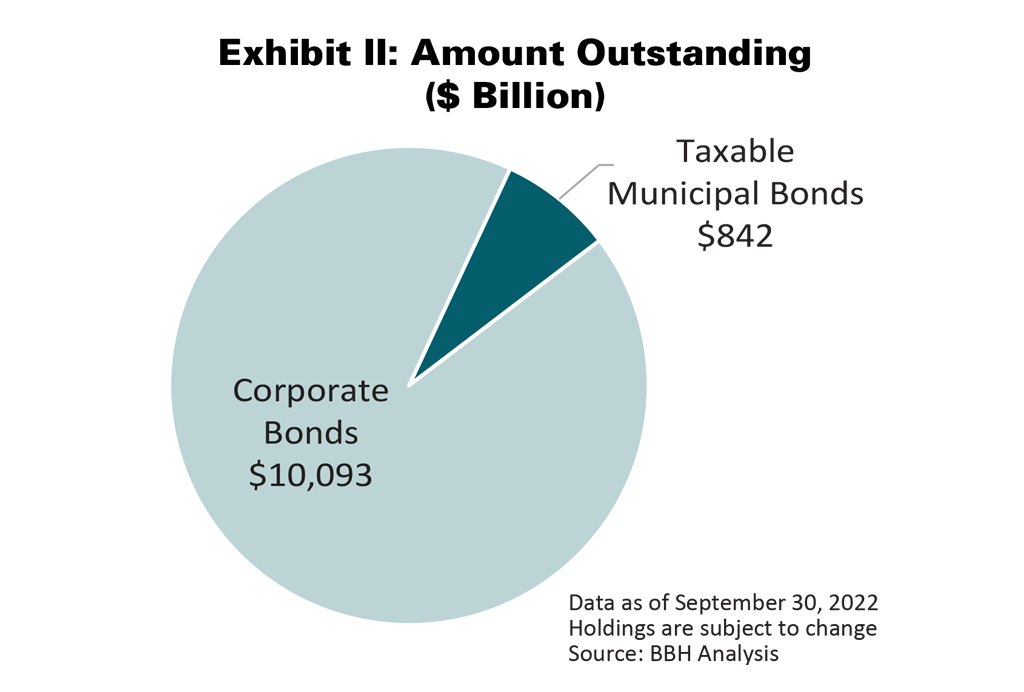

Exhibit I shows that the taxable municipal market has grown to over $800 billion outstanding, and it offers prospective investors a large and deep market to gain meaningful exposures.