* 34th percentile of 136 strategies over 1 year, 5th percentile of 135 strategies over 5 years, and 7th percentile of 128 strategies over 10 years in the U.S Core Plus Fixed Income Category based on gross returns as of for the periods ending 12/31/2025.

Strategy Objectives: Peer-leading results, preservation of capital

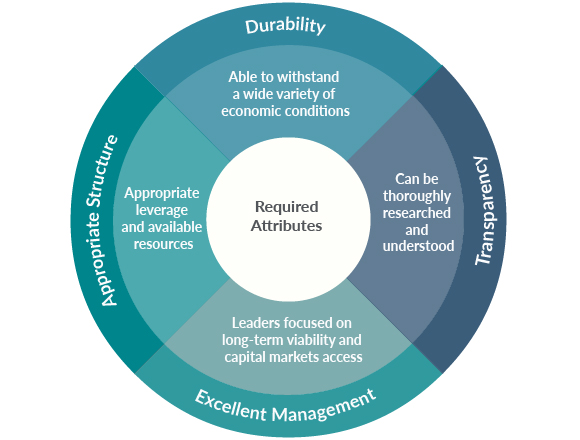

The Core Plus Fixed Income Strategy is designed to deliver excellent returns through market cycles for investors seeking broad exposure to the U.S. fixed income markets. We take an active management approach, seeking to build duration-neutral taxable bond portfolios from the bottom up and allowing valuation to drive our portfolio construction. We only invest in credits we believe to be durable, well-managed, appropriately structured, and comprehensively researched and understood.

Where there is volatility, we see opportunity. Credit spreads can be more volatile than underlying credit fundamentals, which creates a recurring need for active management.

Investment Process

Our valuation framework:

- Allows uniform evaluation of the entire fixed income market.

- Incorporates a margin of safetyX

Margin of Safety

With respect to fixed income investments, a margin of safety exists when the additional yield offers, in BBH's view, compensation for the potential credit, liquidity and inherent price volatility of that type of security and it is therefore more likely to outperform an equivalent maturity credit risk-free instrument over a 3-5 year horizon.

See More Definitions considering volatility differences across sectors and ratings tiers.

- Highlights new opportunities and assesses the ongoing attractiveness of existing holdings.

- Provides valuable input on position-sizing and allocating our credit team’s resources.

Buy Discipline:

- Systematic review and ranking of available credit universe

- Deep fundamental credit review of identified opportunities

- Durable positions sized commensurate with expected excess return

Sell Discipline:

- Trim positions as margin of safety recedes

- Sell positions when a margin of safety no longer exists

- Immediate sale if the analyst’s credit outlook changes

We view investment risk in absolute, rather than relative, terms. We believe the greatest risk to a fixed income portfolio is the permanent impairment of a portfolio holding. Our credit underwriting process is a primary defense against impairment.

- We employ this disciplined process through the lifecycle of an investment.

- We underwrite all credit investments to maturity and only purchase performing credits we believe to be highly durable.

- Every credit we purchase has been pre-stressed to withstand the most severe adversity that we anticipate for its industry or asset type.

We believe that investors should only accept risk for which they are appropriately compensated. Our valuation framework helps quantify investment risks to identify opportunities that are worthy of deeper research. Our fundamental credit criteria, along with continuous discipline around position size and economic sector concentration help to mitigate portfolio risk.

We ensure both a well-controlled trading platform and compliance with client guidelines through a comprehensive enterprise risk management framework including:

- Pre-trade guideline clearance by a dedicated risk management team

- Independent senior management compliance oversight

- Formal weekly portfolio reviews

What Makes Us Different? Bottom-up, value-conscious investment process

- We strive to identify strong absolute-value, not relative-value, opportunities.

- We are entirely bottom-up with a team-based approach emphasizing security selection.

- Our portfolio sector exposures take shape through a strict adherence to our valuation and credit criteria.

- We avoid large macroeconomic and directional positions that add volatility, but not return.

How to Invest

Our Core Plus Fixed Income Strategy can be accessed through a variety of investment vehicles. To learn more please contact a member of our institutional relationship management team.

Visit the BBH Funds website and the BBH Luxembourg Funds website for more information about our public fund offerings.

Oops, this table is temporarily unavailable.

Please try again later or refresh the table.Portfolio Characteristics as of 12/31/2025

BBH Core Plus Fixed Income Composite

| Total Returns | Average Annual Total Returns | |||||||

|---|---|---|---|---|---|---|---|---|

|

Composite/Benchmark

|

3 Mo.

|

YTD

|

1 Yr.

|

3 Yr.

|

5 Yr.

|

10 Yr.

|

Since Inception (01/01/1986) |

|

|

BBH Core Plus Fixed Income Composite

(Gross of Fees)

|

1.07% | 8.21% | 8.21% | 7.33% | 1.91% | 4.64% | 6.32% | |

|

BBH Core Plus Fixed Income Composite

(Net of Fees)

|

1.00% | 7.94% | 7.94% | 7.06% | 1.65% | 4.38% | 6.05% | |

|

Bloomberg US Aggregate

|

1.10% | 7.30% | 7.30% | 4.66% | -0.36% | 2.01% | 5.54% | |

The Bloomberg Aggregate Bond Index is a market value-weighted index that tracks the daily price, coupon, pay-downs, and total return performance of fixed-rate, publicly placed, dollar-denominated, and non-convertible investment grade debt issues with at least $300 million paramount outstanding and with at least one year to final maturity. The index is not available for direct investment.

Effective January 1, 2026, Brown Brothers Harriman Credit Partners, LLC., a subsidiary of BBH, became the strategy's investment adviser. Performance prior to that date is of accounts managed by BBH.

Oops, this table is temporarily unavailable.

Please try again later or refresh the table.Portfolio Characteristics as of 03/31/2026

BBH Core Plus Fixed Income

| Representative Account | Benchmark | ||

|---|---|---|---|

|

Effective Duration (years)

|

5.71

|

5.82

|

|

|

Yield to Maturity

|

6.26%

|

4.57%

|

Portfolio holdings and characteristics are subject to change.

Portfolio Characteristics are of the Representative Account. The Representative Account is managed with the same investment objectives and employs substantially the same investment philosophy and processes as the strategy.

The BBH Core Plus Fixed Income Strategy was previously called the BBH Core Fixed Income Strategy.

Gross of fee performance results for this composite do not reflect the deduction of investment advisory fees. Actual returns will be reduced by such fees. Net of fees performance reflects the deduction of the maximum investment advisory fees. Returns include all dividends and interest, other income, realized and unrealized gain, are net of all brokerage commissions, execution costs, and without provision for federal or state income taxes. Performance is calculated in U.S. dollars.

eVestment rankings are based on gross of fee performance of the Composite and reflect reinvestment of earnings. The deduction of an advisory fee reduces an investor's return. Return may not be representative of any one client's experience. Past performance does not guarantee future results.

Effective duration is a measure of the portfolio’s return sensitivity to changes in interest rates.

Yield to Maturity is the rate of return the portfolio would achieve if all purchased bonds and derivatives were held to maturity, assuming all coupon and principal payments are received as scheduled and reinvested at the same yield to maturity. This figure is subject to change and is not meant to represent the yield earned by any particular security. Yield to Maturity is before fee and expenses.

This communication is for informational purposes only and does not constitute an offer or a solicitation to buy or sell any particular security or to adopt any specific investment strategy. The information herein has not been based on a consideration of any individual investor’s circumstances and is not investment advice, nor should it be construed in any way as tax, accounting, legal or regulatory advice. Any views and opinions are subject to change at any time.

Strategies are shown without regard to whether they are offered as separately managed account mandates or through pooled vehicles. Any discussion of or reference to any given strategy herein should not be taken as a recommendation or solicitation of any pooled vehicle which has an investment objective featuring or similar to such strategy.

This material does not constitute an offer or solicitation in any jurisdiction where or to any person to whom it would be unauthorized or unlawful to do so.

“Bloomberg®” and the Bloomberg U.S. Aggregate Index are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by Brown Brothers Harriman & Co (BBH). Bloomberg is not affiliated with BBH, and Bloomberg does not approve, endorse, review, or recommend the BBH Core Fixed Income Strategy. Bloomberg does not guarantee the timeliness, accurateness, or completeness of any data or information relating to the strategy.

Risks

There is no assurance that a portfolio will achieve its investment objective or that the strategy will work under all market conditions. The value of the portfolio can be affected by changes in interest rates, general market conditions and other political, social and economic developments. Each investor should evaluate their ability to invest for the long-term, especially during periods of downturn in the market.

Investing in the bond market is subject to certain risks including market, interest-rate, issuer, credit, maturity, call and inflation risk; investments may be worth more or less than the original cost when redeemed.

The value of some asset- backed securities and mortgage-backed securities may be particularly sensitive to changes in prevailing interest rates and are subject to prepayment and extension risks, as well as risk that the underlying borrower will be unable to meet its obligations.

Income from municipal bonds may be subject to state and local taxes and at times the alternative minimum tax.

Below investment grade bonds, commonly known as junk bonds, are subject to a high level of credit and market risks.

The strategy invests in derivative instruments, investments whose values depend on the performance of the underlying security, assets, interest rate, index or currency and entail potentially higher volatility and risk of loss compared to traditional bond investments.

Foreign investing involves special risks including currency risk, increased volatility, political risks, and differences in auditing and other financial standards. Prices of emerging market securities can be significantly more volatile than the prices of securities in developed countries, and currency risk and political risks are accentuated in emerging markets.

The strategy may engage in certain investment activities that involve the use of leverage, which may magnify losses.

A significant investment of assets in one or more sectors, industries, securities and/or durations may increase its vulnerability to any single economic, political, or regulatory developments, which will have a greater impact on returns.

Illiquid investments subject the investor to the risk that she may not be able to sell the investments when desired or at favorable prices.

The strategy is offered through BBH Credit Partners, a subsidiary of Brown Brothers Harriman & Co. New York, New York.

Investment Advisory Products and Services:

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE

Past performance does not guarantee future results.