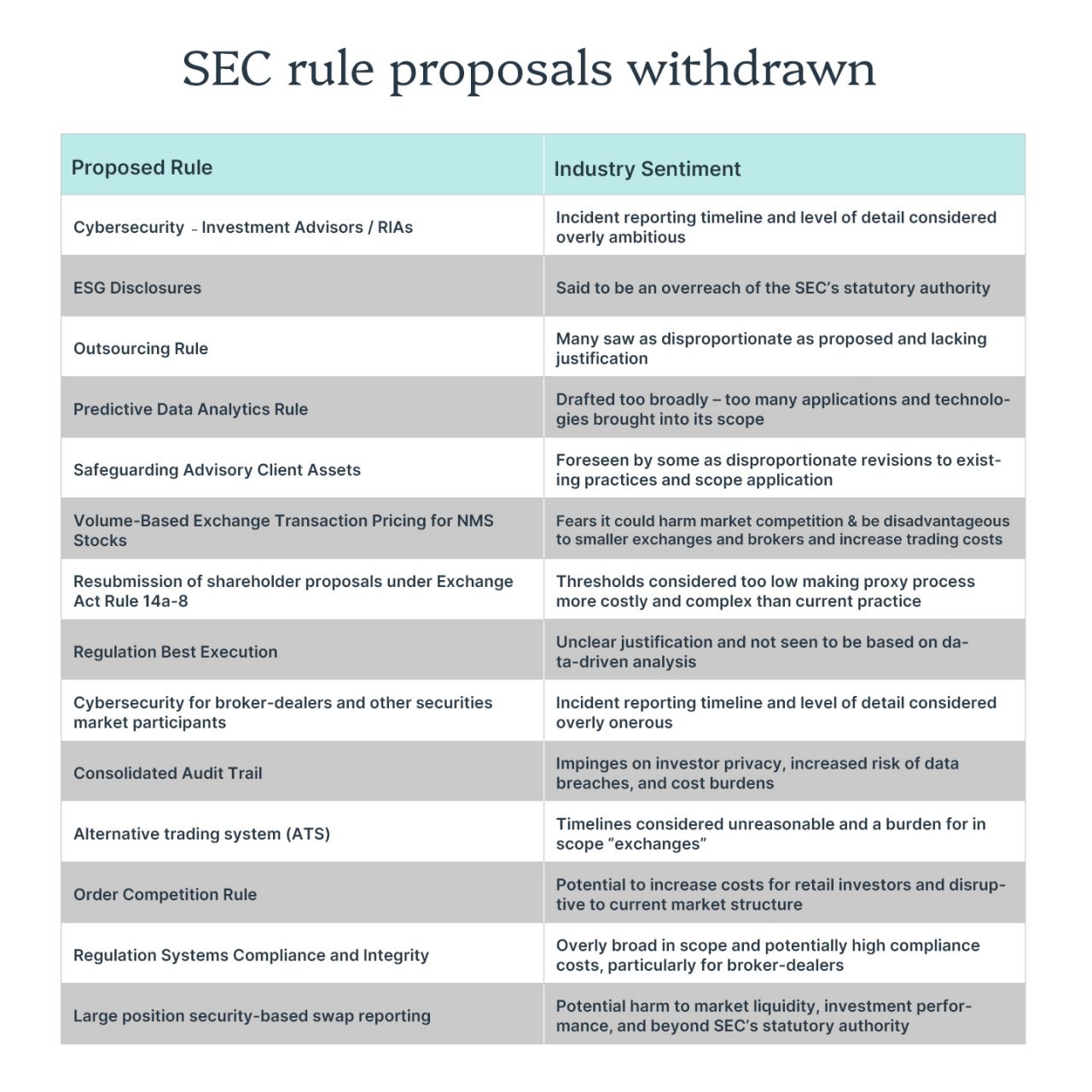

It’s hard not to argue that we are currently living in an era of "loud diplomacy" where policy pronouncements come in a very public and assertive manner, later amplified on social media. Therefore, it was interesting to see the Securities and Exchange Commission quietly drop a raft of previously proposed rules carried over from the Gensler Commission1 with no major fanfare.

This is even more unusual given the fact that the vast majority of the 14 previously proposed rules were largely contentious upon their release fuelling much industry debate.

The rules in question had been subject to notices of proposed rulemaking, but on June 12 the SEC formally withdrew them in keeping with previous statements that it would rebalance its priorities under new chair, Paul Atkins. The SEC notice doesn’t elaborate on the reasons for the withdrawals, nor revisit any of the history of the proposals and portrays Chair Atkins as a master of understatement:

"The commission does not intend to issue final rules with respect to these proposals," the notice reads. "If the commission decides to pursue future regulatory action in any of these areas, it will issue a new proposed rule."

Although the nixing of many of the rules was largely expected, the manner and volume of rules withdrawal is substantial and will be largely welcomed by all firms regulated by the SEC.

One of the criticisms of the prior Commission was that there wasn’t enough opportunity to comment or engage with the SEC on the proposals. If any version of these rules does reappear, it is clear there will be ample opportunity to engage and publicly comment upon any fresh proposals.

There will be SEC rulemaking

Nevertheless, new rule proposals remain likely during the remainder of the current administration, including the possibility of revisiting some of the themes and topics that formed part of the now-withdrawn proposals.

Despite this significant rule proposal purge, it is clear that the Commission wishes to put in place a comprehensive regime to address cryptocurrencies and other digital assets.

The omnipresent artificial intelligence debate means that with rapid proliferation of AI tools across the market, the SEC will likely see the need to address it sooner rather than later; however, with a materially different scope and level of detail compared to the previous Gensler-led proposal.

There are also a host of other deliberations, including those related to dual-class structures for mutual funds and ETFs and consideration of allowing more retail access to private market funds.

The Atkins- led SEC is already looking and feeling very different to its predecessor but that doesn’t mean there won’t be plenty to analyze in the coming months. However, it does seem the rulemaking process might be less fractious, and industry will be given more time and more space to comment on any proposals. A more harmonious and dispassionate rulemaking process seems likely which might give some comforting respite from a world which often seems increasingly full of drama and conflict.

1 Gary Gensler served as SEC chair under the Biden administration.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries.This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2025. All rights reserved. IS-10876-2025-06-27