Applications: deliver services to companies or directly to consumers

Platforms: LLMs and SLMs

Infrastructure: semiconductor value chain and hyperscalers

Artificial intelligence (AI) has dominated headlines over the past several years, and it’s been top of mind for investors as well. On behalf of our next gen newsletter, The Fresh Take, Brown Brothers Harriman Senior Client Associate Jared Edelstein sat down with Vice President and Senior Equity Analyst Anurag Dhanwantri to discuss the latest hot topics in the space.

Jared Edelstein: Let’s start with the basics. What is AI, and why has it received so much attention?

Anurag Dhanwantri: AI, stated simply, is an attempt to get computer systems to do tasks that normally require human faculties, such as visual perception, speech recognition, and decision-making.

AI could soon be the fastest mass-adopted technology platform, with broad-based impacts on our personal and professional lives. You can understand the excitement and hype. Usually, mass adoption takes time. For example, it took 20 years for personal computers to reach 50% user penetration in the U.S. Over the past few decades, the adoption curve has accelerated: The internet achieved 50% penetration in 12 years, and mobile phones did so in six years. Some say AI could reach 50% penetration in about three years.

Many of the companies held in BBH’s equity portfolios, already have AI products in the market. Microsoft is selling AI-powered co-pilots (digital assistants that help enhance productivity) in the enterprise (office) market, and Adobe has launched AI-powered creative tools. Apple plans to launch its first Apple Intelligence smartphones later this year.

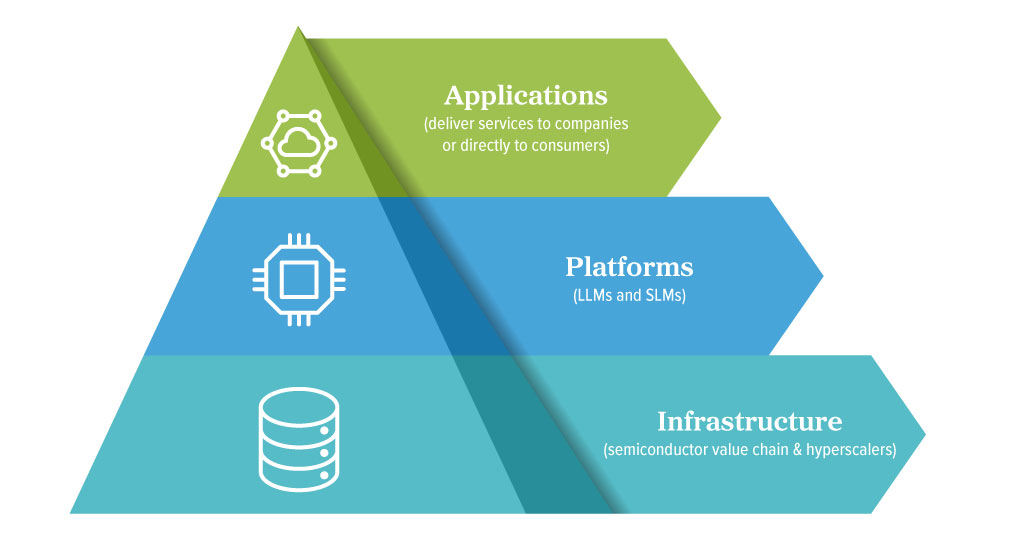

JE: What are the different layers of the AI technology stack (chipmakers, app developers, and so forth), and what areas do we think are the most attractive from an investment opportunity standpoint?

AD: My team likes to think of the AI technology stack as a pyramid:

Applications: deliver services to companies or directly to consumers

Platforms: LLMs and SLMs

Infrastructure: semiconductor value chain and hyperscalers

We evaluate each investment opportunity against BBH’s clearly defined qualitative and quantitative criteria. We currently find the most attractive investment opportunities in the infrastructure layer, although some of our invested companies cut across all three layers of the pyramid.

Most of our investments in the infrastructure layer predate AI’s breakthrough moment in January 2023 (Microsoft‘s $10 billion investment in OpenAI) by years and are based on existing strong non-AI competitive advantages (moats) that drive well-above-average free cash flow per share growth and returns on invested capital. AI-driven economics will be an addition on top of the already formidable financial profiles of our investments.

Our investments in Microsoft, Amazon, and Google are examples of companies that cut across all three layers of the AI pyramid. Microsoft is a leading hyperscaler (infrastructure), has a close working relationship and financial stake in OpenAI (platform), and is already leveraging its dominant enterprise software position to sell co-pilot licenses (application). Google and Amazon, the other leading hyperscalers have also invested in LLMs – Google internally in Gemini and Amazon externally in Anthropic. These three companies run differentiated strategies in their profitable operations and have other cash-generative non-AI businesses. AI-related benefits will again be additive to the existing exceptional financial profile.

JE: Microsoft, Amazon, and Google have been household names for quite some time. Talk to me about Nvidia. What does the company do, and why is it considered one of the biggest players in AI?

AD: Nvidia provided the crucial link that helped morph generative AI from a concept to commercial reality. LLMs, the heart of generative AI, require costly, time-consuming computing power, which was not available in the central processing unit (CPU) architecture that existed before Nvidia. (CPUs are semiconductor chips that, among other applications, run most of the computing on our personal computers, or PCs).

Enter Nvidia, the leading graphics processing unit (GPU) company. The business innovated and launched a GPU – a semiconductor chip that traditionally ran graphics on our PCs – fast enough to train LLMs in a realistic period and within a reasonable budget, in turn unleashing investments across the AI pyramid.

LLM: large language models SLM: small language models GPU: graphics processing unit CPU: central processing unit |

Since its inception in early 1990s, when Nvidia was one among many startups targeting the then-nascent graphics card niche, Nvidia has beaten its own path, with a unique approach to chip design and chip upgrade cadence. Nvidia’s approach to AI is also differentiated vs. the conventional chip supplier model. The company has taken a solutions approach – for example, Nvidia’s Hopper is a complete hardware/software solution for AI data centers that weighs 70 pounds and has 35,000 parts.

Given the criticality of GPUs to AI, it is not surprising to see investments in GPU design across the technology industry. In addition to conventional players like Intel and AMD, most hyperscalers and Meta have been working on their own custom silicon. Nvidia is not sitting still, though. Its soon-to-be-launched B200 GPU is expected to deliver chip-level cost performance that is multiple times better than any existing Nvidia or competitor chip. In terms of raw compute power, Nvidia’s soon-to-be-launched Blackwell will mark 1,000 times improvement in eight years.

JE: We are already seeing evidence of companies using AI tools to enhance worker productivity and, in some cases, replace workers with AI automation. How will AI affect the job market, and which industries will be most impacted?

AD: AI will undoubtedly affect some jobs, but we think, in aggregate, AI will likely end up a net positive for the society.

We may need AI-driven productivity to cover for the aging society and the declining working age population in most of the developed world. UN statistics show that by 2045, the working age population will decline by 119 million in China, 45 million in Europe, and 11 million in Japan. In the U.S., the working age population is projected to increase by 13 million by 2045, but aging will affect the U.S. as well. The U.S. Census Bureau projects that by 2045, more than one in five Americans will be older than 65, up from one in seven today.

Dynamic market economies retrain and reskill workers all the time. ATMs undoubtedly led to job losses among bank tellers, E-ZPass took away toll collection jobs, and we have had many more powerful technology platforms and innovations in the last few decades –yet the recent unemployment rates are not much higher than the lowest ever recorded unemployment rates.

JE: How are governments viewing AI? What, if any, regulation is being discussed to impose limits or curtail the scope and uses of AI?

AD: Regulation typically tends to lag any fast-paced technology development. We expect AI regulation will follow a similar path. For example, 28 years after Section 230 was signed into law by President Clinton to protect Americans’ freedom of expression online by protecting the intermediaries that make the expression possible (for example, Meta and Google), Congress and courts are still debating the utility and the extent of Section 230 immunity.

Governments will also have to strike a delicate balance between managing the scope and use of AI against national security concerns of not “falling behind” in the AI arms race.

JE: What are some of the risks of AI (ethical concerns and climate impact, for example), and how are companies managing this?

AD: Warp-speed growth in AI will force management teams to make important judgment calls to balance near-term headlines with long-term sustainable business models. Copyright protection and data privacy are already bubbling up as important AI-related issues. Adobe and Apple have set a positive example, so far. Adobe’s AI-powered creative tools are based on LLMs that are trained only on data where Adobe has explicit permission to use the data. Adobe can, in turn, offer peace of mind to its customers as they integrate Adobe’s AI-powered creative tools into their workflows. Apple is promising to use only publicly available data to train its AI models and not device-specific data from Apple consumers.

Energy consumption and the resultant climate impact is the other AI hot button topic. At a superficial level, GPUs consume a lot more energy than CPUs. However, per unit of energy consumed, GPUs are far more efficient than CPUs.

AI is evolving fast, attracting tens of billions of dollars in investments across the world. Watch this space as we continue to look for investment opportunities in line with our qualitative and quantitative criteria.

JE: Anurag, thank you for your time.

Brown Brothers Harriman & Co. (“BBH”) may be used to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries. This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners. © Brown Brothers Harriman & Co. 2024. All rights reserved. PB-07754-2024-09-19