How did early 19th-century merchants actually pay for the goods that sailing ships hauled back and forth between the United States and Britain?

Bank notes were of no use to foreign sellers, while moving specie (gold, silver, or other precious metals) across the oceans was both risky and expensive. Separated from buyers by an ocean that took weeks or months to cross, sellers found it difficult to know when—or sometimes if—they would ever get paid.

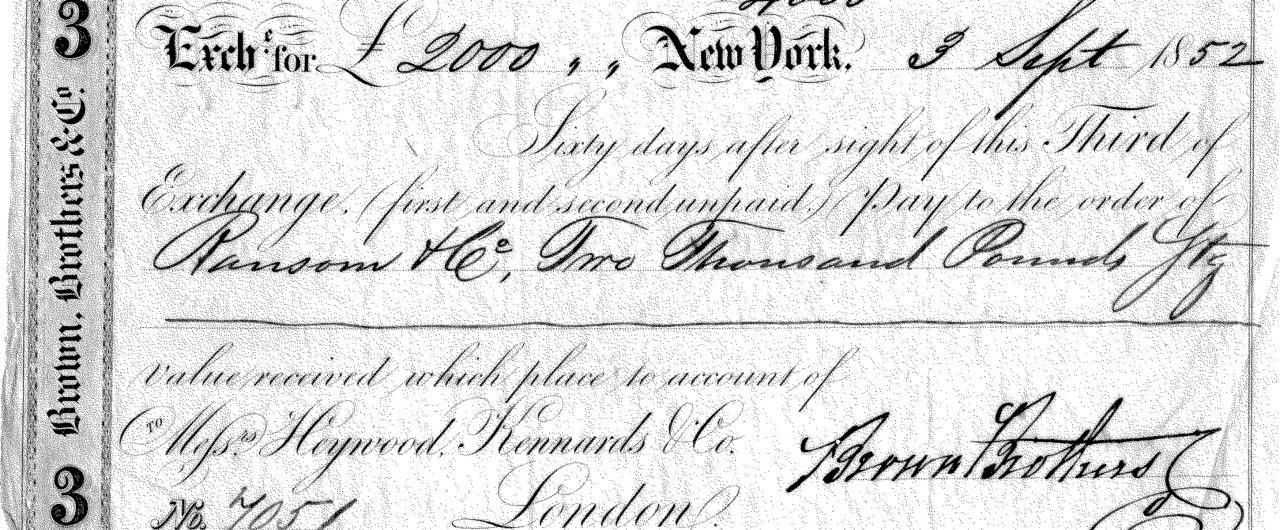

These were age-old problems of international trade. The solution, conceived by 13th-century Italian merchants, was the “bill of exchange.”

Like an international check, a bill of exchange was nothing more than a written order to pay a certain sum of money to the person or company named on the bill at a future specified date—usually three to four months hence to allow for the transport of goods and payment in return.

The bill of exchange became an integral part of early 19th century Anglo-American trade. A U.S. importer wishing to buy goods from a British merchant purchased a bill in dollars from a U.S. merchant banker promising to pay in sterling. The bill was “drawn on” a U.K. merchant banker with which the U.S. merchant banker had a correspondent relationship—or, in the case of the Browns, another house in the same firm.

The U.S. merchant banker exchanged the U.S. dollar bill for a bill promising to pay in sterling and forwarded it (or the equivalent in commodities) to the U.K. merchant banker as payment, who then paid the U.K. exporter when the bill matured. Merchant bankers earned a commission of between one and five percent, according to their role in the transaction.

What made the bill of exchange so powerful was its liquidity.

In practice, the U.K. exporter rarely held the bill to maturity but rather sold it to a bank or broker at a discounted price in return for immediate payment, a transaction called “discounting.” The bank or broker that agreed to purchase the bill thereby “accepted” it, guaranteeing the bill against default. Firms that discounted on a regular basis, including the Browns, became known as “acceptance houses.”

The bill of exchange was also a useful credit instrument.

The U.S. importer sold the goods he had purchased as soon as he received them, usually several months after the bill of exchange had been issued; only then would he pay the bill of exchange. Together with letters of credit and advances on consignment, the bill of exchange enabled buyers and sellers to finance operations in the long interval between production and sale, a crucial factor in the growth of Anglo-American trade.

One reason for Brown Brothers’ success in this realm was its unique organizational structure:

With its allied firm in Liverpool, it was the only Anglo-American merchant bank that could both issue and guarantee a bill of exchange. This gave the firm a powerful advantage over other merchant banks that were forced to coordinate with an independent agent on either end of the transaction.

For Further Reading

- Sven Beckert, Empire of Cotton: A Global History. New York: Penguin Random House, 2014.

- Stanley Chapman, The Rise of Merchant Banking. London: Routledge, 2013.

- James R. Fichter, So Great a Proffit: How the East Indies Trade Transformed Anglo-American Capitalism. Cambridge: Harvard University Press, 2010.

- Edwin J. Perkins, Financing Anglo-American Trade: The House of Brown, 1800-1880. Cambridge, Mass: Harvard University Press, 1975

Brown Brothers Harriman & Co. (“BBH”) may be used as a generic term to reference the company as a whole and/or its various subsidiaries generally. This material and any products or services may be issued or provided in multiple jurisdictions by duly authorized and regulated subsidiaries.This material is for general information and reference purposes only and does not constitute legal, tax or investment advice and is not intended as an offer to sell, or a solicitation to buy securities, services or investment products. Any reference to tax matters is not intended to be used, and may not be used, for purposes of avoiding penalties under the U.S. Internal Revenue Code, or other applicable tax regimes, or for promotion, marketing or recommendation to third parties. All information has been obtained from sources believed to be reliable, but accuracy is not guaranteed, and reliance should not be placed on the information presented. This material may not be reproduced, copied or transmitted, or any of the content disclosed to third parties, without the permission of BBH. All trademarks and service marks included are the property of BBH or their respective owners.© Brown Brothers Harriman & Co. 2021. FIRM-00337-2021-04-20