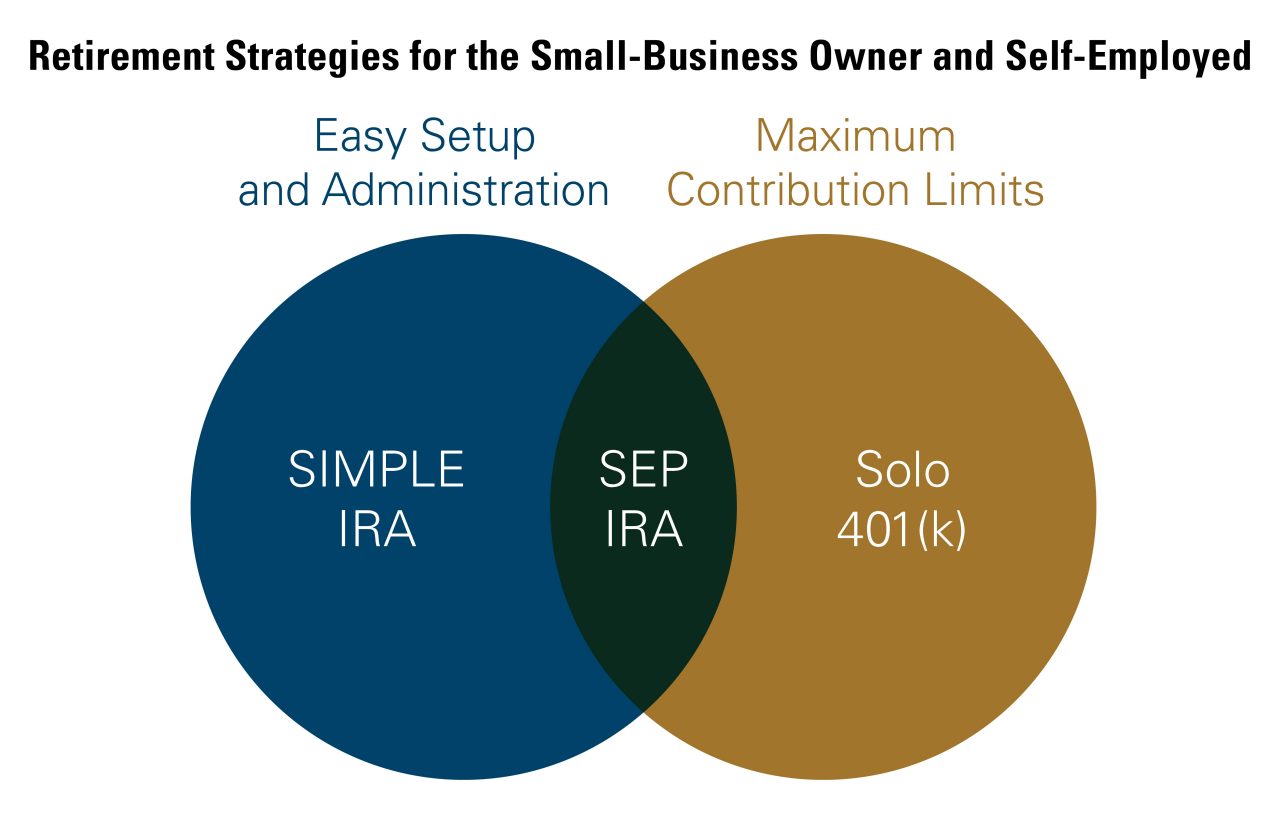

Savings Incentive Match Plan for Employees

A SIMPLE IRA is ideal for small-business owners with 100 employees or fewer who do not have any other type of retirement plan and who are looking for their employees to participate in the funding of their own retirement. These plans are funded by both the employer and employee through salary reductions and, importantly, a mandatory employer contribution every year. As the name suggests, they are easy to set up and administer, and all contributions immediately vest.

There are two big disadvantages to SIMPLE IRAs. The first is their relatively low contribution limits of $14,000 per year. This contribution limit increases to $17,000 when an individual turns 50 years old in a calendar year through what is called a catch-up contribution. The second disadvantage is that employers have an obligation to contribute to these plans each year either through a match or a nonelective contribution of up to 2% of compensation for eligible employees. Eligible employees include anybody who has made $5,000 in compensation during any of the two years preceding the current calendar year and is reasonably expected to receive at least $5,000 in compensation during the current calendar year. For businesses in growth mode, or for those with less predictable cash flow, a mandatory annual contribution for each employee may not be feasible.

SIMPLE IRAs follow the same distribution rules as traditional IRAs in that individuals can begin receiving funds at 59 ½ years old with no 10% penalty and must start receiving funds by April 1 of the following year in which they turn 70 ½. No matter one’s age, though, when a SIMPLE IRA is established, funds must be held in that plan for at least two years. If funds are transferred or withdrawn before the two-year participation rule, the penalty is more severe at 25%. All funds distributed from a SIMPLE IRA are included in an individual’s ordinary income.

Solo or Individual 401(k)

A Solo or Individual 401(k) plan is most ideal for sole proprietors and business owners with no employees, other than a spouse, and no future plans to add any. These plans can be funded with much higher contribution limits than SIMPLE IRAs. The business owner (individual) in these plans is considered the employer and employee, and therefore can make both a salary reduction contribution of up to $20,500 and a profit sharing contribution of up to 25% of compensation (not to exceed $55,000) when combined with the salary reduction contribution. A Solo 401(k), similar to a SIMPLE IRA, also allows for an annual catch-up contribution of an extra $6,500 when a participant turns 50 years old. These limits are similar to the types of 401(k) profit sharing plans seen at big corporations; however, like SIMPLE IRAs, Solo 401(k) plans are easy to set up and vest immediately. Another advantage to Solo 401(k) plans is the flexibility they can offer by permitting an owner to allow the plan to include loans.

Unlike SIMPLE IRAs, the major drawback of Solo 401(k) plans is that they involve more administrative work to remain in compliance. As such, these plans require a plan administrator, who will be responsible for periodic plan amendments resulting from any legislative changes, as well as annual IRS tax filings through IRS Form 5500 once plan assets reach $250,000.

Simplified Employee Pension Plan

If it seems like we have painted two incomplete pictures of the perfect retirement planning solution for small-business owners and sole proprietors, it is because we have. Fear not, however, as the ideal combination of easy setup and administration and high contribution limits does exist. The answer? SEP IRAs. Similar to SIMPLE IRAs, SEPs are easy to set up and administer – almost as easy, in fact, as a traditional IRA. In order to establish a SEP, a small-business owner or self-employed professional would simply need to execute and keep a record of a 5305-SEP document (found on the Internal Revenue Service’s website). This document does not need to be reported to any regulatory agency and can simply be held on file by an IRA custodian or personally.

Unlike a SIMPLE or traditional IRA, the contribution limit for a SEP IRA is very generous. An employer can fund the plan with the lesser of 25% of compensation or $61,000 (for 2022) – 10 times a traditional IRA’s contribution limit. In addition, all contributions are tax deductible to the business. A major advantage to a SEP contribution is that there are no age restrictions on when a professional must stop making contributions, compared with the limit of 70 ½ years old for traditional IRA contributions. As long as the business owner has eligible compensation, he or she can continue making employer contributions after age 70 ½. A SEP is then managed exactly like a traditional IRA and can even be rolled into a Roth IRA. While there are tax implications for doing the latter, those taxes are essentially a wash due to the initial contribution’s tax deductibility. In fact, the SEP IRA contribution and subsequent rollover to a Roth IRA can be a highly advantaged strategy so long as there is 1099 income. In a traditional backdoor Roth, a participant can get around income limits by contributing to a traditional IRA first and then rolling it into a Roth. However the amounts, as discussed, are capped at $5,500 ($6,500 for those over 50 years old) annually. With a SEP, those contributions can be up to 10 times as large, allowing for a $61,000 backdoor Roth. Therefore, the simplicity of establishing and administering a SEP combined with generous contribution limits to the business owner or self-employed professional create a very favorable solution for those with active income who do not want the administrative hassle. SEP IRA plans also follow the same rules as traditional IRAs when it comes to withdrawing money. Once an individual reaches age 59 ½, he or she can begin withdrawing the funds with no 10% penalty and, as in SIMPLE IRAs, an individual must start withdrawing the funds by April 1 of the following year in which he or she turns 70 ½. That is, of course, unless the plan has been rolled into a Roth IRA, at which point there are no mandatory distributions. All funds withdrawn are subject to an individual’s ordinary income rate.

As a trusted advisor to business owners and executives, Brown Brothers Harriman’s goal is to find efficiencies for our entrepreneurial clients. Taking advantage of a SEP IRA is a wonderful, efficient way to maximize retirement contributions and allow for years of tax-deferred, or tax-free, compounding – a strategy that we are confident would garner Einstein’s approval.