Over the 10 years ending April 30, 2020, the S&P 500 Index returned 11.7%, outperforming the 3.6% and 1.5% returns of international developed and emerging markets equities, respectively. The same pattern of outperformance for the S&P 500 holds true during the COVID-19 crisis. Given this historical return data, it is reasonable to ask why investors should invest in non-U.S. equities at all.

There are several reasons why we believe investors should diversify their portfolios to include non-U.S. equities. Before we explore those reasons, it is important to note that Brown Brothers Harriman’s (BBH’s) portfolios have generally been overweight to U.S. large-cap equities for some time now. That positioning is not based on a top-down call, but is a result of our bottom-up research process, where we have been able to identify compelling U.S. equity managers that have capacity to take capital and create portfolios with attractive return potentials. Notwithstanding this overweight, we have also been able to identify compelling active international developed and emerging markets equities managers that make investments in a select group of individual companies that we believe can outperform U.S. large-cap equities over the long term. We prefer to invest in businesses with recurring cash flows, high-quality balance sheets and strong competitive moats whose stocks trade at discounts to their intrinsic values. In addition, when investing outside the U.S., we ensure that our managers look for adequate transparency and financial reporting, which can at times be more difficult to obtain. With a long-term view, investors should be rewarded with attractive returns from a portfolio of such high-quality companies regardless of where they are domiciled. We would also caution clients not to rely on historical returns as an indication of forward-looking returns. Our managers seek to identify businesses whose value has not yet been recognized in the prices of their stocks. In our opinion, while it is difficult to invest when returns have not been as strong, it is often the right decision that leads to compelling returns in the future.

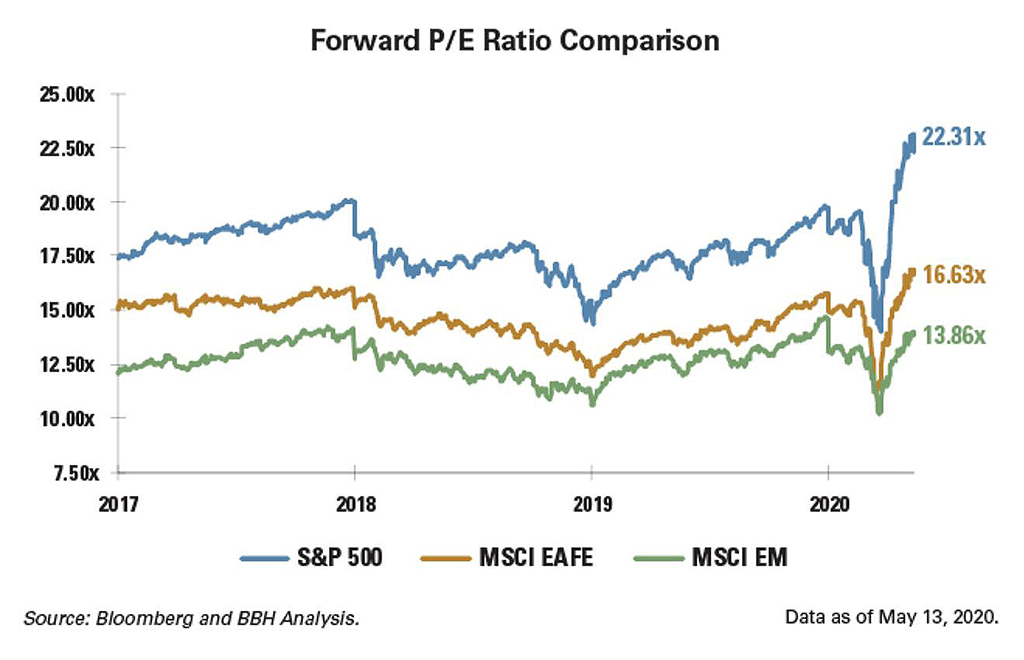

There are several interesting data points that support investing in non-U.S. equities.

First, let’s look at the price-to-forward earnings ratios for the S&P 500, MSCI International Developed (EAFE) and MSCI Emerging Markets (EM) Indices.