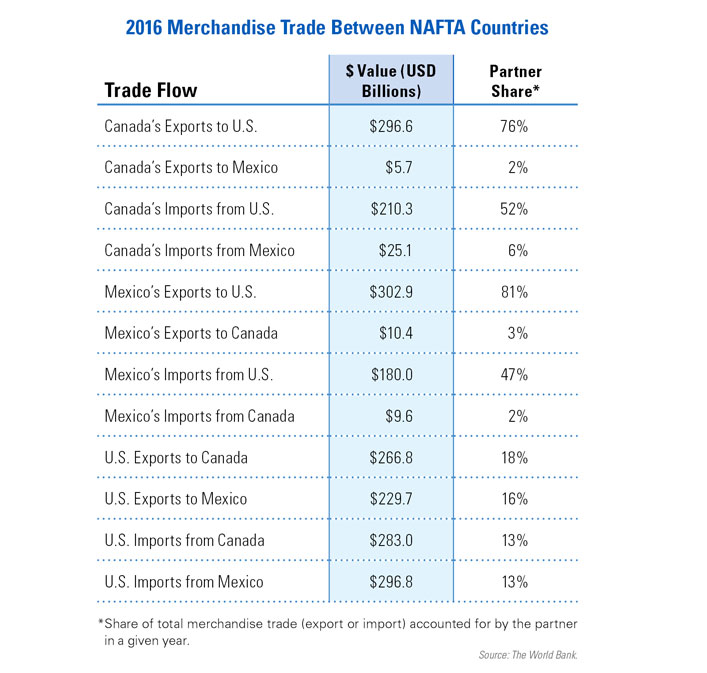

The North American Free Trade Agreement (NAFTA) created one of the world’s leading free trade areas, comprising the United States, Canada and Mexico, which together account for 28% of global GDP.1 NAFTA recognized existing trade patterns and facilitated the growth of new ones. Geopolitical strategic factors were also priorities of its proponents during the late 1980s and early 1990s. However, the agreement’s longevity and the evolution of political and economic factors since its 1994 enactment recently prompted leaders of its member countries to clarify their vision for its future.

In this article, we provide a historical perspective on NAFTA’s origins and objectives, present details of current trade patterns among NAFTA countries and highlight various changes that have been agreed to in its update as the U.S.-Mexico-Canada Agreement (USMCA) in 2018.

NAFTA’s Origins

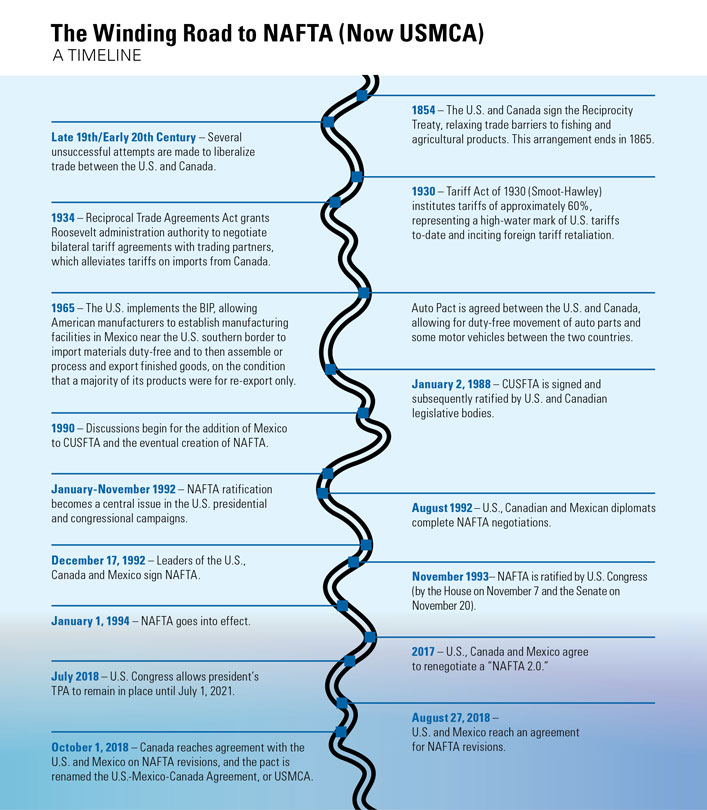

As early as 1854, the U.S. and Canada saw merit in facilitating bilateral cross-border trade. The nations signed a Reciprocity Treaty that relaxed barriers to the flow of Canadian natural resources into the United States. The U.S. ended this arrangement in 1865 following suspicions of Canadian support for the Confederacy during the Civil War. Although several attempts were made in both countries to reinstate free trade policies during the late 19th and early 20th centuries, none were successful. Only the 1934 Reciprocal Trade Agreements Act, passed to incrementally alleviate tariffs raised by the 1930 Smoot-Hawley Act, provided a measure of bilateral tariff reduction between the U.S. and Canada over the next century.2

In recognition of the geographical integration of the automotive industry, principally in the Great Lakes region, the U.S. and Canada agreed to the 1965 Auto Pact, which allowed for duty-free movement of auto parts and some motor vehicles between the two countries. Two decades later in 1986, Canada’s Conservative Mulroney government and the U.S. Republican Reagan administration began negotiating the Canada-U.S. Free Trade Agreement (CUSFTA), which was signed on January 2, 1988, and then ratified by the Canadian Parliament and U.S Congress.3

CUSFTA was the forerunner to NAFTA. Mexico’s participation had roots in several early trade liberalization initiatives. For example, the U.S. implemented the Border Industrialization Program (BIP) in 1965, which allowed manufacturers in Mexico near the U.S. southern border to import materials duty-free and then to assemble or process and export finished goods.4 These border factories became known as maquiladoras, the Spanish term for “miller.” One of the main drivers of the BIP was to alleviate unemployment and poverty along the U.S.-Mexico border; however, U.S. manufacturers quickly discovered labor cost efficiencies there and established affiliates in northern Mexico.

After CUSFTA, negotiations began for the addition of Mexico to the trading bloc and continued until 1992. NAFTA was signed on December 17, 1992, by leaders of the three countries – Brian Mulroney, George H.W. Bush and Carlos Salinas de Gortari – and ultimately went into effect on January 1, 1994. But first, NAFTA had to be ratified by all three nations, including both houses of the U.S. Congress.

Support for the agreement was far from universal, and within NAFTA one can observe an emergence of mobilized coalitions in the U.S. both for and against the expansion of free trade. Earlier U.S. trade liberalization efforts enjoyed broad bipartisan support. For example, the AFL-CIO supported President Kennedy’s 1962 Trade Expansion Act, viewing it as a way to create jobs by expanding trade.5 By the early 1990s, however, a general economic downturn and years of job losses in the U.S. manufacturing sector began to erode the free trade consensus.

Key opponents emerged during the 1992 U.S. presidential campaign and amplified NAFTA into a central issue. These included candidates on the right – such as Patrick Buchanan, who opposed NAFTA and ran a primary challenge against then-President George H.W. Bush – successfully garnering over 20% of the vote across a geographically diverse group of states.6 On the left, environmental, labor (including the AFL-CIO) and other grassroots activists (such as Ralph Nader’s Public Citizen organization) began voicing their opposition to NAFTA as early as 1990, citing what they viewed as weak environmental and labor standards in Mexico.7 Rounding out the opposition to NAFTA from across the political spectrum was independent candidate H. Ross Perot, who made the economy and immigration central planks of his platform.

Principal supporters of NAFTA at the time were Republican incumbent George H.W. Bush and Democratic candidate Bill Clinton. The Bush administration had, like its Reagan predecessors, shepherded free trade agreements over the course of several years, including NAFTA and, concurrently, the Uruguay Round negotiations of the General Agreement on Tariffs and Trade (GATT), which led to the 1995 creation of the World Trade Organization (WTO). The U.S. business community was solidly behind NAFTA passage, and leading the charge was USA-NAFTA – a coalition of 2,300 businesses that sent leaders into congressional districts to advocate NAFTA passage ahead of congressional votes on the pact in fall 1993.8 Overall, it is estimated that U.S. companies spent over $17 million on advertising and lobbying in favor of NAFTA’s passage.9

Candidate Clinton’s support for NAFTA in 1992, however, was nuanced. His endorsement of the pact – just one month prior to his election as president – included conditions that the final agreement should contain worker adjustment assistance, tighter environmental rules and the creation of a joint commission to improve labor standards and safety in Mexico.10 Meanwhile, Bush administration negotiators, led by U.S. Trade Representative (USTR) Carla Hills, secured key provisions to NAFTA in 1992 with a goal of easing its impact and building broad-based support. Tariffs on Mexican exports of agricultural products into the U.S. would be phased out over a 15-year period, rather than immediately. Further, rules of origin standards, which stipulate that a minimum percentage of a product’s contents must originate from the NAFTA countries in order to qualify for tariff-free trade within the bloc, were added to prevent other countries from using Mexico or Canada as a tariff-free export platform into the U.S.11

President Clinton’s USTR Mickey Kantor, ahead of the fall 1993 congressional vote on NAFTA, added to his predecessor’s list of exceptions to broaden support for the pact. A 1993 NAFTA side agreement established a three-nation panel to investigate violations of national environmental laws. A similar panel designed to enforce national labor laws and to force wage increases in Mexico, however, was not agreed to. Lastly, Kantor negotiated sector-based deals to shelter U.S. agriculture producers from an immediate wave of imports, accelerate Mexican tariff reduction on U.S. appliance exports and seek a longer period for the elimination of textile and apparel quotas in the Uruguay Round negotiations.12

A combination of Republican support and concessions reached through NAFTA side agreements enabled Clinton to achieve passage of NAFTA by the Democratic-majority U.S. House of Representatives on November 7, 1993, by a margin of 234 to 199. Just 102 of the 258 Democrats in the House voted for NAFTA, while 132 of the 175 Republican members voted in favor of passage.13 This represents the last time a free trade agreement has been ratified without significant Republican Party opposition. Senate passage was achieved on November 20, 1993, by a vote of 61 to 38, with support from a majority of senators from both parties.

The nearby maps show the degree to which each state’s congressional delegation supported NAFTA ratification in 1993 as well as the importance of NAFTA as a destination for each state’s exports in 1993 and 2017. In observing the percentage of each congressional delegation’s (defined as all U.S. House and Senate members representing the state) support of NAFTA, compared with each state’s percentage of total exports that went to Canada and Mexico in 1993, one can observe the following:

- Congressional delegations generally voted in line with the economic interests of their states – that is, those from states that sent a large portion of their total exports to Canada and Mexico in 1993 strongly supported NAFTA. The opposite was true for states that sent few exports to these countries.

- Notable exceptions were coastal and border states Florida, Louisiana, New Mexico and Washington, whose representatives strongly supported NAFTA, despite their sending a relatively small share of exports to Canada and Mexico at the time. Perhaps these states’ representatives saw an opportunity in greater economic integration through NAFTA?

- Another exception can be observed with border states Michigan and North Dakota, whose congressional delegations strongly opposed NAFTA, despite Canada and Mexico being a significant market for their exports. Perhaps these representatives were concerned by potential threats posed by NAFTA?