After developing a love of wine in college, Patrick Stella knew that he wanted to work in the wine industry. The question revolved around how he was going to do it. What was ultimately born was WineCredit, a wine lending service founded by Stella in 2013 that allowed him to combine his finance background, passion for wine and entrepreneurial side to solve a burning issue in the wine industry: a lack of credit. We recently had the pleasure of sitting down with Stella in New York City to discuss the extent to which wine is investable, shifting sources of demand and value in the market, issues surrounding wine forgery and tips for people looking to build a collection.

Brown Brothers Harriman: Describe your business and the types of opportunities you look for.

Patrick Stella: Broadly speaking, the goal of WineCredit is to underwrite fine wine anywhere, in any way that we can get our hands on.

The variety is in the financial structuring. We serve many different types of clients and accommodate a lot of different needs. We might help a merchant expand inventory and manage working capital by underwriting wine it holds as inventory, or we might help a private collector create a bridge loan while he waits to receive the liquidity from selling a home.

As for why clients come to us, we provide competitively priced, incremental capital against an asset that isn’t doing anything except sitting around soaking up cash. It’s also an asset that – in a worst case – clients can live without. People often ask me, “Why would anyone borrow against a wine collection when they could get a home equity line of credit, or HELOC, at a cheaper rate?” My answer is that price isn’t everything. Utilizing a wine collection instead of a house to fund an investment can be a great form of risk management. If the investment succeeds, you probably won’t notice that you paid an extra point or two of interest. If it fails, though, you’ll be very happy that all you have to do is sell part of your wine collection. Defaulting on a mortgage is obviously a bigger problem. Discretionary assets like a wine collection may not provide the absolute cheapest capital, but they can be a great match for higher-yielding, higher-risk opportunities from a risk perspective.

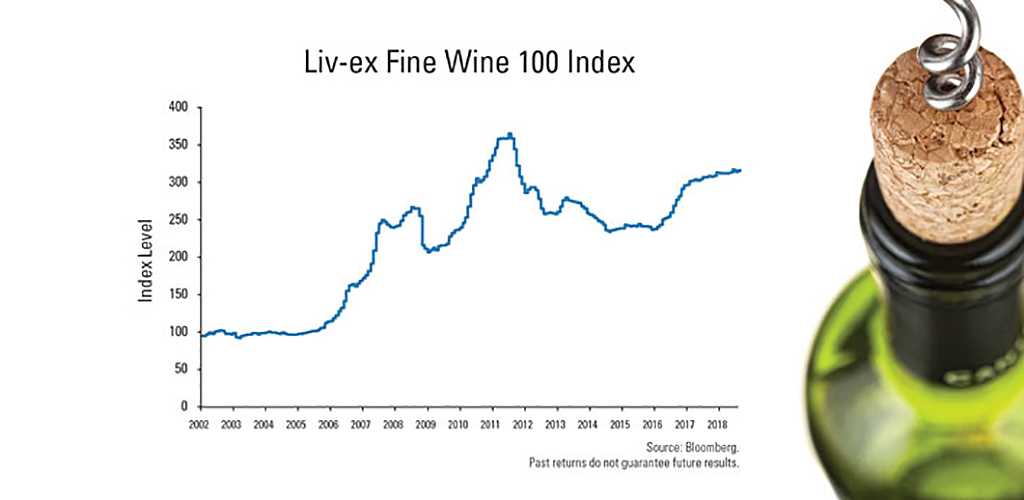

BBH: How investible has wine become, and how has storage evolved to keep up with it?

PS: The whole business that I started is an answer to that question. WineCredit’s theory is that wine is investible and that the best way to invest in it is from a credit perspective, not through speculation.

As a collector myself, I know there are transactional and frictional costs when you hold wine as an owner. It’s a market that clears efficiently but with relatively high transaction costs – probably about 20%. And then you have storage and insurance costs.

Wine is not going to tank, but it can be difficult to push your way through the transaction, storage and insurance costs that are just going to drag on your return. You need to have such appreciation to get a strong internal rate of return (IRR) when you factor those in. There are definitely specific producers, vintages and regions where you could have made good money holding them for 10 years, but I think once you factor out all those transactional and frictional costs, you are never going to get a huge IRR. So, wine is investible, but the magic solution is to do it from a credit perspective, not an equity perspective.

In terms of storage, the nice thing is that as the market trends upward, some of those costs are reduced because they are driven by electricity for refrigeration, security costs and square footage costs, not as much by value. Insurance goes up as the value of the bottle goes up, but things like storage, appraisals and inspections are all benefiting from economies of scale as prices rise.

Transportation costs are also relatively lower as prices increase. Shipping a $1,000 bottle of wine from London to New York is much cheaper on a percentage basis than shipping a $100 bottle. We are certainly seeing that the wine market is a lot more logistically efficient now than it was 20 years ago because there is money to be made shipping, selling, buying and trading.