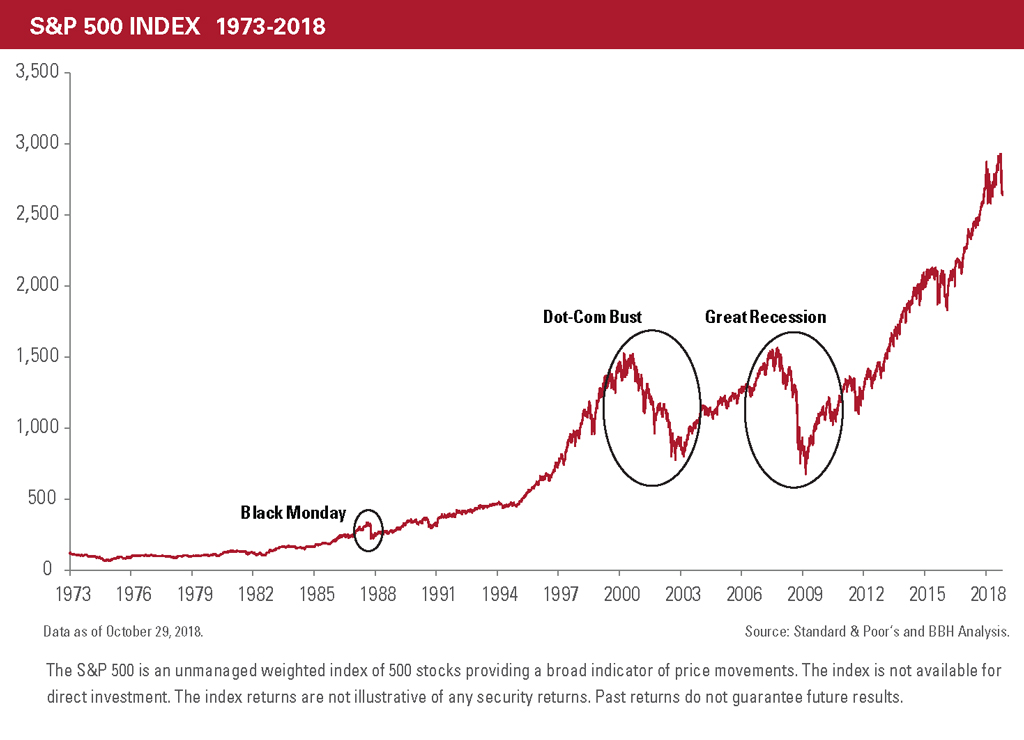

Yet this analysis of historical returns ignores a critical dynamic – inflation. In our earlier example, we observed that a dollar invested in stocks in 1973 would have grown to $85 today, but adjusted for inflation that figure would only be $15. This is still a fifteenfold real return on investment yet illustrates the challenge that inflation – even at modest levels – poses to the goal of wealth preservation.

Throughout this period, BBH has sought to add additional asset classes to client portfolios to help insulate against the threat of inflation while providing greater diversification and broader exposure to investment opportunities.

Investment Innovation

The first foray into an additional asset class took place in-house. BBH has served as banker and lender to middle-market companies throughout its history, so it seems inevitable that at some point the firm would provide equity capital in addition to the debt capital offered through its traditional banking practice. The firm launched its first private equity offering in 1989. Investors in this 1818 Fund I were primarily institutional, but by the 1993 launch of 1818 Fund II, the wealth management business was able to aggregate private client commitments into representing between 10% and 20% of the fund.

The firm’s private equity practice was rechristened BBH Capital Partners in 2006, and private clients and principals of the firm represented the majority of invested assets. That alignment of interest and capital differentiates the BBH approach from other private equity firms, as does the strategy for deploying capital. Rather than depend on investment banks and an auction process, BBH relies on a well-established ecosystem of private companies and owners to source investment ideas. This results in fewer, but better, investment opportunities.

While the private equity business was taking shape, the firm was also looking for ways to invest outside the United States in response to growing client demand for non-dollar assets. In the early 1990s, BBH’s International Equity Group managed money for several institutional clients, and this led to the launch of an international equities strategy in 1997. As with private equity, the primary audience for this fund was the firm’s own wealth management clients. Portfolio managers and analysts based in New York, London and Tokyo applied the same fundamental analytical approach as their domestic colleagues and shared research on global economic and market developments that influenced domestic as well as international assets.

Around the turn of the 21st century, growth of the wealth management business challenged a model that relied on portfolio managers in each office to construct portfolios from a list of approved securities. Jack Borland, the Partner who led the business at that point, notes that “it was clear that centralizing the management of equity portfolios was necessary. Client experiences varied too widely, and we needed to free up our managers’ time to focus on asset allocation, the introduction of new asset classes and client service. It was the only way to grow our business without damaging the client service approach for which we were known.” The business undertook the effort to transition portfolio managers into relationship managers charged with taking a more holistic approach to helping preserve and grow their clients’ portfolios.

Steps were taken in this direction in the early years of the 2000s and came to full fruition when Partners Rick Witmer and Tim Hartch assumed management of the centralized Core Select portfolio strategy in 2005. The Core Select approach was both old-fashioned and innovative at the same time. Witmer and Hartch, along with their team of analysts, sought to find companies that sell essential products and services, generate robust free cash flow on the strength of strong balance sheets, enjoy a sustainable competitive advantage and trade at a discount to the intrinsic value of the business. The Core Select idea was, in a way, simply a private equity approach to public equity markets, a philosophy resonant with the firm’s private equity activities as well as Witmer’s and Hartch’s prior experience in that asset class.

The subtly innovative idea behind this strategy is that successful investing is not an exercise in price anticipation, but in value recognition. We define risk as the possibility of permanent capital impairment, and long holding periods allow for the power of compounding to work in a tax-efficient way. This remains the Core Select philosophy today under the management of Partner Michael Keller

The evolution of financial markets and investment solutions brought BBH’s private wealth business to a fork in the road about 15 years ago. To meet growing client demand, we either had to develop new investment strategies ourselves or partner with third-party investors to allocate capital into new asset classes. Rather than try to be all things to all people, the firm decided to stick to those asset classes where it had a core competence and outsource management where it didn’t. The first application came in 2004 when we chose to outsource the management of our international equities strategy and appointed two subadvisors to manage the portfolio.

In the same way that our private equity practice informed the development of the Core Select philosophy, so, too, did the success of Core Select lay the groundwork for building out our network of third-party managers. Rather than adopt a completely open architecture approach, in which all investment decisions are outsourced, we opted for a hybrid approach, in the belief that remaining a disciplined and active investor allows us to more readily identify those traits in other managers.

What are the characteristics of a good investment manager? First, we want the principal investors at outside managers to have a lion’s share of their own wealth at risk in the same investment strategy that we are making available to our clients. This alignment ensures focus and leads to a second characteristic. Since they have their own capital at risk, our managers – like our colleagues in private equity and Core Select – define risk in absolute terms. If the ultimate objective of investing is to preserve and grow wealth, then falling behind an index from time to time does not represent real risk. Losing money does.

Most institutional money managers define risk as the possibility of deviating from an index, and they manage that risk by diversifying portfolios to the extent that they often mimic the benchmark. An investor who defines risk in absolute terms, however, manages risk through concentration. She wants to know the companies in her portfolio in such depth that she has the courage of her conviction to hold or even put more money to work in periods of market volatility. Good investors know what they own and why they own it, and that naturally leads to more concentrated positions.

Finally, we partner with investors who appreciate the importance of capacity. Every investment strategy is subject to the law of diminishing returns at some point, where the marginal dollar of committed capital requires a dilution of investment discipline. We want managers to be thoughtful about those constraints and close their practice to new inflows of funds as they approach capacity. Why would investors ever refuse new funds to manage? Because the driver of their own bottom line is not asset gathering, but the funds they already have invested in the same strategy as our clients. This alignment of interest is vanishingly rare in the investment management world and requires discipline and creativity to find.

The BBH Private Banking business today offers access to a wide variety of asset classes through its Wealth Strategies platform of third-party managers, now including some asset classes where BBH has an internal solution as well. As our business grows and markets evolve, we intend to keep expanding this platform, albeit at a thoughtful pace.

Whereas a firm doesn’t get to be 200 years old without innovating, nor does a firm survive for 200 years by chasing every new thing that Wall Street cooks up. Our history includes more than a few dodged bullets, such as underwriting securities in the years before the Great Depression or investing in subprime securities in the 2000s. Financial innovation is a double-edged sword, and we are cautious and thoughtful before embracing new financial products for our Private Banking clients.

In his 2002 letter to shareholders, Warren Buffett famously claimed that “derivatives are financial weapons of mass destruction, carrying dangers that, while now latent, are potentially lethal.” Buffett was proven tragically right (and prescient) when opaque counterparty risk in the derivatives market crashed the economy and markets a few years later. BBH clients suffered from the bear market of 2008 and 2009, but not nearly as much as the broad indices, and their portfolios therefore recovered more quickly.

In a similar vein, former Fed Chairman Volcker addressing a Wall Street audience in the wake of the financial crisis stated, “The most important financial innovation that I have seen in the past 20 years is the automatic teller machine.” Innovative financial products are often designed to enrich the issuer rather than the investor, and the age-old caveat of “buyer beware” is worth remembering. The list of investment fads that we have avoided is long. Among the rogues’ gallery of investment products that caused far more harm than good over the past few decades are variable rate annuities, margin trading, collateralized debt obligations, portfolio insurance and today’s cryptocurrencies.

Our success, and the success of our clients’ portfolios, is driven as much by what we’ve avoided as by what we’ve embraced.

The Bigger Picture

A culture of investing lies at the heart of our firm and our Private Banking business, yet we never forget that money is a means to an end. We spend a fair amount of time with our clients in order to understand what their ultimate objectives are regarding retirement, lifestyle, legacy, philanthropy and so forth. A careful investment approach helps clients pursue those goals, and over the years we have complemented our investment offerings with other services designed to help further preserve, protect and grow our clients’ wealth.